In testimony before Congress last June, I think I may have shocked some Representatives by estimating that insurers selling policies on the individual exchanges as part of the Affordable Care Act would be sufficiently unprofitable that they would get only 37% of what they would have received under the Risk Corridors program had the federal government not required that the budget for that program be balanced. It turns out, however, that my gloomy estimate was, in fact, wrong — but only because it was far too cheery. In fact, according to data released yesterday, insurers will receive only 12.5% of what they thought at one time they would receive. There is a $2.5 billion shortfall between the money taken in under that program from profitable insurers and the money now owed to those who lost money, at least as the government measures it.

The shortfall spells trouble for Obamacare in a number of ways. And it is difficult to overestimate how troubling this development should be for supporters of that program.

Some Exchange insurers are likely in serious trouble

First, it likely means that some of the smaller insurers who, at least before passage of section 227 of the Cromnibus bill last December, had anticipated receiving full payment for the money the government owes under the Risk Corridors program, are going to find themselves with a serious cash flow problem. Some may even find themselves with solvency problems given the improbability that the full amount of the Risk Corridor obligation will ever be paid. Companies that had booked Risk Corridor payments as receivables valued at 100% of the face amount, may have to start writing off at least part of them off as uncollectable. Thus, when CMS says that the government’s inability to pay 87.5% of what it owes may create “some isolated solvency and liquidity challenges,” that is likely an understatement. Fortunately, as the Wall Street Journal reports, some insurers apparently saw the handwriting on the wall and accounted for the Cromnibus limitation properly so as not to deceive shareholders or state regulators.

Bad news for Exchange premiums

Second, it augurs severe pressure on insurance pricing in the healthcare exchanges. The reason that there is a $2.5 billion shortfall is that a lot of insurers lost a lot of money selling policies on the Exchanges during 2014. Insurers, like other businesses, have this habit of trying to make up for past losses by charging more in the future. So we will see later this month some of the effect when the Obama administration releases data on premiums for 2016, but the massive losses in 2014 shown by the Risk Corridors results is likely to add to pricing pressures.

The Obama plan to rescue insurers has failed

Third, it shows that broken promises have consequences. Let’s go through some history here. Remember the infamous promise, “if you like your healthcare plan, you can keep it. Period.”? That was, of course, not exactly true in light of what the statute actually said. And, when Americans saw their policies cancelled as a result, the Obama administration decided it would delay and relax enforcement of the various provisions of the ACA that would have killed enough many non-Exchange insurance plans.

But this refusal to salvage the political rhetoric by sacrificing the language of the statute got many insurers angry. The insurershad priced their policies on the assumption that of course the Obama promise was the usual political moonshine and that those healthy insureds previously owning now non-compliant policies would migrate their way over to Exchange policies and stabilize that market. In true Cat in the Hat Comes Back style, the Obama administration “solved” that problem, as I explained twice (here and here) in December of 2013, by fiddling with the accounting rules in the Risk Corridors program by making it more difficult for insurers to be deemed to have made sufficient money to owe the government and making it easier for insurers to be deemed to have lost money and thus be owed money by the government. (Although its pronouncements were a bit cryptic, as I noted last April, the CBO may have estimated that the cost of this gimmick was as much as $8 billion). Now, however, with the Cromnibus bill prohibiting the Obama administration from dipping into unspecified accounts to pay for Risk Corridors, which I guess is what they planned since no money was ever appropriated for the program, that last bit of multi-billion tinkering has backfired. Insurers will not be paid for Risk Corridors for a long time if ever and, thus, they have indeed suffered a significant loss of a chain of make-it-up-as-you-go-along policies designed to salvage the ACA.

Don’t trust government accounting

Fourth, the Risk Corridors deficit exposes as pure bunkum the statements of many in Washington in the post ACA era — and continuing even today — about the state of the insurance market and the Risk Corridors program. Recall that at one point not too long ago the CBO was asserting that the Risk Corridors would actually make the government $8 billion. This was done, perhaps not coincidentally, after an effort by Senator Marco Rubio gained prominence to defund Risk Corridors as an insurance industry bailout. Devoted readers may also recall that I found the CBO’s estimate “baffling,” a bit of cynicism whose sagacity may have improved with age. And even today with the announcement, officials at CMS repeated the technically correct and yet practically dubious notion that, yes, there were shortfalls today, but Risk Corridor payments made by insurers in 2015 and 2016 might be enough not just to overcome the 2014 deficit now valued at $2.5 billion but also to make whole insurers who lost money in 2015 and 2016.

And the plea to undo Cromnibus

It is no wonder that former CMS head administrator Marilynn Tavener, now speaking for the America’s Health Insurance Plans, is now saying it is “essential that Congress and CMS act to ensure the program works as designed and consumers are protected.” By “as designed, Ms. Tavenner means before Cromnibus when Congress, in a spasm of fiscal responsibility, required that Risk Corridors, for which no money was ever appropriated, actually pay for itself just like the Risk Adjustment program. Translation of Ms. Tavenner: find someone else’s money somewhere to bail out insurers who lost money in the Exchanges.

A key feature of the Affordable Care Act are the “SHOP Exchanges.” These are markets established by either a state exchange pursuant to section 1311 of the ACA or the federally facilitated market (FFM) pursuant to section 1321 of the ACA in which employers with fewer than 50 full time equivalent employees can purchase health insurance for their workers. They can do so without being subject to either rating based on the projected health of those covered or “experience rating” in which premiums are tied to health expenses in prior years. SHOP exchanges are intended to be a mechanism whereby the burden of providing healthcare can remain where some people (not me) believe it belongs: with the employer.

To date, the key feature of the SHOP exchanges has been their complete failure to attract customers. A GAO report issued in November, 2014, said that only 76,000 individuals—including employees, their spouses, and dependent children— had enrolled in SHOPs operated by a state and, although the data was, amazingly enough, not available from the federal government for the remaining states whose marketplace it operated, enrollment had apparently followed a similar dismal pattern. This is in stark contrast to yet another stunningly wrong forecast of the Congressional Budget Office, which, as late as April 2014, had made forecasts that tax credits under section 45R of the Tax Code would cost $1 billion for 2014, an estimate that implies enrollment by more than a million, persons in the SHOP exchanges.

There have, of course, been multiple explanations of the failure of the SHOP exchanges in 2014. As has been well documented, the computer systems for the Federally Facilitated Marketplace (FFM) simply did not work. Applicants thus had to resort to more primitive paper processes. Second, the transient nature of a tax credit offered to some SHOP purchasers may have been insufficient to attract buyers, some of whom likely feared it would heighten expectations among employees of employer provided coverage that would be difficult to sustain in two years when the tax credit expired. And a variety of other explanations have been offered ranging from insufficient advertising to competition from non-SHOP-exchange markets, to difficulties with use of traditional intermediaries in the new market.

But perhaps, as some have noted, the basic problem is that it purchase of policies on a SHOP exchange at full or close-to-full price just doesn’t make doesn’t make a lot of economic sense when it appears that most employees could otherwise qualify for a taxpayer funded subsidy if they purchased similar policies on the individual exchanges. If small employers have the funds to help their employees more and want to help them meet medical expenses, perhaps the best medicine would be green: cash. Such a choice would have the fringe consequence — perhaps fringe benefit — of pushing more healthy people into the individual exchanges thereby reducing the risk of an adverse selection death spiral. It might also have distributional consequences that many would regard as an improvement. One can thus see the seed of bipartisan support for repeal of this provision.

The rest of this entry explores this proposition using four sample scenarios. Given that employees can purchase policies on the individual exchange that, at least for now, will be subsidized by the federal government in many instances, does it make sense for benevolent employers to provide health insurance or to instead, give workers higher wages, and let them choose to purchase policies that may be subsidized on the individual exchange?

