Contrary to the views of some, the number of people who have insurance coverage through the Exchanges as of January 1, 2014, matters to everyone. It matters because the pool that exists on that date will determine, at least for a while, whether the premiums charged by insurers in the Exchange are likely to be stable and the extent of the federal government’s multiple obligations to subsidize plans purchased on the various Exchanges. It is not as if insurers get a claims paying holiday simply because more and healthier people may enroll later in the year. It also matters because a major point of the Affordable Care Act was to increase in an efficient and relatively painless way the net number of people who have insurance or social protection against significant illness. If the numbers in the Exchanges and in the expanded Medicaid program do not way more than offset the number of persons who lose their insurance as a result of the ACA, or if the cost of extending health protection in this fashion proves too high, the ACA will not have accomplished its goals.

Given the chaos that has erupted as procrastination strains Exchange infrastructure and deadlines are repeatedly extended, it is difficult to tell right now whether the ACA is performing as hoped. A few things are clear, however. The first thing is that the Obama administration is not releasing the sort of information from which an objective assessment could be made. Platitudes such as “Millions of Americans, despite the problems with the website, are now poised to be covered by quality affordable health insurance come New Year’s Day,” from President Obama at his last press conference are just not a substitute for knowing how many people have enrolled in the plans in the various Exchanges, and more importantly, have paid for coverage. What are their ages? How about some real numbers as a Holiday present?

Second, the Obama administration is acting as if a large number of enrollees in the aggregate is the measure of success. This is simply not true. Putting aside the problem of it being paying customers rather than mere enrollment that ultimately matters, meeting or exceeding projections in some states does not compensate for deficiencies in many other states. Because the pools are state-based, Texas insurers and insureds are not helped if enrollment in New York or Connecticut exchanges ultimately equals or exceeds targets. The insurance market in Texas and many other states will still be unstable with some insurers likely pressing for significant premium increases, contemplating withdrawal from the Exchanges, and demanding larger subsidies from the federal government via Risk Corridors and other programs.

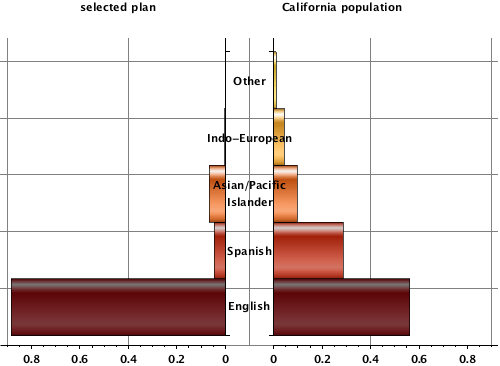

Third, even those who have been on the more pessimistic side of matters, must acknowledge that there has indeed been a surge in many state Exchanges and in many states covered by the federal Exchange. On December 11, I wrote: “With a decent last minute kick, it is not unimaginable that California could make 1/3 of its total by the December 23, 2013 deadline and get closer to its ultimate goal by the end of March.” With enrollments at 17,000 per day, California may in fact be there. Colorado, which previously had dismal enrollment numbers, reports 33,356 enrolled as of Monday, which puts it at of the 136,000 projected enrollment for 2014 and 52% of the way towards the Obama administration’s projections for this time of the open enrollment season. (33356/(0.47 x 136000)). Other states such as New York and Connecticut, which previously were doing better than most, have also reported a high pace of enrollment.

Whether that surge has been as large in many other states remains to be seen. Proponents of the ACA like to cherry pick their states with at least as much zest as opponents do. Perhaps both sides share the belief that insurance enrollment is at least much a social phenomenon as a purely economic one. Numbers for large states (with large numbers of uninsureds) such as Texas, Florida, Georgia, Indiana, Illinois, North Carolina and Florida have yet to report any numbers that I have seen. And, as mentioned above, even if California and New York and some other states have enrollment sufficient to forestall premium instability and possible entrance into an adverse selection death spiral, that will not greatly help states in which enrollment ends up being less than half of that projected.

Finally, we need to look beyond the last minute holiday rush for health coverage and see what happens between now and March 31, 2014. The carrot of the ACA has basically been eaten for 2014. If you wanted health care coverage and could afford the prices on the Exchange it made little sense to wait until after the December deadline to acquire it. This is all the more true given that the President has permitted people to game the system by simply enrolling in a plan now and deciding until January 10, 2014, whether to pay.

Now, however, the first surge is likely over. Will there be the needed second surge? All that really remains is the stick: the individual mandate tax penalty. Many people, including me, believe that even before the events of last week, it was too small in 2014 to achieve its goal of inducing enrollment by those in good or average health. The number of people for whom insurance would not be a good deal at, say, $2,000 a year net but for whom it would be a good deal at (effectively) $1,705 per year ($2,000 – the $295 per person tax penalty) is not likely to be enormous. This is so because ACA premiums often depart greatly from actuarial risk by their prohibition on medical underwriting, accurate age rating, gender rating and their — shall we say — loose enforcement of tobacco rating.

Moreover, with the administration exempting last week upwards of half a million people from the individual mandate, the number of people who need fear the stick got even smaller. So, yes there are mega-procrastinators or people who have been stymied by the dysfunctionality of various Exchange website in obtaining coverage. There are former skeptics who see their neighbors helped by health insurance coverage under the ACA and who now enroll just as there may be some turned off by whatever problems emerge in administration of the plans. On balance, I would not be surprised to see modest increases in enrollment between now and the middle of March. I remain highly skeptical, however, that there will be a second surge equivalent to what has occurred this past week. As they say, however, only time will tell.

Personal Note

I am enjoying a family vacation in the Colorado mountains this winter holiday. It’s snowing outside my window as I write this and the beauty of a quiet snowfall can eclipse what may seem so important at other times. So please continue to read ACA Death Spiral periodically, but don’t expect a huge amount of activity for about the next week. I’m confident we’ll be back exploring issues in the new year.