The Obama administration announced earlier today that it would increase the rate of subsidy provided insurers under the transitional reinsurance program established by the Affordable Care Act. This program, in effect for the policies sold in 2014, 2015, and 2016 on one of the individual insurance exchanges fostered by the ACA, provides free specific stop loss reinsurance to insurers, something insurers would otherwise have to pay a lot of money to obtain. The Center for Medicare and Medicaid Services (CMS) announced today that instead of taxpayers giving insurers 80% of the losses on any individual for their claims between $45,000 and $250,000, it would now pay a full 100% of these losses.

The higher rate of reinsurance should not be interpreted as a sign that claims were lower than insurers expected — something that would run contrary to many of the recent insurer rate hike filings or the losses reported by many insurers. It is not a sign of the success of Obamacare; rather it is an artifact of its problems. If, for example, there were 14% fewer people enrolled in Obamacare than at the time the reinsurance rates were initially determined (7 million vs. 6 million), reinsurance payments could be, as here, yet more generous to insurers even if claims were 10% higher than originally projected.

There are several implications of today’s announcement. First, it means that, on a percentage basis, the ACA is subsidizing exchange insurers for 2014 even more than regulations enacted under it had heretofore prescribed. Since this same money paid to insurers could instead have been used to provide greater subsidies to poorer and middle class individuals trying to purchase health insurance, the candy distributed today to insurers is a bit troubling. Second, because CMS says it will actually have money left over from 2014 even after the increase in reinsurance rates, and because enrollment in Obamacare remains considerably lower than was estimated at the time of its enactment, there is an increased likelihood of reinsurance payments to insurers being higher than originally authorized in 2015.

We can get some sense of the magnitude of the changes announced today. To do so, I use data embedded in the Actuarial Value Calculator, a document produced by CMS for the purposes of figuring out whether various insurance plans met the standards for bronze, silver, gold and platinum policies. For an average silver policy, for example, the reinsurance that would have been provided prior to today would have been expected to save insurers about 11% in expenses, and, quite likely, premiums. With the new reinsurance parameters, the transitional reinsurance program will save insurers selling the same silver policies about 14%.

We can do the same exercise for platinum, gold and bronze policies. The results are not much different. The table below shows the results.

Metal Level

Original subsidy

New subsidy

Bronze

11%

13%

Silver

11%

14%

Gold

11%

13%

Platinum

10%

12%

Two foootnotes

1. This is actually the second time CMS has made the transitional reinsurance program for 2014 more generous. Originally, the reinsurance would “attach” at $60,000. If an individual’s claims were below that amount, no reinsurance would kick in. Leter, CMS changed the attachment point to $45,000.

2. How could I do this computation so swiftly? I’ve been preparing for testimony before the House Ways and Means Committee on, among other things, the effect of the transitional reinsurance program on insurer rate changes and I’ve been working on a talk on a similar topic for the R in Insurance Conference later this month. So, all I had to do was plug the new parameters into my model, and out came the results. Be prepared.

That’s in addition to whatever increases are caused by medical inflation and adverse selection

As we draw to what was originally to be the close of the 2014 regular open enrollment period for policies sold on Exchanges under the Affordable Care Act and as the evidence comes in on the actual numbers and demographics of purchasers, it’s time to start thinking about 2015. In this post, I’m not going to speculate today about the effects of the expanding the “hardship exemption” from the individual mandate on insurers’ experience in 2014, the effect of the “Honor System” in extending the time in which individuals can purchase coverage on the Exchange without medical underwriting, or on the effects of any of the other the myriad changes in the law that have been promulgated by the Executive Branch since Congress passed the ACA in 2010. Instead, I want to focus on the effect of statutory changes in the government-created reinsurance program on likely premiums in 2015.

First, a refresher. One of the ideas behind Obamacare was to lure people into the Exchanges with carrots and sticks. The most frequently discussed carrots were advanced premium tax credits that reduced the effective price of insurance for many individuals and, for many of those receiving the premium tax credits, contracts with extra benefits (cost-sharing reductions) for which the purchasers do not have to pay. Not only, however, are Exchange policies subsidized by reducing the price to the consumer but also by reducing the cost the insurer faces in paying claims. A key mechanism for this latter reduction for the first three years of the program is free “reinsurance” provided to all insurers for slices of their claims. Of course, the reinsurance isn’t really free; there’s a $63 per insured life tax levied on other health insurance policies in order to make policies on the Exchange more attractive, a transfer whose justice will not be considered today.

The reinsurance works in 2014 by having the government reimburse insurers for 80% of the amount of any insureds claim between $45,000 and $250,000. Thus, if an insured had claims of $105,000, the government rather than the insurer would pay for $48,000 of the claim while the insurer itself would pay for the remaining $57,000. If an insured had claims of $30,000, the insurer would pay the whole bill. And if an insured had claims of, say, $300,000, the government would cover more than half — $164,000 — while the insurer itself would pay the remaining $136,000.

Sample of the data embedded in the Excel spreadsheet for The Actuarial Value Calculator

One can use information contained in the government’s own “Actuarial Value Calculator” to estimate the effect of this reinsurance on Exchange premiums. (I’ve placed a graphic above this paragraph showing some of the information in the Calculator.) Based on my computations using Mathematica and done in connection with a recent academic conference, the reinsurance should lower the price of an Bronze policy by about $450 (11%), a Silver policy by $531 (11%), a Gold policy by $545 (11%) and a Platinum policy by $616 (10%).

The parameters of the reinsurance policy will change in 2015. HHS currently says that instead of “attaching” at $45,000, reinsurance will only kick in if an individual’s claims exceed $70,000. And instead of reimbursing the insurer 80% of the slice between the attachment point and the $250,000 limit, the government will now reimburse just 50% of the slice. The table below shows the results of this change in reinsurance on the expected value of the reinsurance policy. If one assumes that medical inflation will be 4%, the value of the reinsurance will range from $192 for Bronze policies to $243 for Platinum policies. These computations are all again done using Mathematica based on data provided by the government itself in its Actuarial Value Calculator.

Value of reinsurance subsidy in 2015 for varying rates of medical inflation

Insurers will need to compensate for the diminished reinsurance by raising prices. How much? The table below shows the answer: somewhere between 7 and 8% depending on the type of policy being sold and the rate of medical inflation.

Increase in premiums for 2015 just to cover reduction in reinsurance subsidies

If one adds regular medical inflation to the increases induced by reduced subsidization, here’s a picture of what we get. To obtain a single result for each rate of medical inflation, I’m going to weight the metal tiers according to their rough proportions in the market as last measured.

Projected premium increases for 2015 with reinsurance subsidy reductions taken into account for varying rates of medical inflation

The results of combining ordinary medical inflation with reinsurance reductions are a bit scary. While most people seem to believe the ACA system can survive premium increases of 6% or 8%, what we see is that even if medical inflation is kept to 4%, the results of combining medical inflation with subsidy reduction is a 12% hike. And, if insurers are nervous about pricing in 2015 due to higher than expected claims experience in the early parts of 2014 or the persistence of problematic demographics such that they expect ordinary claims inflation of 10%, then we start getting into premium increases of about 18%.

Is there a workaround?

It is fair to say that the Obama administration has not been reluctant to change implementation of the Affordable Care Act in response to changing circumstances. And, I suspect that if the Obama administration starts getting hints that insurers selling on the Exchanges are either thinking of pulling out of the Exchanges or of raising premiums significantly, one of the ways it will respond is by altering the parameters of the reinsurance program. The attachment point, limit and reimbursement rate are all matters as to which the Obama administration has regulatory flexibility. Indeed, it changed the 2014 reinsurance parameters favorably for insurers late into the process. And, of course, by providing a lower attachment point, higher reimbursement rate and/or a higher limit, the government can increase the effective subsidy created by the free reinsurance and thereby reduce pressure on insurers to raise premiums.