Executive Summary

Several factors matter in determining whether it makes sense to SHOP from the perspective of an employer and employee:

1. How much of a subsidy, if any, is the employee entitled to if it purchases a policy on the individual exchange. This may in turn depend not just on the compensation the employer pays the employee but also on the size of the employee’s household and sources of income of other household members. The higher the subsidy, the less generally it is in the interest of the employee that the employer purchase coverage through the SHOP exchange.

2. Would the small employer be eligible for a tax subsidy under section 45R of the Tax Code (section 1421 of the ACA).?These subsidies can range up to 50% of premiums. Generally, the higher the 45R subsidization rate, the greater the possibility that it is in an employee’s interest that the employer purchase coverage through a SHOP exchange rather than provide the employee with cash.

3. How do premiums in the individual market match up with premiums in the SHOP market for comparable policies. Many supposed that SHOP market policies might be cheaper and provide an advantage to employer purchase. But to the extent there are no such savings or, as perhaps is turning out to be the case, SHOP policies are more expensive, the case for having a SHOP exchange option is weakened.

4. To what extent do the preferences of the employer about which plan to select (Metal Levels and Plan Types) match the preferences of the employees. To the extent the fit is poor, that is factor suggesting that benevolent employers do better to avoid the SHOP exchange and instead give their employees cash so they may do as they see fit.

If it turns out that few employees benefit from the existence of the SHOP exchanges or that its distributional consequences are not sensible, the case for simplifying the Affordable Care Act by elimination of this component makes some sense.

Examples

Here are the families in the scenarios: Dora, the Dursley family, James and Mary, and Ada.

Example 1: Dora

Consider Dora, a 40 year old single woman making $27,195 per year working for a business Exploration, Inc. , that employs 40 full time equivalent workers and is thus ineligible for any sort of section 45R subsidy. For concreteness, we’ll put Dora in Harris County, Texas (Houston). If Exploration, Inc. goes to the SHOP marketplace for 2015, it will find that the second cheapest silver plan is sold by Blue Cross for $400 per month ($4,800 per year) for a single person age 40. The policy features a $3,000 all-inclusive deductible and a $6,350 all-inclusive out-of-pocket limit. So, if Exploration, Inc. were to purchase this policy, Dora would have health insurance and no additional tax liability as a result.

Suppose that in lieu of paying $4,800 in premiums to buy health insurance for Dora, Exploration just raises Dora’s wage by $4,800 . Call this her gross “in lieu compensation.” Assuming Dora is in the 15% marginal tax bracket, she would actually receive $4,080 of in-lieu compensation from her employer. If Dora then went to the federally facilitated marketplace for Texas, Dora would find that she could purchase an essentially identical policy from Blue Cross with the same deductible and out-of-pocket limit for $363.60 per month or $4,363 per year as a gross premium. But, at least until a decision against the Obama administration in King v. Burwell throws the nation into chaos , Dora would be eligible for a small subsidy from the federal government of $15.22 per month since the second cheapest silver plan in her area (a “Blue Advantage Silver HMO”) costs $250 per year. Dora’s net premium would thus be about $4,181.

Thus, to be in almost exactly the same position as would have been had Exploration purchased a policy on the SHOP exchange, Dora would be out a net of $101. Maybe, at least for Dora, its marginally in her interest if her employer goes SHOPping.

Dora accounting

But this small negative sum may well be offset by a benefit Dora receives as a result of Exploration not going to the SHOP exchange and not buying health insurance for its employees: freedom. Freedom could help Dora in a variety of circumstances.

Suppose, for example, that Dora is in great health, has some money saved up, and just wants a Bronze policy to cover her against catastrophic medical expenses. Now Dora can go to the Exchange and pick up a Blue Cross Bronze “Blue Advantage Bronze HMO” policy for just $191.03 per month gross and about $176.03 per month after her subsidy. After she pays this net premium and her taxes on the $4,800 she got from her employer, she’ll have about $1,970 left in her pocket. If her medical expenses for the year end up being $4,970 or less for the year she’s come out ahead relative to where she would have been under the hypothesized Silver policy purchased by Exploration.

Or, suppose Dora isn’t in such good health and doesn’t like the risk created by a silver plan. She wants a platinum plan. She could obtain the “UnitedHealthcare Platinum Compass 250” plan with a deductible of just $250 and a out-of-pocket limit of $1,500 for a gross premium of $328.91 per month or $3,947 per year. The net premium for the policy after consideration of subsidies would be about $3,764 per year. She could buy this with the extra compensation she received from Exploration Inc. and still have $316 left over. If her medical expenses ended up being very low or somewhere between $1500 and $6,350 she will end up ahead.

Example 2: The Dursley Family

Vernon Dursley is the 40-year old Vice President Grunnings, a small drill manufacturer in Potter County, South Dakota. His family consists of his 40-year old wife Petunia and his young son Dudley, who is diabetic. Grunnings employs 15 individuals full time who have an average annual wage of $23,000. Dursley himself earns $90,000 per year. If Grunnings went to the SHOP exchange operating by the FFM for South Dakota, it would find a Bronze plan, “Sanford Simplicity-$3,000” available at a gross premium of $716.05 per month to cover the Dursley family. Because, however, Grunnings employs fewer than 25 people and pays a low annual average wage, it is eligible under section 45R of the Tax Code (section 1421 of the ACA) for a federal tax credit for one third of the amount of such purchases. Thus, the amount Grunnings would save by not purchasing the policy — at least with respect to Mr. Dursley — is $477.37 per month or about $5728 per year.

Giving Mr. Dursley $5,728, will not, however, be enough to enable him to purchase comparable coverage for his family on the FFM for individual policies for South Dakota. He is not eligible for a subsidy because his income is more than 400% of the applicable federal poverty level. First, the Dursley’s marginal tax rate is likely to be 25%. Thus, he will not net $5,728 from the Grunnings bonus; he will net $4,296. The least expensive Bronze policy for the Dursleys would be the “Dakota Reserve 6000” for $558.58 per month or about $6,703 per year. Thus, the Dursleys would be about $2,407 worse off if Grunnings failed to purchase a SHOP policy.

Dursley accounting

The underlying reason that the Dursleys do better if Grunnings SHOPs is that that Mr. Dursley is a well compensated employee of a company that is eligible for a tax credit if it goes to the SHOP exchange. Thus, even if premiums in the individual market are a little lower for comparable benefit packages as they are in the SHOP market, that benefit ends up being overwhelmed by the differential tax treatment.

Example 3: James and Mary

This example is somewhat more complicated but it is also quite important.

James is a 60 year old worker in medium health working for Peaches Unlimited in Peach County, Georgia. He’s married to his 60 year old wife, Mary. His household makes $50,000 per year. Peaches, which has 30 full time equivalent employees, has considered going to the SHOP Exchange and providing Bronze coverage for its employees and spouses, paying for all of the employee’s premium expenses and for half of the spouses. When it does so, it finds one plan: “BCBSHP Bronze Pathway X Enhanced 5000 30 6600 Plus” a POS (point of service) plan from the Georgia Blue Cross/Blue Shield carrier. The premium attributable to a 60 year old couple is $14,652. But Peaches will only pay half the premium for spouses, so, if Peaches were to purchase this policy, the annual incremental cost attributable to James and Mary would be $10,989. For this, James and Mary would get a plan with a $10,000 deductible for medical expenses, an additional $1,000 deductible for drugs, and a $13,200 out-of-pocket limit. If they wanted the policy, however, James and Mary would have to cover half of Mary’s premium, which would add an additional $3,663 to their costs. So, if we are to compare apples to apples, we need to see what James and Mary’s financial position would be if they shopped instead on the individual exchange.

