Contrary to the views of some, the number of people who have insurance coverage through the Exchanges as of January 1, 2014, matters to everyone. It matters because the pool that exists on that date will determine, at least for a while, whether the premiums charged by insurers in the Exchange are likely to be stable and the extent of the federal government’s multiple obligations to subsidize plans purchased on the various Exchanges. It is not as if insurers get a claims paying holiday simply because more and healthier people may enroll later in the year. It also matters because a major point of the Affordable Care Act was to increase in an efficient and relatively painless way the net number of people who have insurance or social protection against significant illness. If the numbers in the Exchanges and in the expanded Medicaid program do not way more than offset the number of persons who lose their insurance as a result of the ACA, or if the cost of extending health protection in this fashion proves too high, the ACA will not have accomplished its goals.

Given the chaos that has erupted as procrastination strains Exchange infrastructure and deadlines are repeatedly extended, it is difficult to tell right now whether the ACA is performing as hoped. A few things are clear, however. The first thing is that the Obama administration is not releasing the sort of information from which an objective assessment could be made. Platitudes such as “Millions of Americans, despite the problems with the website, are now poised to be covered by quality affordable health insurance come New Year’s Day,” from President Obama at his last press conference are just not a substitute for knowing how many people have enrolled in the plans in the various Exchanges, and more importantly, have paid for coverage. What are their ages? How about some real numbers as a Holiday present?

Second, the Obama administration is acting as if a large number of enrollees in the aggregate is the measure of success. This is simply not true. Putting aside the problem of it being paying customers rather than mere enrollment that ultimately matters, meeting or exceeding projections in some states does not compensate for deficiencies in many other states. Because the pools are state-based, Texas insurers and insureds are not helped if enrollment in New York or Connecticut exchanges ultimately equals or exceeds targets. The insurance market in Texas and many other states will still be unstable with some insurers likely pressing for significant premium increases, contemplating withdrawal from the Exchanges, and demanding larger subsidies from the federal government via Risk Corridors and other programs.

Third, even those who have been on the more pessimistic side of matters, must acknowledge that there has indeed been a surge in many state Exchanges and in many states covered by the federal Exchange. On December 11, I wrote: “With a decent last minute kick, it is not unimaginable that California could make 1/3 of its total by the December 23, 2013 deadline and get closer to its ultimate goal by the end of March.” With enrollments at 17,000 per day, California may in fact be there. Colorado, which previously had dismal enrollment numbers, reports 33,356 enrolled as of Monday, which puts it at of the 136,000 projected enrollment for 2014 and 52% of the way towards the Obama administration’s projections for this time of the open enrollment season. (33356/(0.47 x 136000)). Other states such as New York and Connecticut, which previously were doing better than most, have also reported a high pace of enrollment.

Whether that surge has been as large in many other states remains to be seen. Proponents of the ACA like to cherry pick their states with at least as much zest as opponents do. Perhaps both sides share the belief that insurance enrollment is at least much a social phenomenon as a purely economic one. Numbers for large states (with large numbers of uninsureds) such as Texas, Florida, Georgia, Indiana, Illinois, North Carolina and Florida have yet to report any numbers that I have seen. And, as mentioned above, even if California and New York and some other states have enrollment sufficient to forestall premium instability and possible entrance into an adverse selection death spiral, that will not greatly help states in which enrollment ends up being less than half of that projected.

Finally, we need to look beyond the last minute holiday rush for health coverage and see what happens between now and March 31, 2014. The carrot of the ACA has basically been eaten for 2014. If you wanted health care coverage and could afford the prices on the Exchange it made little sense to wait until after the December deadline to acquire it. This is all the more true given that the President has permitted people to game the system by simply enrolling in a plan now and deciding until January 10, 2014, whether to pay.

Now, however, the first surge is likely over. Will there be the needed second surge? All that really remains is the stick: the individual mandate tax penalty. Many people, including me, believe that even before the events of last week, it was too small in 2014 to achieve its goal of inducing enrollment by those in good or average health. The number of people for whom insurance would not be a good deal at, say, $2,000 a year net but for whom it would be a good deal at (effectively) $1,705 per year ($2,000 – the $295 per person tax penalty) is not likely to be enormous. This is so because ACA premiums often depart greatly from actuarial risk by their prohibition on medical underwriting, accurate age rating, gender rating and their — shall we say — loose enforcement of tobacco rating.