If, for example, the Obama administration were to go to, say, a 65% reimbursement rate rather than a 50% rate for 2015 and were to go to a $60,000 attachment point rather than a $70,000 one, a 4% increase in medical inflation might result in a lesser 9% increase in premiums rather than 12%. And even a 10% increase would result in a lesser 14% increase in premiums rather than an 18% one.

The problem with this “fix,” however is that it costs money. And, by statute, the government is supposed to spend $4 billion less on the reinsurance program on claims for 2015 than it spent on claims for 2014. That’s why HHS reduced the reinsurance parameters for 2015 in the first place.

I can foresee two ways around this limitation. The first is for the Obama administration to engage in creative math and find a theory under which the projected cost of its reinsurance program aligns with statutory requirements. While cynics may be fond of my projection of this response, there is a serious question as to the extent that principled actuaries in the Executive branch will permit this “methodology” to be used. The second possibility is for the Obama administration to stockpile funds from 2014 and use them to pay reinsurance in 2015. Section 1341(b)(4)(A) of the ACA appears to make this possible. This scheme only works, however, if the government actually has money left over from its 2014 reinsurance pool. And, while lower than expected enrollments in the Exchanges increase the probability that there will be money remaining, that potential surplus could well be eaten away if claims for 2014 are higher than expected.

A result of improper conceptualization

Amidst all the technical detail, it’s worth thinking about how this could have happened. How could the architects of the ACA, who were acutely aware of the risks of an adverse selection death spiral, create a system in which there were built in pressures to increase premiums? I think the answer comes in examining the rhetoric of the reinsurance program. It was not articulated as a subsidy but rather as a way of reducing the risk of entering the Exchanges. See here, here and here for examples. If adverse selection or moral hazard drove claims costs up, the government would significantly insulate insurers from that risk by providing reinsurance. This, along with Risk Corridors in the first three years of the program, and Risk Adjustment thereafter, was supposed to provide insurers with comfort as they deliberated whether to enter an untested market for health insurance in which most of their conventional underwriting mechanisms were prohibited. And, indeed, the Transitional Reinsurance program does reduce risk. Based on my computations, it reduces the standard deviation of losses for Bronze policies from $16,403 to $11,430 and for Platinum policies from $17,215 to $11,598.

If one conceptualizes the transitional reinsurance program merely as a risk reduction policy, it makes sense to phase it out as insurer experience with the purchasing pools in the ACA. Insurers gain confidence in how to price their policies. But what appears to have been forgotten in that calculation is that these reinsurance subsidies also save insurers lots of money. And insurers will need to respond to the phasing out of these substantial subsidies by raising premiums. Whether that tunnel vision in conceptualization contributes to an implosion of the ACA, at least in some states, remains to be seen.

Concerns about whether insurance sold on the individual Exchanges under the Affordable Care Act will succumb to an adverse selection death spiral have focused mainly on the shortage of younger enrollees into the system. This shortage is potentially a problem because, due to section 1201 of the ACA, premiums for younger enrollees must be at least one third of that for older enrollees even though actuarial science tells us that younger enrollee expenses are perhaps just one fifth of those for older enrollees. Younger enrollees are needed in large numbers to subsidize the premiums of the older enrollees. But at least premiums under the ACA respond at least somewhat to age.

The lesser studied potential source of adverse selection problems, however, is the fact that medical expenses of women for many ages are essentially double those of men and yet the ACA forbids rating based on gender. In a rational world, one would therefore expect women of most of the ages eligible for coverage in the individual Exchanges to enroll in plans on the Exchange at a higher rate than men. But, since the women have higher than average expenses than men, premiums based on the average expenses of men and women will prove too low, creating pressure on insurers to raise prices. And, of course, there could also be some disproportionate enrollment by older men who have higher medical expenses than women of equal age. While I welcome contrary arguments in what I regard as a fairly new area of study involving the ACA, gender-based adverse selection would certainly appear to be a real problem created by the structure of that law. To me, it looks to be potentially as large a problem as age-based adverse selection. It is certainly one that needs continuing and careful evaluation.

Caveats

I see only three limited factors that reduce what would otherwise appear to be a significant additional source for significant adverse selection. As set forth below, however, I do not believe that any of these factors are likely to materially reduce the problem.

1. Ignorance

The first is ignorance. Adverse selection emerges only if individuals can accurately foretell their future medical expenses with some accuracy. To the extent, therefore, that men and women are ignorant of the effect of gender on their projected medical expenses, adverse selection is potentially diminished. I say “potentially,” however, because of a subtlety: people don’t have to know why their expenses are what they are in order for adverse selection to emerge; they only have to be somewhat accurate in their guess. Thus, even if men and women don’t make the cognitive leap from seeing lower (or higher) medical expenses to issues of gender, but they still on balance get it right, adverse selection can exist. Thus, I end up doubting that ignorance of the correlation between gender and medical expense is going to retard adverse selection problems very much.

2. Correlation between gender and expense is lower for those 50-65.

The second factor that might reduce adverse selection based on gender is, curiously enough, adverse selection based on age. The difference between male and female medical expenses diminishes as one exits the middle 40s and heads into the 60s. Indeed, somewhere in the late 50s, the rates cross and men have slightly higher average medical expenses than women. Therefore, to the extent that it is the 50-65 set that is disproportionately purchasing coverage in the individual Exchanges, the potential for gender-based adverse selection is diminished — but only somewhat . I say “but only somewhat” because if males over the age of about 55 or 58 enroll at higher rates than women of similar ages there will actually be adverse selection pressures due to the higher medical expenses of men that age. On the other hand, to the extents efforts are made to reduce age-based adverse selection by promoting coverage to the younger (potentially child-bearing) set, the potential for most forms of gender-based adverse selection increases.

3. Gender-correlated risk aversion

The third factor that could in theory reduce adverse selection problems is if men are more risk averse than women with respect to medical expenses and therefore purchase health insurance at equivalent rates even though their risk is objectively lower. Men could conceivably be somewhat more risk averse due to prevailing gender roles in the economy: on average it is possible that health problems among men may affect the family’s income more than health problems among women. Although as an academic I feel I would be remiss in failing to at least mention this possibility, in the end I doubt it amounts to very much. The roles of men and women in the family economy are complex and variegated. And the sources of risk aversion with respect to health are likewise multifold, having a lot to due with individual psychology, family history and family structure. And, of course, it could be that middle aged men are less risk averse than women, in which case the effects of adverse selection are worse.

The data

How do we know about the effects of gender? The graphics below show two studies on the topic. The first is from the Society of Actuaries and was relied on by the Kaiser Family Foundation in its recent study of the effect of age rating. Look at the solid blue (male) and pink (female) lines. (Cute, Kaiser). One can see that until age 18, the costs for men and women in the commercial market has been about the same. By the time we get to, say, age 32, the cost for women is about 2.5 times that for men. The gap then shrinks so that by the time we get to age 58 or so, men’s costs actually start to somewhat exceed women’s.

Society of Actuaries report on gender and healthcare expenses

A study by the respected Milliman actuarial firm, although differing in detail, shows roughly the same pattern. At age 30 or so, female expenses (blue) and about double those of males (green). The gap shrinks until about age 55, at which point male expenses exceed female expenses. (I’m not sure why Milliman shows female expenses being so much higher than male expenses for the age bracket marked “to 25” unless by “to 25” they mean ages 18-25.)

Is Gender-Based Adverse Selection Actually Happening?