Suppose that Peaches gives James and Mary $10,989 in in lieu compensation. They would likely have a marginal tax rate of 15%, which would make their after-tax additional compensation about $9,341. If James and Mary try to acquire a matching plan, the closest it looks they can come is the Humana Bronze 6300/National POS – OpenAccess plan, which has a gross premium of $1,181 per month or a hefty $14,177 per year. The net premium, however, will be only $5,578 after premium tax credits are received. Thus, James and Mary will be able to take the $9,341 in after-tax compensation they received, pay $5,578 and have $3,762 left over. But it’s better than that. James and Mary won’t have to pay $3,663 for half of Mary’s policy. So, in fact they will be $7,426 better off and Peaches no worse off if Peaches does not go to the SHOP exchange. For a couple making $50,000 that is a lot of money.

James and Mary accounting

How has this happened? It is the result of three factors coming together: (1) James and Mary being eligible for a large subsidy from the federal government due to their age and the consequent high cost of a silver policy; (2) Peaches having too many employees to be eligible for any sort of tax benefit from the government; and (3) the high price of SHOP policies in Peach County relative to individual policies. As shown here, when these factors come together, employees should prefer a situation in which employers give them cash, not expensive health insurance policies. Moreover, if Peaches does not go to the SHOP exchange, James and Mary are no longer wedded to the likely small number of plans Peaches wants; they can pick any plan that best meets their needs available in the individual exchange.

Ready for one more?

Example 4: Ada

Ada is a 30 year old programmer at Babbage Enterprises , a small tech firm in Allegheny County, Pennsylvania. It has 10 employees but their average wage is $75,000 per year, making Babbage ineligible for any section 45R tax credit. Ada is single and makes $100,000 a year. It believes employees should have the best health care available. Babbage, which has a CEO with recurrent heart problems, could go to the SHOP Exchange and purchase a Platinum PPO for its employees — the “UPMC Small Business Advantage Platinum PPO $250 $10/$25 – Premium Network” for which the cost of adding Ada would be $353.94 per month or $4,247 per year. For that Ada would receive a plan that had a unified $250 deductible and a unified $1,250 out-of-pocket limit.

But what if Babbage instead provided Ada with $4,247 in additional compensation? Ada could go into the FFM for Pennsylvania and find a policy similar to the UPMC one listed above. She could get the “UPMC Advantage Platinum $250/$20 – Premium Network” for a gross premium of $391.75 per month ($4,701 per year )with a unified $250 deductible and a $1,500 out-of-pocket limit. Ada would have to dig into her own pocket to do so, however. Because Ada is in likely in the 25% marginal tax bracket, she will net only $3,185.25 from the additional compensation. And, because Ada’s income is well above 400% of the federal poverty level, she will receive no advance premium tax credit to help pay for the policy. Thus, Babbage’s decision not to purchase on the SHOP exchange will end up costing Ada about $1,516 if she wants a comparable policy.

Ada accounting

Ada is worse off largely because she gets no subsidy and because, by receiving cash instead of health insurance, she loses the current tax advantage offered by the latter. Thus, it is the wealthy individual who is hurt by having to go to the individual market.

Provisional Conclusion

All of the above is hardly a proof. There are lots more scenarios to be considered. But my initial conclusion is that the SHOP exchanges tend to be most useful only for the wealthy who would not get a premium tax credit were they to go to the individual exchange. Also since my preliminary research indicates that, on balance, SHOP policies are at least as expensive as individual policies and because the employer purchasing a SHOP policy generally ends the ability of the employee to get a subsidized policy on the individual exchange, the option to purchase in fact may hurt employees and their families.

So, we have to ask.: If we are going to keep some version of Obamacare, why not help stabilize the individual exchange pools by bringing some additional people into them: the generally healthy people who work for small employers.? So long as the market works and those employers pass on to their employees what they would have spent on the SHOP exchange for health care, most except the wealthiest are likely to be better off. Although one answer to this provisional suggestion is that doing so will hurt the federal budget — more people will get section 36B tax subsidies — there may be many who share the preference for a simpler Obamacare, and one that helps breaks the peculiar stranglehold that employer provided health insurance has had on this nation since the government distorted the market after World War II.

The Congressional Budget Office issued a report this week revising its February projections of the cost of the Affordable Care Act. Although there is much to discuss regarding the report, I want to focus here on its troubling discussion of “Risk Corridors.” That’s the part of the law under which the federal government reimburses insurers selling policies on the new Exchanges for sizable fractions of their losses. It also taxes insurers if they happen to make money selling policies on the new Exchanges. Between February and April, the CBO estimated cost of Risk Corridors jumped $8 billion. In February, Risk Corridors were predicted to make the government a net of $8 billion over the three years of the program. Now, Risk Corridors are expected to net the government nothing. The CBO claims that this jump was caused by regulations issued by the Obama administration in March that drove up the cost of the program.

There’s a second explanation, however, for the $8 billion change between February and April that’s possibly more troubling. This past February I wrote a blog entry with a lot of math explaining that the CBO prior analysis of the Risk Corridors provision was baffling and rested on extremely dubious and factually unsupported assumptions about the profitability of insurers selling on the Exchanges. That error, if it was one, was particularly salient because it ended up forestalling growing efforts within Congress to repeal Risk Corridors as an unwarranted “bailout” of the insurance industry. Could it be that with the repeal threat gone, CBO is now using the “noise” created by an Obamacare regulation as cover for rectifying the unduly optimistic assumptions it made back in February regarding Risk Corridors? That would be very troubling, because while math errors merely challenge the CBO’s competence, the alternative behavior about which I am speculating here goes to something more important: the CBO’s integrity.

The CBO explanation means the Obama administration shoveled $8 billion to insurers through a regulatory “tweak”

The official explanation from the CBO on its change of $8 billion in the cost of Risk Corridors is as follows:

“In March 2014, the Department of Health and Human Services issued a final regulation stating that its implementation of the risk corridor program will result in equal payments to and from the government, and thus will have no net budgetary effect. CBO believes that the Administration has sufficient flexibility to ensure that payments to insurers will approximately equal payments from insurers to the federal government and thus that the program will have no net budgetary effect over the three years of its operation. (Previously, CBO had estimated that the risk corridor program would yield net budgetary savings of $8 billion).”

So, if the CBO is to be believed, the change isn’t due to any earlier error, but due to an administration regulation promulgated by the Obama administration that has resulted in a net of $8 billion more going to insurers. That’s a big change for several reasons. First, it means that the regulatory changes instituted by the Obama administration cost the federal government $8 billion. All of that money went to the insurance industry. And so, in March of 2014, without much fanfare, the Obama administration would in effect have written a check to the insurance industry for $8 billion. That payment would only have been motivated by one thing: a desire to keep insurers pacified and in the Exchanges after having deprived them of perhaps their most healthy potential insureds by a prior administrative ruling — in violation of the ACA — that insurers could keep selling non-compliant policies. The $8 billion would thus have been “damages” paid by the taxpayer in order to permit the President to honor his campaign promise that if you liked your insurance plan you could keep it.

In short, if you believe the CBO, a regulation for which statutory support will be extremely hard to find, resulted in the government shoveling $8 billion to insurers, basically to pacify them for the losses they suffered as a result of further regulatory changes of dubious legality. The Obama administration can not afford to have its signature program enter a death spiral as a result of regulatory actions that, while mollifying those who otherwise would have lost their health insurance coverage, caused insurers to lose more money in the Exchanges. And, again, the Obama administration did so in a clever way that made it difficult for anyone to have legal standing to challenge them. So far as I can discern, no insurer will be worse off as a result of the March 2014 regulatory changes. The real victims are taxpayers with diffuse interests and, of course, the Rule of Law.

