The Congressional Budget Office issued a report this week revising its February projections of the cost of the Affordable Care Act. Although there is much to discuss regarding the report, I want to focus here on its troubling discussion of “Risk Corridors.” That’s the part of the law under which the federal government reimburses insurers selling policies on the new Exchanges for sizable fractions of their losses. It also taxes insurers if they happen to make money selling policies on the new Exchanges. Between February and April, the CBO estimated cost of Risk Corridors jumped $8 billion. In February, Risk Corridors were predicted to make the government a net of $8 billion over the three years of the program. Now, Risk Corridors are expected to net the government nothing. The CBO claims that this jump was caused by regulations issued by the Obama administration in March that drove up the cost of the program.

There’s a second explanation, however, for the $8 billion change between February and April that’s possibly more troubling. This past February I wrote a blog entry with a lot of math explaining that the CBO prior analysis of the Risk Corridors provision was baffling and rested on extremely dubious and factually unsupported assumptions about the profitability of insurers selling on the Exchanges. That error, if it was one, was particularly salient because it ended up forestalling growing efforts within Congress to repeal Risk Corridors as an unwarranted “bailout” of the insurance industry. Could it be that with the repeal threat gone, CBO is now using the “noise” created by an Obamacare regulation as cover for rectifying the unduly optimistic assumptions it made back in February regarding Risk Corridors? That would be very troubling, because while math errors merely challenge the CBO’s competence, the alternative behavior about which I am speculating here goes to something more important: the CBO’s integrity.

The CBO explanation means the Obama administration shoveled $8 billion to insurers through a regulatory “tweak”

The official explanation from the CBO on its change of $8 billion in the cost of Risk Corridors is as follows:

“In March 2014, the Department of Health and Human Services issued a final regulation stating that its implementation of the risk corridor program will result in equal payments to and from the government, and thus will have no net budgetary effect. CBO believes that the Administration has sufficient flexibility to ensure that payments to insurers will approximately equal payments from insurers to the federal government and thus that the program will have no net budgetary effect over the three years of its operation. (Previously, CBO had estimated that the risk corridor program would yield net budgetary savings of $8 billion).”

So, if the CBO is to be believed, the change isn’t due to any earlier error, but due to an administration regulation promulgated by the Obama administration that has resulted in a net of $8 billion more going to insurers. That’s a big change for several reasons. First, it means that the regulatory changes instituted by the Obama administration cost the federal government $8 billion. All of that money went to the insurance industry. And so, in March of 2014, without much fanfare, the Obama administration would in effect have written a check to the insurance industry for $8 billion. That payment would only have been motivated by one thing: a desire to keep insurers pacified and in the Exchanges after having deprived them of perhaps their most healthy potential insureds by a prior administrative ruling — in violation of the ACA — that insurers could keep selling non-compliant policies. The $8 billion would thus have been “damages” paid by the taxpayer in order to permit the President to honor his campaign promise that if you liked your insurance plan you could keep it.

In short, if you believe the CBO, a regulation for which statutory support will be extremely hard to find, resulted in the government shoveling $8 billion to insurers, basically to pacify them for the losses they suffered as a result of further regulatory changes of dubious legality. The Obama administration can not afford to have its signature program enter a death spiral as a result of regulatory actions that, while mollifying those who otherwise would have lost their health insurance coverage, caused insurers to lose more money in the Exchanges. And, again, the Obama administration did so in a clever way that made it difficult for anyone to have legal standing to challenge them. So far as I can discern, no insurer will be worse off as a result of the March 2014 regulatory changes. The real victims are taxpayers with diffuse interests and, of course, the Rule of Law.

The CBO math is still baffling

A second reason the change by the CBO is big comes from a look at the math. As I said in my February 2014 post calling the CBO February report “baffling,” consider the implications of asserting that the insurers would make so much money on the Exchanges that they would, on net owe the federal government $8 billion. If you do the math, it means that the CBO assumed that, over the course of three years, insurers would be earning about 8 cents on every dollar they earned via policies sold on the Exchanges. I just ran the numbers again and came up with a very similar conclusion: the earlier estimate could only be true if insurers were supposed to make a hefty 8% or greater return on premiums. That estimate of 8 cents on the dollar was really peculiar at the time because enrollment — let alone actually paying customers — was running seriously behind projections and the number of “young invincibles” was particularly low. Low overall insurance purchases and particularly low rates of purchases by the people who were most needed in the Exchanges caused many people to believe back in February that insurers would hardly make hefty profits and pay money to the government under Risk Corridors. Instead, they thought insurers would fare poorly and probably have to be subsidized (or “bailed out”) by the government.