As to whether the theoretical possibility of gender-based adverse selection is actually materializing, there is yet strikingly little evidence. I have scoured the Internet and found almost nothing on the gender of enrollees. In some sense this is not surprising since, unlike age, on which we have a trickle of data from CMS, which somehow is just unable to compile and release more complete information, gender is completely irrelevant to premium rates. On the other hand, as shown below, the federal application asks about gender, as do a few other state applications such as California, Kentucky and Washington State. So, in theory we should be able to get the information at some point. In the meantime, if anyone has information on this issue, I would love to see it. What we really need is a breakdown of enrollees based on both age and gender because the ratio’s role varies depending on whether enrollees below age 55 or so are involved or whether enrollees above age 55 are involved.

Two other notes

1. Someone might, I suppose, think that since the role of gender reverses at about age 55, the effects of gender on adverse selection cancel each other out. This would be totally wrong. If women have higher medical expenses than men up to about age 55 and if women therefore enroll at higher rates, that can cause adverse selection and premium pressures for enrollees of those ages. And if men have have higher medical expenses than women after about age 55 and if men therefore enroll at higher rates, that can cause adverse selection and premium pressures for enrollees of those ages. The effects are cumulative and not offsetting.

2. Does this mean I am opposed to unisex rating? No, not necessarily. First, women face higher medical expenses than men from about 20 to 50 significantly because of childbearing expenses. A family law expert on my faculty confirms what I suspected, which is that there is certainly no routine cause of action by the pregnant female against the prospective father for prenatal maternity expenses. We currently ascribe these expenses to the woman even though a male generally has contributed to those expenses through consensual sex. One could argue that unisex rating offsets this proxy for responsibility.

Second, if there are adverse selection problems caused by unisex rating, they can, in theory, be addressed by programs that that subsidize insurers for female enrollees. Impolitic as it might be to say so, one could treat being a fertile woman as a “risk factor” in the same way that section 1343 of the ACA currently treats medical conditions such as heart disease. The cost of the subsidies resulting therefrom could be seen as compensating somewhat for the transaction costs of figuring out which childbearing expenses the male partner has contributed to as well as tracking down the male partner and trying to hold him financially responsible.

What I am concerned about, however, is ignoring the issues created by unisex rating. Since it is not currently corrected for by section 1343 of the ACA and corrected for only in a very indirect and partial way by sections 1341 and 1342 of the ACA, there is the potential for the absence of gender rating to destabilize and ultimately shrink the insurance markets in ways that do few people any good. Wishing that a problem would go away or hoping that people don’t see the opportunities to optimize their behavior is seldom a recipe for successful government programs.

That might be how the National Enquirer would title this blog entry. And, hey, if mimicking its headline usage attracts more readers than “Reconstructing mixture distributions with a log normal component from compressed health insurance claims data,” why not just take a hint from a highly read journal? But seriously, it’s time to continue delving into some of the math and science behind the issues with the Affordable Care Act. And, to do this, I’d like to take a glance at a valuable data source on modern American health care, the data embedded in the Actuarial Value Calculator created by our friends at the Center for Consumer Information and Insurance Oversight (CCIIO).

This will be the first in a series of posts taking another look at the Actuarial Value Calculator (AVC) and its implications on the future of the Affordable Care Act. (I looked at it briefly before in exploring the effects of reductions in the transitional reinsurance that will take effect in 2015). I promise there are yet more important implications hidden in the data. What I hope to show in my next post, for example, is how the data in the Actuarial Value Calculator exposes the fragility of the ACA to small variations in the composition of the risk pool. If, for example, the pool of insureds purchasing Silver Plans has claims distributions similar to those that were anticipated to purchase Platinum Plans, the insurer might lose more than 30% before Risk Corridors were taken into account and something like 10% even after Risk Corridors were taken into account. And, yes, this takes account of transitional reinsurance. That’s potentially a major risk for the stability of the insurance markets.

What is the Actuarial Value Calculator?

The AVC is intended as a fairly elaborate Microsoft Excel spreadsheet that takes embedded data and macros (essentially programs) written in Visual Basic, and is intended to help insurers determine whether their proposed Exchange plans conform to the requirements for the various “metal tiers” created by the ACA. These metal tiers in turn attempt to quantify the ratio of the expected value of the benefits paid by the insurer to the expected value of claims covered by the policy and incurred by insureds. The programs, I will confess, are a bit inscrutable — and it would be quite an ambitious (and, I must confess, tempting) project to decrypt their underlying logic — but the data they contain is a more accessible goldmine. The AVC contains, for example, the approximate distribution of claims the government expects insurers writing plans in the various metal tiers to encounter.

There are serious limitations in the AVC, to be sure. The data exposed has been aggregated and compressed; rather than providing the amount of actual claims, the AVC has binned claims and then simply presented the average claim within each bin. This space-saving compression is somewhat unfortunate, however, because real claims distributions are essentially continuous. Everyone with annual claims between $600 and $700 does not really have claims of $649. This distortion of the real claims distribution makes it more challenging to find analytic distributions (such as variations of log normal distributions or Weibull distributions) that can depend on the generosity of the plan and that can be extrapolated to consider implications of serious adverse selection. It’s going to take some high-powered math to unscramble the egg and create continuous distributions out of data that has had its “x-values” jiggled. Moreover, there is no breakdown of claim distributions by age, gender, region or other factors that might be useful in trying to predict experience in the Exchanges. (Can you say “FOIA Request”?)

This blog entry is going to make a first attempt, however, to see if there aren’t some good analytic approximations to the data that must have underlain the AVC. It undertakes this exercise in reverse engineering because once we have this data, we can make some reasonable extrapolations and examine the resilience — or fragility — of the system created by the Affordable Care Act. The math may be a little frightening to some, but either try to work with me and get it or just skip to the end where I try to include a plain English summary.

The Math Stuff

1. Reverse engineering approximate continuous approximations to the data underlying the Actuarial Value Calculator

Nothwithstanding the irritating compression of data used to produce the AVC, I can reconstruct a mixture distribution composed mostly of truncated exponential distributions that well approximates the data presented in the AVC. I create one such mixture distribution for each metal tier. I use distributions from this family because they have been proven to be “maximum entropy distributions“, i.e. they contain the fewest assumptions about the actual shape of the data. The idea is to say that when the AVC says that there were 10,273 claims for silver-like policies between $800 and $900 and that they averaged $849.09, that average could well have been the result of an exponential distribution that has been truncated to lie between $800 and $900. With some heavy duty math, shown in the Mathematica notebook available here, we are able, however, to find the member of the truncated exponential family that would produce such an average. We can do this for each bin defined by the data, resorting to uniform distributions for lower values of claims.

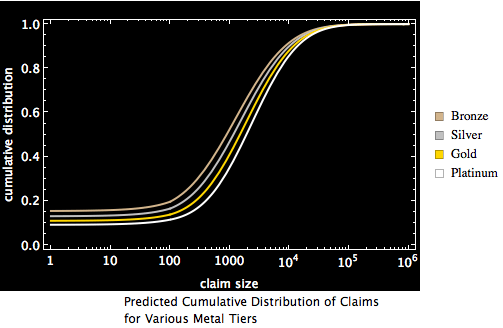

The result of this process is a messy mixture distribution, one for each metal tier. The number of components in the distribution is essentially the same as the number of bins in the AVC data. This will be our first approximation of “the true distribution” from which the claims data presented in the AVC calculator derives. The graphic below shows the cumulative density functions (CDF) for this first approximation. (A cumulative density function shows, for each value on the x-axis the probability that the value of a random draw from that distribution will be less than the value on the x-axis). I present the data in semi-log form: claim size is scaled logarithmically for better visibility on the x-axis and percentage of claims less than or equal to the value on the x-axis is shown on the y-axis.