Moreover, with the administration exempting last week upwards of half a million people from the individual mandate, the number of people who need fear the stick got even smaller. So, yes there are mega-procrastinators or people who have been stymied by the dysfunctionality of various Exchange website in obtaining coverage. There are former skeptics who see their neighbors helped by health insurance coverage under the ACA and who now enroll just as there may be some turned off by whatever problems emerge in administration of the plans. On balance, I would not be surprised to see modest increases in enrollment between now and the middle of March. I remain highly skeptical, however, that there will be a second surge equivalent to what has occurred this past week. As they say, however, only time will tell.

Personal Note

I am enjoying a family vacation in the Colorado mountains this winter holiday. It’s snowing outside my window as I write this and the beauty of a quiet snowfall can eclipse what may seem so important at other times. So please continue to read ACA Death Spiral periodically, but don’t expect a huge amount of activity for about the next week. I’m confident we’ll be back exploring issues in the new year.

The State of California is doing neither the best nor the worst when it comes to enrolling people in individual healthcare plans on its Exchange (Covered California), but it is doing the best job I have seen in releasing detailed information. In particular, it has released detailed information on the the age distribution of enrollees, “metal tiers” being selected by enrollees, subsidization rates, and the distribution of enrollees among insurance companies, and rates of enrollment among different language groups. Let’s look at the data and see what can be learned. And, other states, would you please do what California is doing. You have the data. It’s not that hard to put out the numbers.

Age Distribution

As shown in the paired bar graph below, the distribution of enrollees in individual Exchange plans by age in California is weighted far more heavily towards those in the older age brackets. There is, in particular, a dearth of children relative to the large numbers in the population and a disproportionately high number of those in the 55-64 age bracket.

Distribution of enrollees by age in California

The graphic here is less “bullish” on the enrollment of younger enrollees than Covered California would like to make it appear. This is because in various press releases, Covered California has been comparing the proportion of younger people enrolled against the proportion of younger people in the population and suggesting that they are similar. But this is highly misleading because the relevant statistic is the proportion of younger people in the eligible population. The elderly are not eligible to purchase policies on the Exchange. Thankfully, however, California has released the raw data that lets people do their own analyses. When the results are examined properly, in my opinion, the distribution of the young is more problematic.

Metal Tier Distribution

As noted in an earlier blog entry, a high proportion of purchases of Gold and Platinum policies could be worrisome because those policies are likely to be disproportionately purchased by those in poorer health. These policies generally have significantly less cost sharing than the Bronze and Silver policies. The chart below, taken from data provided by Covered California, shows that this concern has not materialized thus far in California. “Sub.” in the graphic shows policies that are eligible for subsidy under 26 U.S.C. § 36B and possibly under 42 U.S.C. § 18071 whereas “Unsub.” shows policies that are not eligible for subsidy. Silver is by far and away the most popular plan selected. And, contrary to earlier information released by California, which initially got matters backwards, subsidized policies are significantly more prevalent than unsubsidized ones.

Distribution of California enrollees by metal tier

Insurer Distribution

The pie chart below shows the distribution of enrollees by insurer. As one can see, enrollment in California has been dominated by large insurers. The top 4 insurers have 96.2% of the market. No small insurers have broken into the top 4. Moreover, some insurers are likely to have problems with the small absolute size of their pool if it does not increase significantly: Valley Health Plan has just 122 people enrolled to date in its health plans; Contra Costa Health Plan has just 178.