The effect of the February CBO pronouncement was to dampen enthusiasm for a bill proposed by Senator Marco Rubio that would have repealed the Risk Corridors provision as a bailout to the insurance industry. If, after all, the federal government was, on balance, making money on Risk Corridors, it was hard to see it as a “bailout” to the insurance industry. Whether intended or not, the political effect of the February CBO announcement was to pull the rug out from one justification for repeal of Risk Corridors.

But is it even plausible to believe that the regulatory change made by the Obama administration in March without the approval of Congress could cause such a large change in the Risk Corridors program? I have done the math again and the answer is no. I do not see how it is possible to get $8 billion out of the regulatory tweak that was made. Again, the calculations are baffling.

Here’s how we know. The $8 billion the CBO thought back in February the government would make off of Risk Corridors represents about 4% of the premiums insurers on the Exchanges would take in during that time period. One can use that and other information from the CBO to reverse out a distribution for “allowable costs” (basically claims expenses) We can thus make a respectable estimate of how many insurers would make money on the Exchanges, how many would lose, and how much these insurers would gain and lose. I describe the gory process in my post from February. Call this distribution the CBO Insurer Profitability Distribution. Then assume the government tweaks, as it did, two regulatory parameters used in the computation of Risk Corridor payments, changing something called a profit margin floor from 0.03 to 0.05 and changing an “administrative cost cap” from 0.2 to 0.22. If one then takes the CBO Insurer Profitability Distribution and computes how much the government would now make on Risk Corridors does one emerge with the CBO’s new prediction that Risk Corridors will produce no net revenue? No! One gets that the Risk Corridors program now generates about 2.8% of premiums for the government. In other words, the reduction in Risk Corridor revenue resulting from the administrative tweak is only 1/3 of what the government claims.

The easier way to reach the CBO’s April’s conclusion is to assume that the gain of $8 billion resulted from two phenomena: (1) the regulatory tweak mentioned by the CBO and discussed above, but (2) a recognition that the CBO Insurer Probability Distribution the CBO had used in February was, as I have said, wrong. If, for example, one assumes that insurer claims were about 6% higher than the CBO estimated in February, the regulatory tweaks combined with higher insurer claims expenses indeed generate an $8 billion shift in the amount of revenue the government would make on Risk Corridors.

For those interested in the details, I link here to a Mathematica notebook showing the computations; I try to avoid black boxes.

Conclusion

So, what are we to make of this apparent discrepancy between the CBO’s explanation of its change in estimates and the actual effects of the regulatory changes it asserts to be the cause ? It could, I suppose, be my mistake. I have been careful and consider myself pretty knowledgable in this area, but I will hardly claim to be mathematically infallible. The problem is that the for ordinary Americans (like me), the CBO is a black box. It is not subject to the Freedom of Information Act and it does not publish enough of its methodology for even experts in the field to figure out what it is doing. That, I would submit, is a real problem for the democratic process, where the fate of legislation depends essentially on trust rather than the Reagan doctrine of “trust but verify” (doveryai no proveryai, in the original Russian).

It could also, however, be a coverup for a mistake (or worse) back in February. There is, after all, an alternative explanation of the change in estimate. It was unrealistic all along for the CBO to think that insurers in the Exchange were going to make money on balance. That’s what I suggested in my February 2014 post. So, rather than admit that the it had been guilty of unwarranted optimism, the CBO simply used a new distribution of likely claims expenses, came up with a different answer, and used the March 2014 regulatory changes as a smokescreen.