CDF of the four tiers derived from the first approximation of the data in the AVC

There are two features of the claims distributions that are shown by these graphics. The first is that the distributions are not radically different. The model suggests that the government did not expect massive adverse selection as a result of people who anticipated higher medical expenses to disproportionately select gold and platinum plans while people who anticipated lower medical expenses to disproportionately select bronze and silver plans. The second is that, when viewed on a semi-logarithmic scale, the distributions for values greater than 100 look somewhat symmetric about a vertical axis. They look as if they derive from some mixture distribution composed of a part that produces a value close to zero and something kind of log normalish. If this were the case, it would be a comforting result, both because such mixture distributions would be easy to parameterize and extrapolate to lesser and greater forms of adverse selection and because such mixture distributions with a log normal component are often discussed in the literature on health insurance.

2. Constructing a single Mixture Distribution (or Spliced Distribution) using random draws from the first approximation

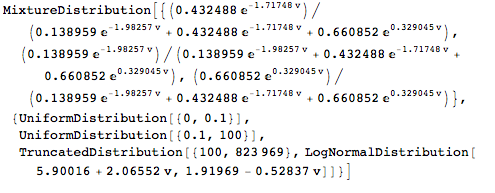

One way of finding parameterizable analytic approximations of “the true distribution” is to use our first approximation to produce thousands of random draws and then to use mathematical (and Mathematica) algorithms to find the member of various analytic distribution families that best approximate the random draws. When we do this, we find that the claims data underlying each of the metal tiers is indeed decently approximated by a three-component mixture distribution in which one component essentially produces zeros and the second component is a uniform distribution on the interval 0.1 to 100 and the third component is a truncated log normal distribution starting at 100. (This mixture distribution is also a “spliced distribution” because the domains of each component do not overlap). This three component distribution is much simpler than our first approximation, which contains many more components.

We can see how good the second-stage distributions are by comparing their cumulative distributions (red) to histograms created from random data drawn from the actuarial value calculator (blue). The graphic below show the fits to look excellent.

Note: I do not contend that a mixture distribution with a log normal distribution perfectly conforms to the data. It is, however, pretty good for practical computation.

Actual v. Analytic distributions for various metal tiers

3. Parameterizing health claim distributions based on the actuarial value

The final step here is to create a function that describes the distribution of health claims as a function of a number (v) greater than zero. The concept is that, when v assumes a value equal to the actuarial value of one of the metal tiers, the distribution that results mimics the distribution of AVC-anticipated claims for that tier. By constructing such a function, instead of having just four distributions, I obtain an infinite number of possible distributions. These distributions collapse as special cases to the actual distribution of health care claims produced by the AVC. This process enables us to describe a health claim distribution and to extrapolate what can happen if the claims experience is either better (smaller) than that anticipated for bronze plans or worse (higher) than that anticipated for platinum plans. One can also use this process to compute statistics of the distribution as a function of v such as mean and standard deviation.

Here’s what I get.

Mixture distribution as a function of the actuarial value parameter v

Here is a animation showing, as a function of the actuarial value parameter v, the cumulative distribution function of this analytic approximation to the AVC distribution.

Cumulative distribution of claims by “actuarial value”

One can see the cumulative distribution function sweeping down and to the right as the actuarial value of the plan increases. This is as one would expect: people with higher claims distributions tend to separate themselves into more lavish plans.

Note: I permit the actuarial value of the plan to exceed 1. I do so recognizing full well that no plan would ever have such an actuarial value but allow myself to ignore this false constraint. It is false because what one is really doing is showing a family of mixture distributions in which the parameter v can mathematically assume any positive value but calibrated such that (a) at values of 0.6, 0.7, 0.8 and 0.9 they correspond respectively with the anticipated distribution of health care claims found in the AVC for bronze, silver, gold and platinum plans respectively and (b) they interpolate and extrapolate smoothly and, I think, sensibly from those values.

The animation below presents largely the same information but uses the probability density function (PDF) rather than the sigmoid cumulative distribution function. (If you don’t know the difference, you can read about it here.) I do so via a log-log plot rather than a semi-log plot to enhance visualization. Again, you can see that the right hand segment of the plot is rather symmetric when plotted using a logarithmic x-axis, which suggests that a log normal distribution is not a bad analytic candidate to emulate the true distribution.

Some initial results

One useful computation we can do immediately with our parameterized mixture distribution is to see how the mean claim varies with this actuarial parameter v. The graphic below shows the result. The blue line shows the mean claim as a function of “actuarial value” without consideration of any reinsurance under section 1341 (18 U.S.C. § 18061) of the ACA. The red line shows the mean claim net of reinsurance (assuming 2014 rates of reinsurance) as a function of “actuarial value.” And the gold line shows the shows the mean claim net of reinsurance (assuming 2015 rates of reinsurance) as a function of “actuarial value.” One can see that the mean is sensitive to the actuarial value of the plan. Small errors in assumptions about the pool can lead to significantly higher mean claims, even with reinsurance figured in.

Mean claims as a function of actuarial value parameter for various assumptions about reinsurance

I can also show how the claims experience of the insurer can vary as a result of differences between the anticipated actuarial value parameter v1 that might characterize the distribution of claims in the pool and the actual actuarial value parameter v2 that ends up best characterizing the distribution of claims in the pool. This is done in the three dimensional graphic below. The x-axis shows the actuarial value anticipated to best characterize an insured pool. The y-axis shows the actuarial value that ends up best characterizing that pool. The z-axis shows the ratio of mean actual claims to mean anticipated claims. A value higher than 1 means that the insurer is going to lose money. Values higher than 2 mean that the insurer is going to lose a lot of money. Contours on the graphic show combinations of anticipated and actual actuarial value parameters that yield ratios of 0.93, 1.0, 1.08, 1.5 and 2. This graphic does not take into account Risk Corridors under section 1342 of the ACA.

What one can see immediately is that there are a lot of combinations that cause the insurer to lose a lot of money. There are also combinations that permit the insurer to profit greatly.

Ratio of mean actual claims to mean expected claims for different combinations of anticipated and actual actuarial value parameters

Plain English Summary

One can use data provided by the government inside its Actuarial Value Calculator to derive accurate analytic statistical distributions for claims expected to occur under the Affordable Care Act. Not only can one derive such distributions for the pools anticipated to purchase policies in the various metal tiers (bronze, silver, gold, and platinum) but one can interpolate and extrapolate from that data to develop distributions for many plausible pools. This ability to parameterize plausible claims distributions becomes useful in conducting a variety of experiments about the future of the Exchanges under the ACA and exploring their sensitivity to adverse selection problems.

Resources

You can read about the methodology used to create the calculator here.

You can get the actual spreadsheet here. You’ll need to “enable macros” in order to get the buttons to work.

The actuarial value calculator has a younger cousin, the Minimum Value Calculator. If one looks at the data contained here, one can see the same pattern as one finds in the Actuarial Value Calculator.

Joke

Probably I should have made the title of this entry “Shocking sex secrets of the actuarial value calculator revealed!” and attracted yet more viewers. I then could have noted that the actuarial value calculator ignores sex (gender) in showing claims data. But that would have been going too far.

Many people who remain basically positive about the Affordable Care Act are viewing the enrollment statistics like the football fan whose team is 2-6 and who point out that the team could win 7 out of its 8 remaining games and still probably make the playoffs. Yes, getting off to a really bad start doesn’t preclude a happy ending. Success may still be mathematically possible. But unless there’s good reason to think that the fundamental factors such as poor coaching, poor game plans or unexpected injuries that have led to the bad start no longer apply, the more reasonable prediction is that things will continue more or less as they have.