Distribution of California enrollees by insurer

Language Distribution

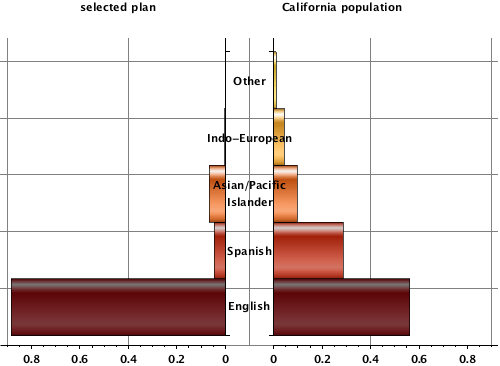

California has released information the primary language of enrollees. As shown in the paired bar graph below, the data demonstrates that English speaking individuals are enrolling at a rate significantly higher than those whose primary language is something else. People whose primary language is Spanish, for example, constitute 28.8% of the California population but only 4.6% of persons who have enrolled to date.

Distribution of California enrollees by primary language

The federal government announced today that 137,204 people have selected a healthcare plan through the federal Exchange as of November 30, 2013. The number is an increase over the 29,794 who had done so by the end of October, a month during which the website portal for enrollment, healthcare.gov, was in disarray. The government reports that 258,497 have now selected a plan through one of the state Exchanges, making a total of 364,682 enrolled. Asked by reporters whether the Obama administration stands by its estimate that 7 million will enroll in individual plans sold on the various Exchanges by March 31, 2013, the day necessary to do so in order to avoid a tax penalty, Michael Hash, director of the office of health reform in the federal Health and Human Services Department, said that they were “on track, and we will reach the total that we thought.”

The pace of enrollment announced by the federal government today is inconsistent with the claim that its 7 million goal will be achieved. The claim rests on hopes of two surges, one taking place over the next 12 days before the December 23, 2013, deadline for coverage starting January 1, 2014 and a second surge taking place as we approach the end of March at which point, if coverage has not been obtained, many Americans will be hit with a tax penalty.

The magnitude of the surge required strains credulity. A scenario in which most of those who wanted coverage have already applied and in which the pace of enrollment stays the same or even sags for lengthy periods as we go forward would appear almost as likely. Plus, it seems unlikely that there will be major enrollment between December 23, 2013, the first deadline, and March 23, 2014, the second deadline. If someone wanted coverage, they would try to get it earlier. What does applying in the middle of February accomplish? Moreover, if, given the unpredictability of human behavior, the surge actually materialized, it might well strain the government’s computer systems.

Analysis

There are many disturbing aspects to today’s release of numbers. First, forget for the moment about the March 2014 projection date and the March deadline. There are only 12 shopping days left before the pool will be closed for those who will have coverage as of January 1, 2014. Even if the pace of enrollment surges by a factor of 10 over what it was for the last two weeks on which we have data and healthcare.gov enrolls people at 45,000 per day, that would still put only about 668,000 persons enrolled through the federal Exchange as of that deadline. Even this rather cheery estimate would result in only 14% of the 4.8 million the Obama administration has projected will be enrolling in the federal Exchanges in 2014. The original projections for enrollment on opening day, January 1, 2014, were considerably higher, 3.3 million.

The number enrolled as of December 23, 2014, matters greatly. While of course there could be a second surge, in the mean time insurers are having to pay claims for three months on those first 14% to enroll. The initial enrollees are very likely to be comprised disproportionately of people with above average health care expenses. The result will be that, until that prayed-for second surge occurs, insurers will likely be losing large sums of money in the Exchanges and, ultimately, seeking reimbursement pursuant to the Risk Corridors program from the federal government and, derivatively, taxpayers.

Moreover, the aggregate numbers mask the fact that there are 50 different sets of Exchanges. While numbers are better in some, there are many jurisdictions in which there are huge problems. It is not “OK” if the Exchanges succeed in California, New York and a few other states if insurers and insureds in many other states suffer severe adverse selection problems that result in rapidly rising prices or reductions in availability.

Let’s look at a few states. I start with Texas. There, out of 780,959 projected to be enrolled, there are 14,038 as of the end of November. This is fewer than 2% of the ultimate projected amount. Even if one assumes that enrollments in Texas surge to go 20 times faster in December than they did in November, which is a pretty heroic assumption, this would still result in only 183,425 being enrolled as of the December 23 deadline. This would be only 23% of what needs to occur. It would be as if a football team were down 35-3 in the 3rd quarter and hoping to make a comeback. It could, I suppose, happen, and you shouldn’t turn off the TV set, but the probabilities are remote.