I will confess, however, that I am very uncomfortable with conspiracy theories or with theories that are premised on people acting in bad faith. Nonetheless, I would not find it impossible to believe that a culture could emerge in a politically sensitive agency that was reluctant to expose forcefully the consequences of government programs that proved far more expensive and far less successful than forecast originally. It would be a culture in which good news, or optimistic speculation, was uncritically embraced. What I challenge the CBO to do, therefore, not only with the Risk Corridors analysis, which is but the tip of a very big iceberg, but with the entirety of its ACA analysis, is to open it up for scrutiny. When government policy is essentially set on the basis of models that are not subject to peer review or public scrutiny, there is a great chance for error and, frankly, for manipulation. Government by black box breeds suspicion.

Postscript: Is the tweak legal?

I have said before and I say again that the regulatory tweak that the CBO now says will cost the federal government $8 billion is extremely dubious. It’s an extremely sneaky way of sending money to the insurance industry, resting, as it does, on arcane manipulations of mathematical formulae. And I have serious doubts that the changes are authorized by Congress.The submission of the original regulations in March, 2013 says that essentially all commenters agreed that a 3% margin for profit was appropriate. No commenters indicated at that time that insurers were entitled to a higher imputed rate of return on capital. No one said anything about 5%. Back in March of 2013, HHS thought 3% was the right number. There has been no fundamental change in the capital markets since that time. The only thing that has changed is that the Obama administration has made the pool of insureds making purchases in the Exchanges less healthy on average. The regulatory “tweak” moving the profit margin from 3% to 5% is thus not consistent with the original goal of Congress for the Risk Corridors program, but is simply a way of compensating insurers for another regulatory change.

The change in the administrative cost cap from 20% to 22% that will likewise result in higher payments to insurers is likewise dubious. The reason 20% was suggested in the original July 2011 proposal and chosen in the March 2013 regulations was to maintain parity with regulations governing the “Medical Loss Ratio” codified at 42 U.S.C. § 300gg-18 as part of the ACA. The idea, which was apparently supported by commenters on the original rules, was that if insurers — even small group and individual insurers — could not claim more than 20% administrative costs without owing rebates pursuant to section 10101(f) of the ACA then they should not be able to claim more than 20% administrative costs under the Risk Corridors provision. Makes sense! But, again, nothing has changed. There is no indication that anything President Obama did that raised the administrative costs of running a health insurance plan on the Exchanges. There is no indication that any factor in the real world (such as the cost of computers or paper) increased the administrative costs of running a health insurance plan on the Exchanges. The limits for the Medical Loss Ratio computation have not changed. There is no better reason now then there was a year ago to let the cap on administrative costs be higher for Risk Corridors than it is for Medical Loss Ratio. And, yet, it is now 22% instead of 20%. The only reason it has changed is to provide a vehicle for shoveling money to insurers.

Again, unless one thinks that the goal of keeping insurers in the Exchange is so overwhelming as to permit the Executive Branch to do anything, it is difficult to see a conventional, lawful justification for the regulatory change that results, according to the CBO, in $8 billion of compensation to the insurance industry. And I say that believing fully well that many of the Obama administration’s other regulatory changes — also of dubious legality — such as expanding the hardship exemption and permitting insurers to sell policies off the Exchanges that contain prohibited provisions have significantly hurt insurers selling policies on the Exchanges. Two wrongs do not make a right.

Technical Appendix

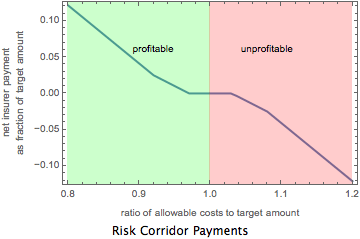

The following graphic shows the relationship between the Risk Corridor Ratio and the net receipts of the government for each premium dollar. As one can see, the higher the Risk Corridors Ratio, the less money the government receives or, in some instances, the more money the government pays out.

The following graphic compares the relationship between claims costs (“allowable costs”) incurred by an insurer as a percentage of premiums and the Risk Corridors Ratio. It does so for two sets of regulatory parameters. It first uses the regulatory parameters that were in place prior to March of 2014 (3% profit margin and 20% administrative cost cap). It next using the new regulatory parameters (5% profit margin and 22% administrative cost cap). As one can see, the regulatory changes increased the Risk Corridors Ratio for all levels of allowed costs and thus decreased the amount the government would receive from insurers (or increased the amount the government would pay to insurers).