The CBO math is still baffling

A second reason the change by the CBO is big comes from a look at the math. As I said in my February 2014 post calling the CBO February report “baffling,” consider the implications of asserting that the insurers would make so much money on the Exchanges that they would, on net owe the federal government $8 billion. If you do the math, it means that the CBO assumed that, over the course of three years, insurers would be earning about 8 cents on every dollar they earned via policies sold on the Exchanges. I just ran the numbers again and came up with a very similar conclusion: the earlier estimate could only be true if insurers were supposed to make a hefty 8% or greater return on premiums. That estimate of 8 cents on the dollar was really peculiar at the time because enrollment — let alone actually paying customers — was running seriously behind projections and the number of “young invincibles” was particularly low. Low overall insurance purchases and particularly low rates of purchases by the people who were most needed in the Exchanges caused many people to believe back in February that insurers would hardly make hefty profits and pay money to the government under Risk Corridors. Instead, they thought insurers would fare poorly and probably have to be subsidized (or “bailed out”) by the government.

The effect of the February CBO pronouncement was to dampen enthusiasm for a bill proposed by Senator Marco Rubio that would have repealed the Risk Corridors provision as a bailout to the insurance industry. If, after all, the federal government was, on balance, making money on Risk Corridors, it was hard to see it as a “bailout” to the insurance industry. Whether intended or not, the political effect of the February CBO announcement was to pull the rug out from one justification for repeal of Risk Corridors.

But is it even plausible to believe that the regulatory change made by the Obama administration in March without the approval of Congress could cause such a large change in the Risk Corridors program? I have done the math again and the answer is no. I do not see how it is possible to get $8 billion out of the regulatory tweak that was made. Again, the calculations are baffling.

Here’s how we know. The $8 billion the CBO thought back in February the government would make off of Risk Corridors represents about 4% of the premiums insurers on the Exchanges would take in during that time period. One can use that and other information from the CBO to reverse out a distribution for “allowable costs” (basically claims expenses) We can thus make a respectable estimate of how many insurers would make money on the Exchanges, how many would lose, and how much these insurers would gain and lose. I describe the gory process in my post from February. Call this distribution the CBO Insurer Profitability Distribution. Then assume the government tweaks, as it did, two regulatory parameters used in the computation of Risk Corridor payments, changing something called a profit margin floor from 0.03 to 0.05 and changing an “administrative cost cap” from 0.2 to 0.22. If one then takes the CBO Insurer Profitability Distribution and computes how much the government would now make on Risk Corridors does one emerge with the CBO’s new prediction that Risk Corridors will produce no net revenue? No! One gets that the Risk Corridors program now generates about 2.8% of premiums for the government. In other words, the reduction in Risk Corridor revenue resulting from the administrative tweak is only 1/3 of what the government claims.

The easier way to reach the CBO’s April’s conclusion is to assume that the gain of $8 billion resulted from two phenomena: (1) the regulatory tweak mentioned by the CBO and discussed above, but (2) a recognition that the CBO Insurer Probability Distribution the CBO had used in February was, as I have said, wrong. If, for example, one assumes that insurer claims were about 6% higher than the CBO estimated in February, the regulatory tweaks combined with higher insurer claims expenses indeed generate an $8 billion shift in the amount of revenue the government would make on Risk Corridors.

For those interested in the details, I link here to a Mathematica notebook showing the computations; I try to avoid black boxes.

Conclusion

So, what are we to make of this apparent discrepancy between the CBO’s explanation of its change in estimates and the actual effects of the regulatory changes it asserts to be the cause ? It could, I suppose, be my mistake. I have been careful and consider myself pretty knowledgable in this area, but I will hardly claim to be mathematically infallible. The problem is that the for ordinary Americans (like me), the CBO is a black box. It is not subject to the Freedom of Information Act and it does not publish enough of its methodology for even experts in the field to figure out what it is doing. That, I would submit, is a real problem for the democratic process, where the fate of legislation depends essentially on trust rather than the Reagan doctrine of “trust but verify” (doveryai no proveryai, in the original Russian).

It could also, however, be a coverup for a mistake (or worse) back in February. There is, after all, an alternative explanation of the change in estimate. It was unrealistic all along for the CBO to think that insurers in the Exchange were going to make money on balance. That’s what I suggested in my February 2014 post. So, rather than admit that the it had been guilty of unwarranted optimism, the CBO simply used a new distribution of likely claims expenses, came up with a different answer, and used the March 2014 regulatory changes as a smokescreen.

I will confess, however, that I am very uncomfortable with conspiracy theories or with theories that are premised on people acting in bad faith. Nonetheless, I would not find it impossible to believe that a culture could emerge in a politically sensitive agency that was reluctant to expose forcefully the consequences of government programs that proved far more expensive and far less successful than forecast originally. It would be a culture in which good news, or optimistic speculation, was uncritically embraced. What I challenge the CBO to do, therefore, not only with the Risk Corridors analysis, which is but the tip of a very big iceberg, but with the entirety of its ACA analysis, is to open it up for scrutiny. When government policy is essentially set on the basis of models that are not subject to peer review or public scrutiny, there is a great chance for error and, frankly, for manipulation. Government by black box breeds suspicion.

Postscript: Is the tweak legal?

I have said before and I say again that the regulatory tweak that the CBO now says will cost the federal government $8 billion is extremely dubious. It’s an extremely sneaky way of sending money to the insurance industry, resting, as it does, on arcane manipulations of mathematical formulae. And I have serious doubts that the changes are authorized by Congress.The submission of the original regulations in March, 2013 says that essentially all commenters agreed that a 3% margin for profit was appropriate. No commenters indicated at that time that insurers were entitled to a higher imputed rate of return on capital. No one said anything about 5%. Back in March of 2013, HHS thought 3% was the right number. There has been no fundamental change in the capital markets since that time. The only thing that has changed is that the Obama administration has made the pool of insureds making purchases in the Exchanges less healthy on average. The regulatory “tweak” moving the profit margin from 3% to 5% is thus not consistent with the original goal of Congress for the Risk Corridors program, but is simply a way of compensating insurers for another regulatory change.

The change in the administrative cost cap from 20% to 22% that will likewise result in higher payments to insurers is likewise dubious. The reason 20% was suggested in the original July 2011 proposal and chosen in the March 2013 regulations was to maintain parity with regulations governing the “Medical Loss Ratio” codified at 42 U.S.C. § 300gg-18 as part of the ACA. The idea, which was apparently supported by commenters on the original rules, was that if insurers — even small group and individual insurers — could not claim more than 20% administrative costs without owing rebates pursuant to section 10101(f) of the ACA then they should not be able to claim more than 20% administrative costs under the Risk Corridors provision. Makes sense! But, again, nothing has changed. There is no indication that anything President Obama did that raised the administrative costs of running a health insurance plan on the Exchanges. There is no indication that any factor in the real world (such as the cost of computers or paper) increased the administrative costs of running a health insurance plan on the Exchanges. The limits for the Medical Loss Ratio computation have not changed. There is no better reason now then there was a year ago to let the cap on administrative costs be higher for Risk Corridors than it is for Medical Loss Ratio. And, yet, it is now 22% instead of 20%. The only reason it has changed is to provide a vehicle for shoveling money to insurers.

Again, unless one thinks that the goal of keeping insurers in the Exchange is so overwhelming as to permit the Executive Branch to do anything, it is difficult to see a conventional, lawful justification for the regulatory change that results, according to the CBO, in $8 billion of compensation to the insurance industry. And I say that believing fully well that many of the Obama administration’s other regulatory changes — also of dubious legality — such as expanding the hardship exemption and permitting insurers to sell policies off the Exchanges that contain prohibited provisions have significantly hurt insurers selling policies on the Exchanges. Two wrongs do not make a right.