One might argue that Texas is an exceptional case due to the degree of hostility prevailing among many here about “Obamacare.” Take another fairly large state using the federal Exchange, Pennsylvania. There, we see 11,788 enrolled out of 268,858 ultimately projected, just 4.4%. To get to even 1/3 of the ultimate projected number being enrolled by December 23, the pace for December would have to be 6 times greater than it was in the last two weeks of November. Not impossible given procrastination, but again, a major challenge.

The figures when one looks to the various state Exchanges are a mixed bag. The poster child for the Obama administration would appear to be California. It has 107,087 of the 691,016 it ultimately hopes to enroll, over 15%. With a decent last minute kick, it is not unimaginable that California could make 1/3 of its total by the December 23, 2013 deadline and get closer to its ultimate goal by the end of March. But even with these better-than-average numbers, there is the risk of at least some adverse selection in a pool substantially smaller than projected. Also doing better than many is New York. There, we see 45,513 enrolled. But even this is but 11% of the 411,304 projected. It will again take a major surge over the next 12 days if New York were to get to even 1/4 of the ultimate projected enrollment by the December 23 first deadline.

But for every California or New York running its own show, there is an Oregon or a Maryland. These are large states in which enrollment is lagging. In Oregon, owing substantially to the collapse of its computer system, only 44 people have enrolled in plans on their Exchange. It will take an unimaginable surge there to make the system functional. Officials there and in Washington, D.C. will soon need to start contemplating what to do about a failed system; will, for example, tax penalties be imposed for those in Oregon who do not have health care coverage? In Maryland, where the director of the program recently quit, just 3,758 have enrolled out of 91,528 projected, just 4.1%. It goes beyond hope and into the realm of fantasy to believe that Maryland is not going to have a serious adverse selection problem starting January 1, 2014, when those 3,758 who penetrated the state’s application system start filing claims.

Finally, nowhere in the release do I see an age distribution of those enrolling. Unquestionably, the administration has this information. It is required in the enrollment process. And, perhaps this is a bit cynical, but I have to think that if those numbers looked good, if the hoped-for proportion of younger persons were enrolling, the Obama administration would release the information. I believe we are entitled to draw a negative inference from the fact that the information was not released that the pool is disproportionately elderly. If this is correct, what we are seeing is a small pool composed disproportionately of the elderly. That does not augur well for those who want to see the promises of the Affordable Care Act fulfilled.

An Experiment

HHS was kind enough to include a graphic in their report. Here it is.

Cumulative enrollment in the federal Exchange for various states

The graphic plots time on the x-axis and cumulative enrollment on the y-axis. Recognizing all the enormous problems with doing so, I thought it would still be interesting to try to fit a curve to the data and extrapolate it out to see where we might end up.

The short version is that if we extrapolate the curve using quadratic and cubic models, we end up at between 278,000 to 383,000 enrolled in the federal system by the December 23, 2013 first deadline. This would represent fewer than 10% of the ultimate projected enrollment and will create substantial adverse selection problems for at least the first three months of the program, particularly in the less enthusiastic states. This all assumes, of course, that all people who have selected a plan actually pay the premiums. The numbers could be worse. Regardless, insurers are going to be very concerned if these are the sort of numbers that materialize; the federal government better get out its Risk Corridors checkbook to help relieve the pain.

By March 23, 2013, however, the same models show we could be at 1.35 million to 3.94 million, depending on the model chosen. This would represent 28% to 82% of that originally projected and would cause serious adverse selection problems at 28% or mild adverse selection problems at 82%. I appreciate fully that these are large error bars but we just don’t have the data or an a priori model that permits me to extrapolate with any confidence this far into the future.

Here’s a graphic showing these results. The Mathematica notebook that generated them has been placed here on Dropbox.