For purposes of this blog entry, I’m going to assume that enrollment in the Exchanges ends up being about 2 million for 2014 instead of the projected 7 million. I can’t rigorously justify that number — but, of course, neither could the pundit who is now saying 4 million. And, if I had time and space I’d prefer to do this analysis under a variety of scenarios, but, for now, the 2 million figure feels about right. And if I were betting on which side of the 2 million we will fall, it would be the lower side. What are the consequences? I can’t address all of them in a single blog entry — and trying to predict matters past 2014 gets very treacherous — but here are some.

And, for those of you who don’t want to read further, here’s the headline:

Insurance sold through Exchanges without medical underwriting — a central promise of the Affordable Care Act — is likely to implode in a significant number of states by 2015 while limping along in several others but providing little net desired decrease in the number of people without quality health insurance. The silver lining in this failure will be that the program will likely cost less than projected due to fewer number of people receiving subsidies, although this reduction will be partly offset by higher-than-projected subsidies to the insurance industry. Expect significant pressure to grow among supporters of the Affordable Care Act to use these net savings to increase the subsidies available to people buying coverage through the Exchanges and to lure insurers in the problem states back into the Exchanges.

1. The number of people without private health insurance may actually grow

This is so because, if 2 million obtain insurance through the Exchanges but more people (3.5 million is a prevailing estimate from sources ranging from Forbes to Jonathan Gruber) lose their current individual health insurance, that’s a net decrease in the number of insured. And if we add in the loss of 100,000 or so people from the Pre-Existing Condition Insurance Plan that likewise is terminated or those who heretofore were in various state high risk pools, there is a serious risk that the Affordable Care Act will have decreased the number with private health insurance.

In fairness, I have not taken Medicaid expansion into account. Some may see it as unfair to count just the number of people with private health insurance rather than the number with access to health care through private insurance or public schemes such as Medicaid. And, indeed, in those states in which Medicaid has been expanded — one can’t blame President Obama too much if other states choose not to participate — enrollment has outpaced enrollment in private plans at about a 4-to-1 ratio. This suggests, by the way, that people are willing to use a web site, even some clunky ones, to sign up for health care if they think the price is right.

The rejoinder to the argument that we should consider Medicaid, however, is that an awful lot of political energy and an awful lot of monetary investment has been predicated on healthcare reform benefiting more than just the poor but the middle class too. If it turns out the middle class has, net, been hurt by the 2014 features of Affordable Care Act or has paid a large investment for the 2014 features of a law that, net, does provide little marginal benefit, it’s fair to criticize the 2014 features of the Act for their architectural shortcomings. And, yes, I know all about staying on your parents’ policy until you are 26 and limitations on rescissions, but none of those pre-2014 “achievements” should count in assessing the 2014 record.

2. The number of people with quality health insurance may stay about the same

Yes, there will be people who formerly had no health insurance or who had rotten health insurance who, thanks to the 2014 aspects of the ACA, now have health insurance that covers more. There are many news accounts from pro-ACA forces providing evidence of this. Here’s one (although all the “success stories” are likely to have high medical claims); here’s another (notice again that the successes are likely to have high medical claims).

But it may well be that for every such success story apparently to be catalogued by paid grants from the government, there is another who had health insurance tailored to their needs (such as policies for the 50 and over set that did not cover maternity expenses) who now find themselves priced out of the health insurance market with its Essential Health Benefits requirement (section 1302 of the ACA). Here’s a website inviting people to post their cancellation notices. Here are some anecdotes relating such problems (although one always have to be very careful about exaggerations in this arena; see here for a discussion of a particular case by Consumer Reports). Here’s another.

On balance, though, it’s quite believable that, many of the gains due to subsidization may be offset due to government offering only products that have more “features” than many people are willing to pay for. To analogize, consider a law that prohibited people from owning either a clunker car (defined somehow) or a car without four-wheel drive. The theory behind the law was that clunkers were unsafe and that four-wheel drive is sometimes useful: even if you don’t need it right now, you might need it or have needed it at some point. Fair enough. But such a law might not actually increase the number of people driving quality cars that fit their needs. Some people just can’t afford a new car. And others, who could afford a respectable car without four wheel drive and didn’t think they needed it right then (urban Floridians, for example), might simply decide not to get a car rather than use scarce marginal dollars for cars with features they don’t need. While such a result need not occur — it depends on all sorts of factors — my sense is that this is where we are heading with the Affordable Care Act and its fairly demanding and undifferentiated requirements for coverage in policies sold on the Exchanges.

3. Federal mandate tax payments may be a little bit bigger than expected for 2014

The Congressional Budget Office estimates this spring that the United States Treasury would receive about 2 billion dollars as a result of the individual mandate tax (26 U.S.C. § 5000A). That figure was premised, however, on a belief that 7 million people would enroll in the Exchanges. If only 2 million people get insurance through the Exchange that’s roughly 5 million fewer than anticipated who will not. There thus could be as many as 5 million more people who will have to pay the individual mandate (26 U.S.C. §5000A) and could lead to something like another $500 million in revenue next year.

Before we spend the money of 5 million more Americans who might have to pay extra in tax, however, we need to we need to subtract off two categories of people. (1) We should subtract off those who acquire faux-grandfathered policies created by President Obama’s recent turnabout to let people who like their (potentially cruddy) coverage keep it under some circumstances and not have to pay the individual mandate. (2) We should subtract off the small number of people who were projected to purchase policies on the Exchange but, because of poverty or otherwise, would not have had to pay the mandate tax had they failed to do so.

So, let’s say on balance that 3 million fewer people than projected pay the tax under 26 U.S.C. 5000A. It’s hard to know exactly what sort of tax revenue would be involved, but it is likely in excess of $285 million per year because each such person would have been responsible for at least a $95 per person penalty. (I know, I know, there are lots of complications because the penalty is difficult to enforce and because you only have to pay half for children, but then there are complications the other way in that $95 is a floor and one may have to pay 1% of household income). Why don’t we use round numbers, though, and say that the government might get about $300 million more in tax revenue for 2014 (although they may not get the money until 2015) due to lower-than-projected enrollments in the Exchanges.

4. Before the federal government subsidizes them, insurers in the Exchange will lose billions

4. Before consideration of various subsidies (a/k/a bailouts) of the insurance industry created by the Affordable Care Act, insurers could lose $2 billion as a result of having gambled that the Exchanges would be successful. Here’s how I get that figure. No one knows for sure but, if the experience under the PCIP plan is any guide, when about 1/3 of the projected number of people apply to a plan that is not medically underwritten, expenses per person can be more than double that originally expected. Even if we assume that experience under the PCIP is not fully applicable, given an enrollment 1/3 of that projected, it would shock me if covered claims were not at least 125% of that expected. If so, on balance that means that losses per insured could total roughly $1,000. If we multiply $1,000 per insured by 2 million insureds, we get about $2 billion. If the Exchanges lose money at the same rate as the PCIP, insurer losses could be upwards of $7 billion. Again, I make no pretense of precision here. I am simply trying to get a sense of the order of magnitude.

5. The federal government will subsidize insurers more than expected but insurers will still lose money

The Affordable Care Act creates several methods heralded as protecting insurers writing in the Exchanges from claims that were greater than they expected. One such method, Risk Corridors under section 1342 of the ACA, could end up helping insurers in the Exchanges significantly. But, if, as discussed here, enrollment in the Exchanges for 2014 is 2 million persons, the cost of helping the insurance industry in this fashion will be another $500 million for 2014. Risk Corridors, which have recently been aptly analogized to synthetic collateralized debt obligations (CDOs), requires the government to reimburse insurers for up to 80% of any losses they suffer on the Exchanges. It also imposes what amounts to a special tax (again of up to 80%) on profits that insurers may make on the Exchanges. The system was supposed to be budget neutral but, as I and others have observed, will in fact require the federal government to pay money in the event that insurer losses on the Exchange outweigh insurer gains. The basis for my $500 million computation is set forth extensively in a prior blog entry. It will only be more if, as discussed in another prior blog entry, the Obama administration modifies Risk Corridors to indemnify insurers for additional losses they suffer as a result of President Obama’s decision to let those with recently cancelled medically underwritten health insurance policies stay out of the Exchanges.