Technical Appendix

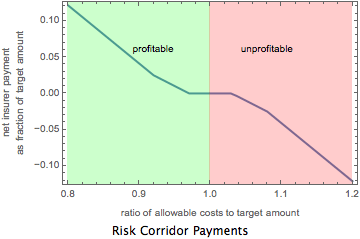

The following graphic shows the relationship between the Risk Corridor Ratio and the net receipts of the government for each premium dollar. As one can see, the higher the Risk Corridors Ratio, the less money the government receives or, in some instances, the more money the government pays out.

The following graphic compares the relationship between claims costs (“allowable costs”) incurred by an insurer as a percentage of premiums and the Risk Corridors Ratio. It does so for two sets of regulatory parameters. It first uses the regulatory parameters that were in place prior to March of 2014 (3% profit margin and 20% administrative cost cap). It next using the new regulatory parameters (5% profit margin and 22% administrative cost cap). As one can see, the regulatory changes increased the Risk Corridors Ratio for all levels of allowed costs and thus decreased the amount the government would receive from insurers (or increased the amount the government would pay to insurers).

The Congressional Budget Office just issued a report that assumes the Affordable Care Act system of individual policies sold in Exchanges without medical underwriting can remain relatively stable. Tightly bound up with that assumption is its prediction about a controversial ACA program known as “Risk Corridors” that requires profitable insurers to pay the federal government up to 80% of profits they make on policies sold on the Exchanges but that also requires the federal government to pay insurers up to 80% of the losses they suffer from policies sold on the Exchanges. The CBO now believes it has enough information to predict that Risk Corridors will actually make money — $ 8 billion over three years — for the government at the expense of insurers.

This CBO prediction of $8 billion in federal revenue, which has gained much publicity, pulls the rug out from critics of the ACA such as Senator Marco Rubio who have introduced legislation that would repeal Risk Corridors as an insurance industry “bailout.” Such a blunting of Senator Rubio’s proposed repeal legislation is crucial in the ongoing battle over the ACA because repeal of Risk Corridors could result in insurers (who just might not believe the CBO’s numbers) exiting the Exchanges for fear of having no government protection against losses resulting from unfavorable experiences in the new market the government has created. On the other hand, if the CBO is just getting its number wrong, Rubio’s case for repeal of Risk Corridors remains as strong (or problematic) as it ever was. The CBO projection is also important because Risk Corridors nets the government money if and only if the ACA works, insurers are able to make some profits, and a death spiral never takes hold. And this, as readers of this blog are aware, is a prediction about which many have serious doubts.

Here’s the short version of the rest of this post.

I’ve done the math and I don’t see how the CBO is getting this $8 billion number unless it is assuming either very high enrollment in policies covered by Risk Corridors or very high rates of return made by insurers. Or it made a mistake. I don’t think the CBO’s own numbers support very high enrollment in policies covered by Risk Corridors and I don’t believe either an emerging reality or the CBO’s own rhetoric justify assuming very high rates of return. So I think the CBO ought to take a second look at its prediction. People should not yet make policy decisions based on the CBO estimate.

Reader, you now have a choice. I’m afraid that the next several paragraphs of this post become very technical. It’s kind of forensic mathematics in which one attempts to use statistics and numerical methods to deduce the circumstances under which something said could be true. If that sounds dreadful, scary or tedious, I would not protest too loudly were you to skip ahead to the section titled “How could I be wrong?” Before you leave, however, realize that what I am attempting to accomplish in the part you skip is a form of proof by contradiction. I prove that if what the CBO was saying were true, then insurers would have to be making 8% profit. But nobody, including the CBO thinks they will make 8% profit, so the $8 billion number can’t be right.

On the other hand, dear reader, if you liked the Numb3rs television show (including my minor contributionsthereto) or math or detective work or just care a lot about the Affordable Care Act, the rest of this post is for you. What I am about to discuss is not only exciting math, but also the soul of the Affordable Care Act — whether the individual Exchanges without medical underwriting can remain relatively stable.

Forensic mathematics in action

Conceptually, here’s the calculation one needs to do. What we want to figure out is the distribution of insurer profits (measured as a ratio of expenses divided by premium revenues) upon which the CBO must be relying. I assume the CBO is using a member from the “Normal” or “Lognormal” family of distributions because those are typical models of financial returns and there is little reason to think that the distributions of insurer profits (expenses minus revenues) will materially depart from those assumptions. To continue reading this post, you don’t have to know exactly what those distributions are except that they look for our purposes like the “bell curves” you have seen for many years. I’ve placed a graphic below showing some normal (blue) and lognormal (red) distributions. Although it should not matter all that much, I’m going to use a lognormal distribution from here on in because the ratio of insurer expenses to premiums should never be negative and the lognormal distribution, unlike its normal cousin, never takes on negative values.

Examples of probability density functions for normal and lognormal distributions

The problem is that there are an infinite number of lognormal distributions from which to choose. How do we know which distribution the CBO is emulating in its computations? How do we know just how positive the CBO assumes the individual Exchange market is going to be on average or how dispersed insurer profits are going to be? As it turns out, the complexity of the lognormal distribution can be characterized with just two “parameters” often labeled μ (mu, the mean of the distribution) and σ (sigma, the standard deviation of the distribution). Once we have those two parameters (just two numbers), we can deduce everything we need about the entire distribution.

Now, to solve for two parameters, we often need two relationships. And, thoughtfully, the CBO has given us just enough information. It has told us how much money in total it intends to raise from Risk Corridors ($8 billion) and the ratio (2:1) between money it collects from profitable insurers and the money it pays out to unprofitable insurers. These two facts help constrain the set of permissible combinations of Risk Corridor populations (the number of people purchasing policies in plans subject to the Risk Corridor program) and insurer profitability distributions. What I want to show is that it takes an extremely high Risk Corridor population in order to get rates of return that are not way larger than most people — including the CBO — think likely to occur.

I first want to calculate the amount of money insurers would pay to HHS under the Risk Corridors program if the total amount of premiums collected were $1. Some of the payments — those by highly profitable insurers — will be positive. Those by highly unprofitable insurers will be negative. To do this I take the “expectation” of what I will call the “payment function” over a lognormal distribution characterized by having a mean of μ and a standard deviation of σ. By payment function, I mean the relationship shown below and created by section 1342 of the ACA, 42 U.S.C. § 18062. This provision creates a formula for how much insurers pay the Secretary of HHS or the Secretary of HHS pays insurers depending on a proxy measure of the insurer’s profitability. The idea is to calculate a ratio of “allowable costs” (roughly expenses) to a “target amount” (roughly premiums). If the ratio is significantly less than 1 (and outside a neutral “corridor”), the insurer makes money and pays the government a cut. If the result is significantly greater than 1 (and outside the neutral “corridor”), the insurer loses money and receives a “bailout”/”subsidy” from the government. The program has been referred to with some justification as a kind of “derivative” of insurer profitability, the ultimate “Synthetic CDO.”

The graphic below shows the relationship contained in the Risk Corridors provision of the ACA. The blue line shows the net insurer payment (which could be negative) to the government as a function of this proxy measure of the insurer’s profitability. Ratios in the green zone represent profits for the insurer; ratios in the red zone represent losses. Results are stated as a fraction of “the target amount,” which, as mentioned above, is, roughly speaking, premium revenue.

How much the insurer pays (positive) or receives (negative) under Risk Corridors as a function of a ratio-based measurement of profitability

When we do this computation, we get a ghastly (but closed form!) mathematical expression of which I set out just a part in small print below. (It won’t be on the exam). I’ll call this value the totalPaymentFactor. Just keep that variable in the back of your mind.

Excerpt of the formula for insurer total payout

I next want to calculate the amount of payments profitable insurers will make to HHS. To do this, we truncate the lognormal distribution to include only situations where the ratio between premiums and expenses is greater than 1. Again, we get a pretty ghastly mathematical expression, a small excerpt of which is shown below. I will call it the expectedPositivePaymentFactor.