The Los Angeles Times has reported that Covered California, the largest state’s health insurance exchange under the Affordable Care Act, has started releasing to insurance agents throughout the state the names and contact information of tens of thousands of persons who started an application using the state’s online system but failed to complete it. The Covered California director Peter Lee acknowledges the practice but says that the outreach program still complies with privacy laws and was reviewed by the exchange’s legal counsel. “I can see a lot of people will be comforted and relieved at getting the help they need to navigate a confusing process,” explained Lee.

I am hardly as confident as Covered California’s lawyers apparently were that this practice was legal. The law requires that disclosures to third parties be necessary and I do not see why Covered California could not have contacted non-completers directly and ask them if they wanted help from an insurance agent rather than disclosing their identify to insurance agents. But even if the practice could be said to be borderline legal, it is difficult to imagine a practice more likely to sabotage enrollment efforts in California — and, since California’s interpretation could be precedent for other states — elsewhere. For every person unable to complete their application online in California and who will, with the comforting help provided by insurance agents, now want to complete it, there are likely 10 who will be turned off by the cavalier attitude towards privacy exhibited by this government agency. Beyond a violation of ACA privacy safeguards, the action is either a sign of desperation about enrollment figures, even in a state that boasts of its success such as Peter Lee’s California, or monumental stupidity.

If California wanted to create an adverse selection death spiral, it would be difficult to be more effective than, without notice or consent, releasing personally identifiable information to insurance agents.

The Law

Let’s start with the Affordable Care Act itself. Section 1411(g)(2), codified at 42 U.S.C. § 18081(g)(2), reads

(g) CONFIDENTIALITY OF APPLICANT INFORMATION.—

(2) RECEIPT OF INFORMATION.—Any person who receives information provided by an applicant under subsection (b) (whether directly or by another person at the request of the applicant), or receives information from a Federal agency under subsection (c), (d), or (e), shall— (A) use the information only for the purposes of, and to the extent necessary in, ensuring the efficient operation of the Exchange, including verifying the eligibility of an individual to enroll through an Exchange or to claim a premium tax credit or cost-sharing reduction or the amount of the credit or reduction; and

(B) not disclose the information to any other person except as provided in this section.

Health and Human Services, one of the key agencies in charge of administering the Affordable Care Act has implemented this statutory provision in section 155.260 of Title 45 of the Code of Federal Regulations. It says:

§ 155.260 Privacy and security of personally identifiable information.

(a) Creation, collection, use and disclosure.

(1) Where the Exchange creates or collects personally identifiable information for the purposes of determining eligibility for enrollment in a qualified health plan; determining eligibility for other insurance affordability programs, as defined in 155.20; or determining eligibility for exemptions from the individual responsibility provisions in section 5000A of the Code, the Exchange may only use or disclose such personally identifiable information to the extent such information is necessary to carry out the functions described in § 155.200 of this subpart.

This regulation requires us to answer several questions: (1) was the information in question “personally identifiable information” ; (2) was it collected for one of the purposes set forth in subparagraph (a)(1); (3) and was its use or disclosure necessary to carry out a permitted function.

Did Covered California release personally identifiable information? Yes.

Section 155.260 of the Code of Federal Regulations does not appear to define personally identifiable information — although it is difficult to imagine anything that would fit it better than one’s name, address, phone number and email address. And, if one consults the Department of Labor, they say “PII” is:

Any representation of information that permits the identity of an individual to whom the information applies to be reasonably inferred by either direct or indirect means. Further, PII is defined as information: (i) that directly identifies an individual (e.g., name, address, social security number or other identifying number or code, telephone number, email address, etc.) or (ii) [omitted] Additionally, information permitting the physical or online contacting of a specific individual is the same as personally identifiable information. This information can be maintained in either paper, electronic or other media.

This definition fits what Covered California released to the letter.

Was it personal information collected for the right purpose? Yes

Apparently it is not just any collection of PII that triggers obligations under 155.260. It is collection for certain purposes. One of those purposes is “determining eligibility for enrollment in a qualified health plan.” It would surely appear that this was the purpose for which the information was provided. The individuals contacting the website were unlikely, except in peculiar cases, to be doing it for academic purposes or research. They wanted to find out whether they could get health insurance in an Exchange, what plans might be available, and what the price might be. That’s what everyone has been advertising as the purpose of the Exchange. And, although one would think this goes without saying, that’s the reason Covered California wanted the person’s name and other personally identifiable information. Covered California wanted to determine whether that person — not some anonymous shopper — was eligible and what plans were available to that person. Covered California wanted very much to be able to link the determinations made by the back end of the web site to the identity of the person requesting that the determination be made.