If claims are, as I have suggested 25% higher as a result of enrollment of 2 million, insurers will lose, after Risk Corridors are taken into account, about 9% on their policies. It would thus not surprise me to see insurers put in for at least a 9 or 10% increase on their policies for 2015 simply as a result of enrollment in the pools being smaller than expected.

The relatively modest 9% figure masks a far more significant problem, however. It is just a national average. Consider states such as Texas in which only 2,991 out of the 774,662 projected have enrolled thus far. If, say, Texas ends up enrolling “only” increasing its enrollment by a factor of 16 and gets to 50,000 enrollees, I would not be surprised to see claims be double of what was projected. Even with Risk Corridors, insurers could still lose about 24% on their policies. A compensating 24% gross premium increase, even if experienced only by that portion of the insurance market paying gross premiums, could well be enough to set off an adverse selection death spiral.

Footnote: For reasons I have addressed in an earlier blog entry, one of those methods, transitional reinsurance under section 1341 of the ACA is best thought of as a premium subsidy that induces insurers to write in the Exchanges. Because the government’s payment obligations are capped, however, the provision is unlikely to help them significantly if the cost per insured ends up being particularly high throughout the nation.

6. The federal government might save $19 billion in premium subsidies

The Congressional Budget Office assumed that premium subsidies would be $26 billion in 2014, representing a payment of about $3,700 per projected enrollee. If the distribution of policies purchased and the income levels of purchasers are as projected, but only 2 million people apply, that would reduce subsidy payments down to $7.5 billion. And if the policies sold in 2014 cost a little less than projected, that might further reduce subsidy payments. I think it would be fair, then, to estimate that low enrollment could save the federal government something like $19 billion in premium subsidies in 2014. This savings coupled with heightened tax revenue under 26 U.S.C. §5000A — could we round it to $20 billion — would be more than enough to cover insurer losses resulting from the pool being smaller and less healthy than projected.

The Bottom Line

I suspect my conclusion will make absolutist ideologues on the left and right equally uncomfortable. What I am wondering is if the Affordable Care Act might not die in 2015 with a giant imploding bang but rather limp on with a whimper. On balance, what we may well see if only 2 million enroll in Exchanges pursuant to the Affordable Care Act is a system that fails to function in some states and remains fragile and expensive elsewhere. On the one hand, it will be an expensive system because of the enormous overhead incurred in creating a highly regulated industry that provides assistance to a relatively small number of people. On the other hand, precisely because it will be helping far fewer people than projected, it might well cost significantly less than anticipated. I would expect this departure from what was projected to lead to two sorts of pressures:

(1) There will be a claim from ACA supporters that we can use the savings to increase subsidies or the domain of the subsidies beyond the 400% of Federal Poverty Line cutoff and thereby reduce the adverse selection problem that will already be manifesting itself.

(2) There will be a claim from ACA detractors that all of this confirms that, apart from ideological considerations, the bill is an expensive turkey and that, if the only way to save it is to impose more and more regulation and spend more and more money, it ought simply to be repealed.

Complicating factors

Rules

There are many factors that could result in the estimates provided in this entry being quite wrong. I do not want to fall into the same trap as others who have ventured into this field and claim that there are not very large error bars around all of these numbers. And I do not believe the system is necessarily linear. It may be that small changes have cascading effects. Here are several reasons my estimates might be wrong.

1. The rules change in 2015. There are at least three significant rule changes in 2015.

a. The tax under 26 U.S.C. 5000A for not having government-approved health insurance increases significantly, going from the greater of $95 per person or 1% of household income to the greater $295 per person or 2% of household income. Insurers may therefore assume that enrollment will be greater in 2015 than in 2014. Some people will be pushed over the edge by the higher tax rate into purchasing health insurance. If so, insurers may feel less pressure to increase prices because they believe their experience in 2014 will not be repeated in 2015.

b. The employer mandate will presumably not be delayed again by executive order which may have two offsetting events: employers reducing the number of full time employees thereby adding more to the Exchanges or employers maintaining health insurance thereby reducing the potential pool for the Exchanges.

c. As discussed in an earlier blog entry, there will be a decline in transitional reinsurance now provided free to insurers in the Exchange which, in and of itself, will put significant pressure on premiums

Realities

Finally, this is a field where events just frequently overtake predictions. All of these predictions go out the window, for example:

a. if there is a major security breach in the government computer systems and people’s personal information is disclosed;

b. healthcare.gov continues to seriously malfunction during the critical pre-December 23 sign up period

d. if people find, as some are projecting (here and here), that the set of medical providers available in the Exchange policies is drastically reduced over what they expected; and

e. there is a major sea change in legislative power in Washington.

HHS is planning to cut reinsurance payments to insurers participating in its Exchanges in a way that, in and of itself, could increase gross premiums 7-8% in 2015 and increase the risk of further adverse selection

HHS has validated the claims of insurers that President Obama’s recent about-face on the ability of insurers to renew certain policies not providing Essential Health Benefits could destabilize the insurance market. The Notice proposes changing the way insurers calculate their profits and losses so that the amount of payments made by government to insurers in the Exchange would increase. It claims, however, that it does not know how much this will cost.

The HHS Notice for 2015

Less reinsurance

Under the system in place for 2014, if insurers in an Exchange have to pay between $45,000 and $250,000 on one of their insureds, the government picks up 80% of that loss (assuming the $63 per insured life it taxes various other health insurance plans is sufficient to pay that amount). But in 2015, the money that goes into this transitional reinsurance pool (section 1341 of the ACA, 42 U.S.C. sec. 18061) declines by a third from $12 billion to $8 billion and the head tax correspondingly declines from $63 to $44. As a result, HHS proposes to now pick up only 50% of the tab for losses between $70,000 and $250,000. Thus, losses between $45,000 and the new $70,000 attachment point will now fall entirely on insurers without federal help and insurers will have to pay 30% more on losses between $70,000 and $250,000.

This reduction in free reinsurance provided by the taxpayers will almost certainly result in increased premiums for insureds. My estimate is that the average premium hike induced by this reduction in reinsurance is likely to be about 7-8%.

Here’s how I did this computation. I took loss distributions contained in the government’s “Actuarial Value Calculator.” That’s the Excel spreadsheet the government (and insurers) use to figure out what metal tier, if any, their policy falls into. I then performed the following steps. You can verify what I have done in the Computable Document Format (CDF) document I have placed on Dropbox. You can view the document using the free CDF player or using Mathematica

Step 1. I determined the expected value of claims under those loss distributions with reinsurance parameters set at the 2014 rates. I get four results, one for each metal tier: {3630.52, 4223.87, 4468.95, 5556.06}. I then do exactly the same computation but use the 2015 reinsurance parameters. I get four results, one for each metal tier: {3906.67, 4550.95, 4807.06, 5948.53}.

Step 2. I multiply each result by the actuarial value of the associated metal tier to approximate the size of the premium needed to support the expected level of the claims. I get {2178.31, 2956.71, 3575.16, 5000.46} for the 2014 reinsurance parameters and {2344., 3185.67, 3845.65, 5353.68} for the 2015 reinsurance parameters.