Formula for expected negative insurer payments under risk corridors over a truncated lognormal distribution

Finally, I want to calculate the amount of payments unprofitable insurers will receive from HHS. To do this, we truncate the lognormal distribution to include only situations where the ratio between premiums and expenses is less than 1. Again, we get a pretty ghastly mathematical expression, which, for those of you who can not get enough, I excerpt below. I will call it the expectedNegativePaymentFactor.

Formula for expected positive insurer payments under risk corridors over a truncated lognormal distribution

The CBO has told us in its recent report that the government will collect twice as much from profitable insurers (expectedPositivePaymentFactor) as it pays out to unprofitable ones (expectednegativePaymentFactor). We can use numeric methods to find the set of μ, σ combinations for which that relationship exists. The thick black line in the graphic below shows those combinations.

Black line shows combination of mu and sigma that result in the correct ratio of positive and negative insurer payouts under Risk Corridors

To determine which point on the black line above, which combination of the parameters μ, σ , is the actual distribution, we need to use our information about the totalPaymentFactor. The idea is to realize that the totalPaymentFactor must be equal to the quotient of the CBO’s estimated $8 billion and the total premium collected by Risk Corridor plans over the next three years. But we know that the total premium collected should be equal to the mean premium charged by the Exchanges multiplied by the number of people in Risk Corridor plans. Some math, discussed in the technical notes, suggests that the mean premium under the ACA is about $3,962. And the CBO accounts for 8 million people being in Risk Corridor plans in 2014, 15 million being in Risk Corridor plans in 2015 and 25 million being in Risk Corridor plans in 2016. This means that the total premiums collected by insurers under Risk Corridor plans over the next 3 years should be about $190.2 billion. And this in turn means that the totalPaymentFactor must be 0.042.

Ready?

It turns out that of all the infinite number of lognormal distributions there is only one that satisfies the requirements that (a) the government will collect twice as much from profitable insurers (expectedPositivePaymentFactor) as it pays out to unprofitable ones (expectednegativePaymentFactor) and (b) for which the totalPaymentFactor takes on a value of 0.042. It is a distribution in which the mean value is 0.923 and the standard deviation is 0.113. I plot the distribution below. A dotted line marks the break even point for insurers. Points to the left of the break even line correspond with profitable insurers; points to the right correspond with unprofitable insurers.

Lognormal distribution of insurer profitability consistent with CBO data

Here are some factoids about the uncovered distribution. The average insurer will have expenses that are 92.3% of premiums and the median insurer will have expenses that are only 91.6% of profits. In other words, they will be making 7.7 cent and 8.4 cents respectively on every dollar of premium they take in. For reasons discussed below, this is a difficult figure to accept. It is particularly difficult in light of the pessimistic news that is emerging about things such as the age distribution of enrollees , reports from Deutsche Bank that one of the largest insurers in the Exchanges, Humana, expects to receive (not pay!) a lot of money under the Risk Corridors program, the hardly exuberant forecasts of other publicly traded insurers about the ACA, and the recent general downgrading of the insurance sector by Moody’s partly because of the ACA.

Implicit in my finding about the most likely distribution of profitability is an assertion by the CBO that 76% of insurers will be profitable under the ACA while 24% will be unprofitable. About 17% will be sufficiently unprofitable that they will receive subsidies (a/k/a bailouts) from the federal government and 9% will be sufficiently unprofitable that their marginal losses will be covered at 80%. Only 15% of insurers will be “inside” the risk corridor and neither pay nor receive under the program.

How could I be wrong?

I feel confident that I’ve done the ” gory math part” of this blog post correctly. Mathematica, which is the software I’ve used to do the integral calculus and the numeric components involved just does not make mistakes. I also feel pretty confident that I understand how the Risk Corridors program works under section 1342 of the ACA. That’s kind of my day job. And so, readers who skipped down to this part, I do believe that if the CBO were right about the $8 billion, that could only happen if insurers were, on average, earning an implausible 8% in the Exchanges.

If I’m wrong, then, it is because, except for the little issue I will mention at the end, I have made bad assumptions about the total premiums insurers expect to collect over the next three years in policies covered by Risk Corridors. That error could come from two sources. I could have the mean premium per policy wrong or I could have the relevant enrollment wrong. Let’s look at each of these.

Could I be wrong about the mean premium?

I computed the mean premium in the computation above by using data collected by the Kaiser Family Foundation on the ratio of premiums by age under most insurance plans and the typical Silver plan premium for a 21 year old (non-smoker). I then used the original forecast about the age distribution of insureds to compute an expected premium. I got $3,962. And this number seems very much in line with earlier HHS estimates, which were that mean premiums would be $3,936. So, I think I have the mean premium correct.

Could I be wrong about the number of people in Risk Corridor plans?

I computed the number of people enrolled in policies covered by Risk Corridors by looking at the CBO’s own figures. I’m not vouching that the CBO is right in its projections, but this is not the day to argue that point. The CBO now says (Table B-3, p. 109) that individual enrollment in the Exchanges will be 6 million, 13 million and 22 million respectively over the next three years. And it says that employment-based coverage purchased through Exchanges (which I assume are SHOP Exchanges) will be 2 million, 2 million and 3 million respectively. So , by addition, that’s where the figures I used of 8 million, 15 million and 25 million come from. I’m not aware of anyone else who would purchase a policy subject to Risk Corridors. Again, bottom line, I don’t think I’m doing anything wrong here.

The little issue at the end: Could ACA definitions be responsible for the incongruity?

The only other conceivable explanation of the divergence between the CBO figures and my analysis is that I am failing to take a subtlety of Risk Corridors into account. Remember, careful readers, that sentence earlier up that started out: “The idea is to calculate a ratio of “allowable costs” (roughly expenses) to a “target amount” (roughly premiums).” I stuck in the “roughlies” because the “allowable costs” are not exactly expenses and the “target amount” is not exactly premiums. When you look at the statute and the regulations, you can see that both of these terms are tweaked: basically you subtract administrative costs from both values. And you subtract reinsurance payments from expenses — but that makes sense because the insurer reduced premiums in anticipation of those reinsurance payments.

So, in the end, I don’t see why these subtleties should affect my analysis in any significant way. But I am not infallible. And I do pledge that if someone points out an error to me, I will dutifully assess it and report it.

Sensitivity Analysis

Out of an abundance of caution, however, I have rerun the numbers on the assumption that premium revenue from policies subject to Risk Corridors is 50% greater than my original estimate either because of an underestimate of per policy costs or a failure to understand that there is some additional group within Risk Corridors protection. When I do that, though, I find that the ratio of expenses to premiums is 0.943, meaning that insurers are still earning a pretty substantial 5.6%. Although that is more believable than the earlier figure of 7.7%, it is still pretty high.

Conclusion

To be honest, it makes me very nervous to say that the CBO did its math wrong or, worse, to accuse it of bad faith. These are intelligent, educated professionals and they have access to a lot more data and a lot more personnel than I do. Here at acadeathspiral it’s just me and my little computer along with some very powerful software. On the other hand, it’s not as if the CBO hasn’t been wrong before. It assumed earlier that the government would reduce its deficit $70 billion over 10 years as a result of Title VIII of the ACA (the so-called CLASS Act on long term care insurance) when many independent sources believed — rightly as it turned out — that the now-repealed CLASS Act was obviously structured in a way that could never fly. The CBO assumed in July 2012 that 9 million people would enroll in the Exchanges in 2014, a number that is now down to 6 million. And, while there are explanations for each of these changes, the bottom line is that CBO is fallible too.

So, if I might, I would strongly urge the CBO to double check its numbers and provide more information on the data it relied upon and the methodology it employed in getting to its results. I’d ask Congress, which has ongoing oversight of the ACA, to insist that the Congressional Budget Office, which is exempt from Freedom of Information Act requests from ordinary citizens, provide further detail. American healthcare is indeed too important to have policy decisions made on the basis of what could be some sort of mathematical error.