Was this a necessary disclosure? Dubious

If I were representing Peter Lee or others involved with this privacy incident, this is where I might want to rest my defense. (But if I were running other health insurance exchanges or hoping for the success of the ACA, I think I’d try to stop him from doing so). The regulation does not prohibit all uses of personally identifiable information. Nor does it actually prohibit release of the information outside of the health insurance exchange. Rather — and this may be as disturbing to some as the news of what Covered California has done — it actually authorizes external disclosure and external use under some circumstances.

First, the Exchange may only use or disclose such personally identifiable information only “to the extent such information is necessary to carry out the functions described in § 155.200 of this subpart.” When we leaf to section 155.200, we find it says the legitimate functions are those in various subparts of the regulations. The relevant parts, however, are determining eligibility for subsidies and actually enrolling in a plan. Since these two functions are, I believe, precisely what Covered California had in mind, it would not appear to violate these specific portions of the regulation to third parties so long as the purpose was eligibility determination and enrollment.

There are, however, at least three rebuttals to this argument that, standing alone, might suggest that Covered California’s actions were lawful.

Rebuttal 1: But surely this does not mean that Covered California could publish the names of incomplete enrollers in the Los Angeles Times or on some internet list and ask that the public help them out. The regulations also place limits on the persons to whom disclosure may be made. Read this part of section 155.260:

(b) Application to non-Exchange entities. … [W]hen collection, use or disclosure is not otherwise required by law, an Exchange must require the same or more stringent privacy and security standards (as § 155.260(a)) as a condition of contract or agreement with individuals or entities, such as Navigators, agents, and brokers, that:

(1) Gain access to personally identifiable information submitted to an Exchange; or

(2) Collect, use or disclose personally identifiable information gathered directly from applicants, qualified individuals, or enrollees while that individual or entity is performing the functions outlined in the agreement with the Exchange.

Thus, if the third parties themselves agree to abide by the privacy regulations, perhaps they could use personally identifiable information the same way as the Exchanges themselves might. But I have doubts that all the parties to whom the information was released had entered into such “subect-to agreements.” The Los Angeles Times article understandably leaves the issue a bit unclear, but it appears the disclosure of the information went in two stages, first to some agencies with whom California had pre-existing agreements and second to various insurance agents. While I would not be surprised if Covered California had “subject-to agreements” with the four agencies, I would be surprised if they had agreements with all to whom the second stage disclosure was met. This is a factual issue that will need to be resolved should a formal dispute arise over the release of the information.

Rebuttal 2: Just because one could disclose the information to certain third parties does not mean it was “necessary” to do so. Section 155.260(b) does not authorize all disclosures to third parties that have entered into subject-to agreements. Rather, it authorizes only necessary disclosures. Was it really necessary for third parties to contact these individuals? Why could Covered California not keep the matter in house and do it itself? They had the information. They could inform those individuals that if they wanted to contact an insurance agent, there was a list of authorized agents who could help them.

Which brings me to …

Rebuttal #3: There’s another provision in the regulations that needs to be considered: the idea of informed consent. Section 155.260(a)(3)(iv) states:

Individuals should be provided a reasonable opportunity and capability to make informed decisions about the collection, use, and disclosure of their personally identifiable information.

If the Los Angeles Times article is complete and accurate, this was not done here. There appears to have been no effort to ask enrollees whether, if they were unable to complete their enrollment, they wanted to be contacted by an insurance agent for help. Rather, contrary to the “informed decision” principle in (a)(3)(iv), Covered California just assumed that they would. And, although some web site users might indeed have wanted such assistance, many others, I suspect, would not want third parties with potential commercial motives and who may not have been well vetted informed about personal medical insurance and financial matters. The whole point of (a)(3)(iv) is that the individuals should have some notice and say about the matter. And it is that provision that appears to have been completely ignored here.