Step 3. I then simply compute the percent increase in the needed 2015 premiums over the needed 2014 premiums and get {0.0760631, 0.077436, 0.0756584, 0.0706371}

If losses are, as I suspect they will be, greater than those assumed in the actuarial value calculator — because the pool is going to be drawn for a variety of reasons from a riskier group than originally anticipated — the diminution in reinsurance is yet more significant and, standing by itself, could add more than 7-8% to the gross premiums charged in the Exchanges.

Whether the increase in gross premiums is about 7-8% or whether it is higher, it creates a heightened risk for an adverse selection problem. This is so because, although subsidies insulate many people in the Exchanges from increases in gross premiums — net premiums are pegged to income rather than gross premiums for them — it will affect the significant number (estimated by HHS to be about 18% (4/22)) who are expected to purchase policies inside the Exchanges without subsidies. The higher premiums go, however, the more we would expect to see the healthy drop out and find substitutes for the non-underwritten policies sold in the Exchanges. (If premiums are low enough, adverse selection is not a problem: insurance is a good deal for everyone and healthy and sick purchase it alike. See, e.g., Medicare Part B, which is very heavily subsidized and does not suffer seriously from adverse selection.)

Note to experts. Some of you might think I erred in saying that the 2014 reinsurance attachment point is $45,000 and not $60,000. But the 2015 notice says on page 11 that it will retroactively reduce the attachment point to $45,000.

HHS Validates Insurer Fears About Obama Reversal and the Destabilization of Insurance Markets

Many individuals, including me, have claimed that President Obama’s recent decision to permit insurers to “uncancel” certain individual plans that do not contain Essential Health Benefits could destabilize insurance markets. The Notice of Benefit and Payment Parameters just released appears to validate that assertion. Stripped of bureaucratese, the HHS document basically says that insurers are right to be disconcerted by the President’s about face.

For those who enjoy bureaucratese, however, or who properly want to validate my own conclusions about the document, here’s what it actually says.

On November 14, 2013, the Federal government announced a policy under which it will not consider certain non-grandfathered health insurance coverage in the individual or small group market renewed between January 1, 2014, and October 1, 2014, under certain conditions to be out of compliance with specified 2014 market rules, and requested that States adopt a similar non-enforcement policy.

Issuers have set their 2014 premiums for individual and small group market plans by estimating the health risk of enrollees across all of their plans in the respective markets, in accordance with the single risk pool requirement at 45 CFR 156.80. These estimates assumed that individuals currently enrolled in the transitional plans described above would participate in the single risk pools applicable to all non-grandfathered individual and small group plans, respectively (or a merged risk pool, if required by the State). Individuals who elect to continue coverage in a transitional plan (forgoing premium tax credits and cost-sharing reductions that might be available through an Exchange plan, and the essential health benefits package offered by plans compliant with the 2014 market rules, and perhaps taking advantage of the underwritten premiums offered by the transitional plan) may have lower health risk, on average, than enrollees in individual and small group plans subject to the 2014 market rules.

If lower health risk individuals remain in a separate risk pool, the transitional policy could increase an issuer’s average expected claims cost for plans that comply with the 2014 market rules. Because issuers would have set premiums for QHPs in accordance with 45 CFR 156.80 based on a risk pool assumed to include the potentially lower health risk individuals that enroll in the transitional plans, an increase in expected claims costs could lead to unexpected losses.

So, the government wants help in figuring out what to do. One method it is contemplating involves technical adjustments to the Risk Corridors program in a way that would get insurers more money (pp. 101-105). Although I will confess to considerable difficulty in understanding exactly what it is that HHS suggesting, the basic idea, as I understand it, would be to assume that those who, by virtue of the President’s about face, “uncancel” their policies would have had claims expenses equal to 80% of the average claims of the rest of the pool (page 103-04). HHS will then, on a state-by-state basis figure out what the position of the insurer would have been and try to adjust Risk Corridors such that the position of the insured after application of adjusted Risk Corridors is similar to that which it would have been in had these persons, who pay the same premium as the rest but who tend to have only 80% of the claims expenditures, enrolled in their plan.

It is not clear to me where the statutory authority to make this change comes from. Section 1342 of the ACA (42 U.S.C. 18062) does not define its key terms of “target amount” and “allowable costs” in a fashion that would appear to my eye to extend to hypothetical costs and hypothetical premiums. I will also confess to being unsure as to who would have standing to challenge this proposed give away of taxpayer money to the insurance industry.

What is clear to me, however, is the proposed reform, by necessity, will result in greater previously unbudgeted expenditures by the federal government. If we are really talking about making insurers whole and the people in question might have profited insurers something like $1,000 a person, the federal government appears to be suggesting a change in regulations that could cost it hundreds of millions of dollars. The HHS Notice declines to put an exact figure on the cost of the change:

Because of the difficulty associated with predicting State enforcement of 2014 market rules and estimating the enrollment in transitional plans and in QHPs, we cannot estimate the magnitude of this impact on aggregate risk corridors payments and charges at this time.

HHS is probably correct in saying it is difficult to estimate the cost of the proposed changes to Risk Corridors. I don’t think we have a good feel for how many people will return to the plans President Obama has carved out for special treatment. It does look, however, as if a floor of a couple of hundred million dollars on the cost of the proposal would be quite reasonable. This, of course, could give some ammunition to those, such as Florida Senator Marco Rubio, who have called for repeal of the Risk Corridors provision as an insurance “bailout.” (For a discussion, look here, here and here)

Final Note

Yesterday, I said I hoped to provide a major post. This actually is not the post I was speaking about. There’s still more news coming. Maybe today or maybe while recovering from a turkey overdose tomorrow.

Let us suppose, for the moment, that enrollment in the Exchanges increases as healthcare.gov becomes less dysfunctional and as we get closer to the January 1, 2014 and March 1, 2014 deadlines. It is, after all, unrealistic to think that enrollment will remain at the pathetic/paltry/miserable levels recounted by today’s testimony from Kathleen Sebelius, notwithstanding her counting of people who merely put a plan in their shopping cart. But it does seem likely to many , including me, that

sticker shock,

the small and difficult-to-enforce penalties for 2014,

President Obama’s decision to let insurers “uncancel” ungrandfatherable policies and let some of those insureds stay out the Exchanges,

will likewise lead the enrollment in the Exchanges to be considerably smaller than projected. This is particularly likely to remain true, I believe, in states such as Texas in which institutional forces and political culture often do not encourage participation and in which fewer than 3,000 out the estimated 3,000,000 eligible to do so have enrolled thus far.

The key question is how resilient are the Exchanges to low enrollments in which, one would expect, the enrollees are — even more than they were projected to be — disproportionately older and disproportionately less healthy. And have the Exchanges been rendered yet more fragile by what many cheered as the surprisingly low premiums charged by many insurers? Could those insurers, who are likely to swoop up most of the business in a price sensitive market, in fact be about to face the winners curse? The answer to these questions may lie deep in the details of one of the least studied and yet one of the most important set of provisions in the Affordable Care Act: the reinsurance and risk adjustment provisions contained in sections 1341-1343 of that Act and now codified at 42 U.S.C. §§ 18061-18063.

Here’s the (long) paragraph-length explanation of how these reinsurance and risk adjustment provisions work. 42 U.S.C. § 18061 basically creates a transitional (2014-16) government operated stop-loss reinsurance program funded out of a special tax on other health plans ($63 per covered life). The reinsurance attaches when a person covered by a plan in an Exchange incurs $60,000 or more in claims per year. After that point, the reinsurer pays for 80% of the claims up to a cap of $250,000. Thus, if an individual had claims of $180,000 in a year, the government would reimburse the insurer for $96,000, which is 80% of the difference between $180,000 and $60,000. What this provision appears to do is make insurer profit and loss less sensitive to attracting high claims insureds. 42 U.S.C. § 18062 basically redistributes money in a complex way from insurers whose Exchange plans profit to insurers whose Exchange plans lose money. Again, the idea is to reduce the insurer anxiety either that their plan and their marketing (if any) happens to attract an unhealthy pool or that they selected a premium too low for the actual risk that materializes. Finally, 42 U.S.C. § 18063, the only program that is supposed to persist past 2016, imagines an incredibly complex system in which the risk posed by an insurer’s pool is assessed and the states or, in their default, the federal government (see 42 U.S.C. 18041(c)(1)(B)(ii)(II)), transfers at least some money from those with the riskiest pools to those with the least.