Really Technical Notes

I’m using a reparameterized version of the lognormal distribution that permits direct inspection of its mean and standard deviation rather than the conventional one, which in my opinion is less informative. The explanation for doing so and the formula for reparameterization is here.

To compute the average premium, I took the premium ratios used by the Kaiser Family Foundation, calibrated it so that a 21 year old was paying the national average payment for a silver plan purchased by a 21 year old. I then computed the expected premium over the distribution of purchase ages originally assumed by those modeling the ACA.

No more than 1% of those with household incomes between 139% and 400% and eligible to select a plan on the individual Exchanges have thus far done so. This is the information about those with middle incomes and lower-middle incomes one can derive from statistics released this week by Health and Human Services. The rate of plan selection among those with incomes over 400% of the federal poverty level is at least 3 times higher than that of persons with middle and lower-middle incomes. It could well be 4 times greater.

No matter how you fine tune the computations, I believe it is fair to say that the middle class is finding the carrots too small and the sticks too small. Some of this may be due to difficulties with the enrollment process rather than the underlying architecture of incentives under the ACA, but either way, most of those eligible to do so, are, at least for now, rejecting the benefit theoretically available to them on the individual Exchanges under the Affordable Care Act.

Visualization

Here are two figures showing the results of my calculations in more detail.

Rates of Take Up

The first graph shows the absolute rates of take up (selection of a plan) among with lower-middle and middle incomes (the lower surface) and the wealthier (the higher surface). The x-axis of the graph shows the assumption one makes about those reasonable eligible to purchase policies. When x is low, one assumes the income distribution of the eligible pool most closely resembles that of persons currently without health insurance. When x is high, one assumes the income distribution of the eligible pool most closely resembles that of persons currently with health insurance form their employer. The y-axis of the graph shows the assumption one makes about the number of persons current with health insurance from their employer who might reasonably be considered eligible to purchase insurance on a health insurance Exchange. A low value of y means that very few of these people should be considered eligible. A high value of y means that 10% of these people should be considered eligible. The z-axis (vertical) shows the fraction of people eligible to do so who have to date selected a policy on an Exchange.

Take Up Rates among the Wealthier (top surface) and the Lower Middle and Middle Income Group (lower surface)

As one can see the values are always less than 1% for the lower-middle and middle incomes. The values for the wealthier depends on the assumptions made but for all values are below 6% and is frequently below 4%. And these are values for selection of a plan, not for actual purchase of a policy. Those numbers are likely to be even smaller due to many people leaving items in their “shopping cart” without paying at the check out counter.

Take Up Ratios

The second graphic shows the ratio between the take up rates among the wealthier and the take up rates among the lower-middle and middle income group. The x and y axes are the same as before. A value of 3.4 on the z-axis means that the take up rate among the wealthy is 3.4 times what it is among the lower-middle and middle income groups. As one can again see the ratio is above 3 for almost all assumptions one could make and is frequently above 4.

Take Up Ratios

Show me the calculation

How do I get to these figures? Algebra. Some of it is very nasty algebra, but I have the world’s best computer algebra system, Mathematica, at my disposal to make the problem much easier. Rather than include the somewhat complex computations directly in this blog post, I’m going to include a PDF file showing the computations and a CDF file (a Mathematica file format). You can read the CDF file either with Mathematica itself or with the free CDF Player available here. The data, by the way comes from a combination of this tidbit of information found on page 7 of the report released by HHS on December 11, 2013, and data from the Urban Institute and Kaiser Foundation.

One of the fixes being seriously considered this week to address the “discovery” that the Affordable Care Act will not permit all people to keep the health insurance plan they may previously had in effect is H.R. 3350, a bill that would permit — though not require — insurers to continue to offer all individual insurance plans they had in effect at the start of 2013 and to treat such plans as “grandfathered” even when, perhaps, they would not be so treated under either the existing Affordable Care Act or the regulations promulgated thereunder. Unfortunately, this “Keep Your Health Plan Act of 2013” is likely to cause more problems than it solves. I also think there may be some technical problems with the bill that someone ought to think about.

The reason the Keep Your Health Plan Act will create problems is that, contrary to the rhetoric formerly used by its supporter-in-chief, the success of the Act depends precisely on many people not being able to keep their healthcare plans. And contrary to the Renaultian shock now being exclaimed by many politicians, depriving people of their existing individual health insurance plans, was part of the plan all along. Since the Affordable Care Act is an intricately woven web of provisions, it may well not be possible simply to excise one part without fatally destabilizing the remainder of the bill.

They Knew

First, as to the allegation that depriving people of their individual healthcare plans was part of the plan all along, I offer several exhibits. To set the background for the evidence, consider that a central philosophical tenet of what became the Affordable Care Act was that medical underwriting of health insurance was unfair because it punished those who, often through no fault of their own, had poor health to begin with, and created needless hardship as a result of their resulting inability to obtain efficiently delivered American-style healthcare. The “genius” of the Affordable Care Act was the notion that one could remedy this problem not just through the previously advanced — and previously rejected — idea of expanding single payor systems such as Medicare in which the government provides insurance, but in a way that preserved at least the fig leaf of a private, entrepreneurial insurance system. And the intellectual key to that alternative path of assuring insurance equality was to show, contrary to the prevailing wisdom, that private insurance could in fact function in an appropriately structured health insurance marketplace notwithstanding the absence of medical underwriting ordinarily thought necessary to prevent an adverse selection death spiral.

The Studies

The RAND studies

And studies there were that supported the idea that, with appropriate penalties for failing to purchase insurance and with a large enough pool enrolling in the nascent Health Insurance Exchanges, the market could stabilize without a fatal adverse selection death spiral taking place. Consider the various studies undertaken by the RAND corporation, one of the nation’s longest standing think tanks and one not known for being given to sentimentality. The first study undertaken by RAND in 2010 found that the number of persons in the “Nongroup” (a/k/a individual) market for health insurance would decline as a result of enactment of an ACA predecessor from the existing 17 million in 2013, to 5 million in 2014 and then down to 0 by 2016.

RAND prediction in 2010

RAND does a second study as the actual Patient Protection and Affordable Care Act (which is the same thing as the Affordable Care Act and the same thing as Obamacare) is enacted. This one is commissioned by the United States Department of Labor. As shown below, the study likewise concludes that of the 18 million they now believe will be enrolled in nongroup health insurance prior to 2014 essentially none will be left; 14 million will migrate to the Exchanges and 4 million will find their way into employer-sponsored insurance. No one will have “kept their plan.”

RAND: 2010 Establishing State Health Insurance Exchanges study (red box added by me)

The CBO and Other Government Assertions

But it was not just RAND that was assuming that many persons with individual health insurance policies would be impelled to enter the Exchanges, in which policies with Essential Health Benefits and other expensive protections would prevail, it was also Congressional Budget Office, another source relied upon critically in forecasting the effects of what was becoming the Affordable Care Act. Consider the CBO’s letter of November 30, 2009, to Senator Evan Bayh. It estimates that 5 million people (14 million now outside Exchanges; 9 million left by 2016) will be move from nongroup coverage to coverage inside the Exchanges. While some of these may move voluntarily, there is no assertion that all will cheerfully accept the “better” coverage offered inside the Exchanges. The key quote comes in an explanation of why the ACA will actually lower premiums.

CBO and JCT estimate that about 32 million people would obtain coverage in the nongroup market in 2016 under the proposal, consisting of about 23 million who would obtain coverage through the insurance exchanges and about 9 million who would obtain coverage outside the exchanges. Relative to the situation under current law, with about 14 million people buying nongroup coverage, the different mix of enrollees would yield average premiums per person in that market that are about 7 percent to 10 percent lower.