Will these provisions really rescue the insurers?

All of this might seem a comfort to insurers that might permit them to survive and continue in the Exchanges even if the pools are, on average, considerably more expensive than originally projected. But to get a better handle on the degree of solace these provisions might provide, we need to look at some of the limitations of these programs and the actual numbers.

Stop-loss reinsurance under 42 U.S.C. § 18061

First, let’s look at how much risk the transitional reinsurance provided by 42 U.S.C. § 18061 really slurps up. What I contend is that while this provision should — and probably did — lower the premiums the insurer would otherwise need to charge to avoid losing money, it does less to rescue insurers if the pool is less healthy than they foresaw. While to really see this, we need to get deep into the weeds and do some math, I’m going to hold off on that fun for now. We have to save some things, such as the Actuarial Value Calculator, for other blog entries. I believe I have developed a plain English explanation that gets us most of the way there.

The key concept is to recognize that sophisticated insurers (are there other kinds?) took the free reinsurance into account when they priced their policies. They computed an expected value of the reinsurance reimbursements and lowered their rates by something approximating that amount. They were able to charge lower rates than they otherwise would because some of the claims bill would be picked up by the government. But this does not mean that the insurers end up having profits that are insensitive to the actual claims incurred by their pool. Unless all of the higher-than-expected claims are stuffed into the zone in which the reinsurance kicks in ($60,000 to $250,000), the insurers will be hurt when the pool has higher claims than expected. But such an assumption is incredibly implausible. If the insurer assumed that only, say, 2% of its insureds would have claims between $20,000 and $25,000 but, as it turns out, 4% of its insureds have such claims, nothing in 42 U.S.C. § 18061 will help such an insurer with that unanticipated loss. Moreover, because the reinsurance even within the relevant zone is incomplete, the insurer will lose money if claims between $60,000 and $250,000 are higher than expected. The effect of the transitional stop-loss reinsurance on reducing the consequences of adverse selection is thus likely to be small.

In the end, what this transitional reinsurance mostly does is mostly to tax non-Exchange policies $63 per covered life in order to make policies within the Exchange more attractive to policyholders. And, yes, that fact should make Exchange-based policies cheaper and reduce the problem of adverse selection. After all, if the insurance were free presumably there would be little adverse selection — everyone would get it. But the reinsurance fails to reduce insurer vulnerability to adverse selection much more than, say, providing more generous tax credits and cost sharing reductions would have done. If the pool ends up being less healthy than the insurer anticipated — an almost certain consequence of lower-than-expected enrollments, 42 U.S.C. § 18061 is hardly going to end up relieving the insurer of most of the unhappy consequences of having written policies in that environment.

Footnote: There is one more wrinkle, but it only means that the transitional reinsurance is a yet weaker rescue vehicle: the government’s obligations under the transitional reinsurance provisions are limited. There’s “only” $12 billion in 2014 and this ramps down to $4 billion in 2015. If those amounts aren’t adequate to pay reinsurance claims, each claim gets reduced pro rata. The reason I relegate this point to a “footnote,” however, is that if the pools are really small then even if claims per person are way higher than expected, the aggregate amount of claims in the reinsured zone of $60,000 to $250,000 aren’t going to be that big. My back-of-the-envelope computation suggests that the $12 billion allocated for transitional reinsurance should not be insufficient unless at least 2 million people enroll on the exchanges; since right now we are almost certainly at less than 100,000, 2 million seems a lot of insureds away.

“Risk Corridors” under 42 U.S.C. § 18062

The biggie in this field is the “Risk Corridors” provisions contained in 42 U.S.C. § 18062. It essentially creates this massive transfer scheme, taking money from insurers who had profitable pools and giving it to those who did not. In some sense, it converts insurers from entities bearing risk to mere fronts for government funded health insurance. If I were prone to accuse the Affordable Care Act of creating “socialized medicine,” my Exhibit A would be the stealth “Risk Corridors” provision of 42 U.S.C. § 18062.

The graphic below shows how the scheme works. The x-axis of the graph shows hypothetical aggregate net premiums (what 18062 calls “the target amount”) an insurer might receive for some plan in some state. The y-axis shows the profits the insurer receives as a function of those aggregate net premiums assuming that claims (a/k/a “allowable costs”) are $11.4 million. The purple line shows what profits would have been as a function of premiums if 42 U.S.C. sec. 18062 did not exist. The blue line shows what profits will be after the payments required by 42 U.S.C. 18062 are taken into account. The khaki-shaded zone shows the payments insurers are supposed to receive (and the Secretary of HHS supposed to pay) under the statute. The green zone shows the payments insurers are supposed to make (and the Secretary of HHS supposed to receive) under the statute.

Profit as a function of premiums before and after 42 USC 18062

We can create a similar graphic in which the role of claims and premiums is reversed. The x-axis of the graph shows hypothetical aggregate claims costs (what 18062 calls “the allowable costs”) an insurer might receive for some plan in some state. The y-axis shows the profits the insurer receives as a function of those aggregate claims costs assuming that net premiums are $8.6 million. The purple line again shows what profits would have been as a function of premiums if 42 U.S.C. sec. 18062 did not exist. The blue line again shows what profits will be after the payments required by 42 U.S.C. 18062 are taken into account. The khaki-shaded zone again shows the payments insurers are supposed to receive (and the Secretary of HHS supposed to pay) under the statute. The green zone again shows the payments insurers are supposed to make (and the Secretary of HHS supposed to receive) under the statute.

Insurers profits as a function of claims before and after 42 USC 18062

If one looks at the slope of the blue lines — the ones that show profits after 18062 risk corridors are taken into account — they are much less steep for most of the domain than the purple lines — the one that show profits before 18062 risk corridors are taken into account. What this means is that, in some sense, it doesn’t matter to insurers all that much whether they price too low or too high, whether claims are lower than they thought or — due to adverse selection or otherwise — higher than they thought. Either they are going to pay money to the government or they are going to get money from the government. The risk of writing policies in the Exchange is greatly diminished.

In some sense, then, if section 18062 (1342) is fully implemented — an issue to which I will shortly return — insurers don’t act very much as profit-making enterprises within the Exchange making or losing money on the spread between premiums and claims. (This is even more true after the corporate income tax is taken into account) Instead, they are almost fronting for the government, providing their license, their claims processing abilities and their credibility to a scheme in which the government really bears the risk associated with the new Exchange-based system of providing insurance. A cynic might term the Exchanges as having gone 80% of the way towards a single payor system in which there is but minor variation in the benefits offered by insurance policies and claims processing contracted out to various insurance companies with the experience to do so.

The incentives issue

There are several implications of this consideration of 42 U.S.C. 18062. The first is to consider what incentives the system sets up for insurers. My tentative belief is that it incentivizes insurers to offer a low premium if they want to go into the Exchanges and this statutory provision may explain in substantial part why insurers priced their policies at rates lower than most expected. Let me see if I can sketch out the argument. If the insurer prices high, they are going to get very little business. Other insurers will take their business away by going low. If they price low, they will get a lot of the business. Sure, they may lose money if they price too low, but, if so, the government will reimburse them for most of their losses. And if they price right or still too high, they can make some money.