That estimate of 5 million people is reiterated in a March 2010 letter from the CBO to Senator Harry Reid in which the CBO attempts to compute the costs of the ACA. The table below (a screen capture edited to delete unimportant parts) shows the computation.

Table showing CBO prediction on nongroup policies

Finally, there is what some have called the “smoking gun” contained in the pages of the June 17, 2010 Federal Register, a document (shown below with yellow highlighting) that captures the official views of the Department of Health and Human Services. Although the document does not state the movement out of non-group policies and into the Exchanges would be entirely voluntary, it is difficult to believe that with 40 to 67% moving, all would be doing so cheerfully and because they just “did not like” their existing healthcare plan.

June 17, 2010 Federal Register

Whether President Obama knew of this issue or at what level of detail is unclear. The Republican party is currently running an emotionally charged “stray cats and dogs video” containing some remarks of the President in 2010 from which those undisposed towards him might infer that he was aware of the issue. There are, however, a number of ways of interpreting the President’s elliptical and metaphorical remarks and it may remain to future historians to discern whether the President was simply unaware of the detail that some Americans might be forced from health plans that they truly liked to dispreferred coverage in the Exchanges or whether he, perhaps like some around him, simply regarded that inevitability as a cost of reforming a major American institution in which it was completely bizarre to think that no one at all would be hurt.

The MIT/Gruber Analysis

A leading academic proponent of the Affordable Care Act and consultant to the Obama administration during its development has been MIT economics professor Jonathan Gruber. (He’s also, by the way, the author by the way of a fantastic (if sometimes fairy tale-esque) graphic novel on Health Care Reform). Professor Gruber’s work has been instrumental in persuading people that an appropriately structured health insurance market can function even in the absence of medical underwriting. In 2011 and under the auspices of the National Bureau of Economic Research, Professor Gruber attempted to assess how reasonable were the projections made regarding the Affordable Care Act and the CBO’s earlier contention that it would actually lower the federal deficit. Here is what he thought would happen with the individual market. He thought those who moved from the existing nongroup market to the exchanges would find their premiums increasing 27-30% as a result. (page 16). He deprecated the potentially significant negative implications many might draw from such a finding by contending, however, that the purchasers would be rewarded with somewhat better policies: “[g]iven that the minimum standards are fairly modest, however, it seems likely that most of the increase in plan quality reflects voluntary upgrades.” (page 16). Thus, Professor Gruber did not contend that all would be better off as a result of the prohibition on non-grandfathered policies sold without Essential Health Benefits; he simply contended (possibly with some accuracy) that most would.

They knew and they understandably did nothing

So, if the people in the know knew, why did they do nothing about it.? Why did they not insist that the people be able to keep their health plans even if they evolved and not be impelled to purchase possibly better but possibly more expensive policies inside the Exchanges? And the answer is that they did nothing about it because they needed those people to sacrifice in order to make the whole scheme work. And so long as those people were the faceless masses — the anonymous red shirts of a Star Trek landing mission — it all made sense. They needed those people inside the Exchanges because many of them would have been recently medically underwritten and have low medical costs. They needed them because pushing people with low medical costs inside the Exchange was what was needed — and is still needed today — to make a health insurance marketplace without medical underwriting work. They needed them to prevent the adverse selection death spiral. They were, in short, expendables, and, besides, were getting something better than they had even if they did not value it properly.

And what was perhaps sadly true back in 2010 is sadly true today. The Exchanges are already unbelievably fragile and becoming more unstable each day that healthcare.gov stays more the butt of jokes than of a system for purchasing insurance. They are even more likely to break if people — the ones with low expected medical expenses — are permitted to separate themselves out and permitted to purchase cheaper and possibly less lavish policies outside the Exchanges. In economics, one might think of the availability of off-the-Exchange lower-benefit policies as permitting a “separating equilibrium” in which the healthier group stay in the tin policies found outside the Exchanges and the more expensive group head for the bronze, silver, gold and platinum to be found inside the Exchanges. And while one might think that everyone would be happy with this broader set of choices, the problem is that the removal of a large chunk of healthy people from the Exchanges means that there will be tremendous pressure on prices inside the Exchange to go up. The discrimination against the unhealthy, opposition to which formed an intellectual premise of the Affordable Care Act, will reappear.

So, do not expect insurers to take the Keep Your Plan Act lying down. Insurers priced their policies inside the Exchanges on the assumption — that sophisticated people knew about — that the Exchanges would be receiving an influx of generally healthy people that had recently been underwritten for insurance outside the Exchanges. Insurers knew — because they had the power to make it so — that those people would be receiving cancellation notices from their insurers and would thus have a choice either to go bare or to purchase policies inside the Exchanges. Insurers banked that many of them would invigorate the pools inside the Exchanges by choosing to purchase policies there. Take all that away, and many insurers will begin to regret — even more than I suspect many of them do as the debacle of healthcare.gov and the enrollment figures become ever more clear — that they ever supported the Affordable Care Act or thought there was gold in the hills of the Exchanges.

Insurers are not without recourse. There is little I know of that prevents the insurers from walking out of the Exchanges. Some have cancellation clauses built in to their contracts and it would create interesting contract litigation if some insurers decided, notwithstanding the existence of such cancellation clauses, simply to refund the advance premiums of prospective policyholders and say that they were not going to play. Note for contracts professors only: voluntary restitution in lieu of performance where performance is prevented by government order under Restatement (Second) of Contracts section 264?

But even if the spectre of mass cancellations for 2014 is unrealistic, insurers have to start planning real soon if they want to continue in the Exchanges in 2015. One expert at a conference in which I served as moderator contended that insurers will likely need to make a decision in April 2014 because that is when they will need to start submitting proposed new rates to insurance regulators. And every single day brings a new alarm bell suggesting they should not. The individual mandate might be delayed or cancelled. And although the individual mandate for 2014 is rather weak, still, such a delay will dilute further any otherwise existing incentives for the healthy to enroll in the Exchange. Healthcare.gov continues not to work well — it is revealed today that even the poor “Glitch Girl” apparently hasn’t tried to sign up. And now a broad spectrum of legislators and at least one former Democratic President — either embarrassed by what now appears to have been an untruth and/or cowed by the faces of earnest Americans being attached to what was heretofore treated as “statistics” — want to remove a source of potentially healthy insureds from the Exchange pools.

To be sure, there remain some protections for insurers who stay in. The little-discussed but, as it may turn out, unbelievably important “reinsurance and risk adjustment” provisions of the Affordable Care Act (42 U.S.C. 18061-063) may limit the losses insurers will suffer even if horrible adverse selection results from the confluence of events and hasty reforms. And, of course, if the enrollment numbers remain as infinitesimal as they now appear to be, not much matters. Even if premiums are off by a factor of 2, insurers in an absolute sense can’t lose all that much money if only 100,000 people ever enroll.

The Fix is not really a Fix

There are two other matters to discuss with respect to H.R. 3350. The first is use of the word “may” and the second is a technical problem.

“May” not “Must”

The key thing to recognize is that H.R. 3350 does not force insurers to restore insurance that they recently cancelled. Nowhere does H.R. 3350 say “must” or “shall.” Instead, it just says that insurers “may continue” to sell the policies they had in effect on January 1, 2013. It says only that, if they do so, they will not be treated as selling some sort of unlawful insurance prohibited by the Affordable Care Act. Thus, if insurers decide for whatever reason that they would rather not continue with those policies but would rather see those people inside the Exchanges, there is nothing in the Keep Your Health Plan Act that forces insurers to try and reverse their recent actions. As a result, some insureds will not be able to keep their health plans although failures in such respect will be more clearly the result of insurer choice than of federal compulsion. This, of course, may come as small consolation to those who truly liked their still cancelled old health insurance plans.

A Technical Problem