Legal conclusion

In the end, it appears to boil down to whether the disclosures to insurance agents was necessary and done in the right way. As to whether it was necessary, I have serious doubts. I don’t see why Covered California could not itself just have easily sent the incomplete enrollers a communication with a list of insurance agents. Moreover, even if many users would prefer that the communication flow go first to insurance agents and then to them, the language of the informed consent regulation indicates that notice of such a policy have been provided.

The stupidity

According to a recent poll published in the Christian Science Monitor, eighty percent of the American public say people should be concerned “about the security features of the Obamacare website.” Concerns about the security of the information inside the health care Exchanges has been fanned by many parties. The right wing (and sometimes the left wing) has repeatedly attacked the implementation of Affordable Care Act on grounds that giving Big Brother all this information about one’s finances, health and identity is dangerous. It is, they have warned, hardly immune from hackers. The government’s abysmal track record in construction of the web site hardly gives one confidence.

Moreover, whether exaggerated or not, fears about the security of the detailed financial and personal data that will ultimately lie inside the health care exchanges have some technological support. Sources that would ordinarily not be dismissed as kooky or overly politicized have repeated these warnings. Here are some from the Mitre Corporation, Popular Mechanics and Information Week. Mainstream media has noted the problem (CNBC, Fox News). Moreover, the fears have been amplified by commentators that, no matter what one may think of them, have large audiences that take what they say seriously. Here are some from Rush Limbaugh (“single biggest threat to individual security and identity security that we have in this country”), Sean Hannity (“we are hearing from security experts that the website is not safe”), Fox News (“it doesn’t look like anything was fixed from a security perspective”), Mother Jones (“According to several online security experts, Healthcare.gov, the portal where consumers in 35 states are being directed to obtain affordable health coverage, has a coding problem that could allow hackers to deploy a technique called “clickjacking,” where invisible links are planted on a legitimate web page.”).

Given the widespread concern and the dependency of the entire system on enough people risking their personally identifiable information in order to enroll in the health care exchanges under the Affordable Care Act, one would think government officials would be extraordinarily vigilant against hackers and others who would seek to take private information outside the Exchanges. One would think, all the more, that government itself would not be disclosing the information.

And this is what makes Covered California’s actions so mind-bogglingly stupid. Yes, releasing one’s name and email address might not be the same as releasing information about sexually transmitted diseases or the size of one’s bank account, it is still precisely the sort of information that many Americans seek to block others from having and give up only as absolutely necessary. And releasing information to insurance agents who promise to abide by privacy rules is not the same as posting names and addresses directly on the Internet. Even so, if government is to give this information out — to those whose bona fides may not always be known and who have a commercial motive to misuse the information — there better be an awfully good reason. Otherwise, those borderline people thinking about enrolling in an Exchange and on whom the whole of the Affordable Care Act really depends for its full success are going to think that the government places very little weight on privacy. It is that sort of thinking, perhaps as much as concerns about the economics of the Affordable Care Act, that risks driving the whole system into an adverse selection death spiral from which it will be unable to escape. It is hard to imagine the pressure Covered California must be under to meet enrollment goals that would cause it to lose sight of these central points.

Conclusion

Let’s end with a look at one final statutory provision: section 1411(h)(2) of the ACA. It says:

Any person who knowingly and willfully uses or discloses information in violation of subsection(g) shall be subject, in addition to any other penalties that may be prescribed by law, to a civil penalty of not more than $25,000.

I would suggest that Peter Lee of Covered California think very carefully about this provision. I would suggest that insurance agents like Warner Pacific Insurance Services in Westlake Village, an identified recipient of this information, think very carefully about it too before using it to contact individuals. Perhaps the Obama administration will choose to excuse this apparent breach of the law due to what they may regard as the good motivations of the violators, but if you multiply $25,000 by each phone call or email, it can really add up. Those involved in this release of information better hope that Covered California lawyer did some really good legal research and analysis before apparently giving the practice a clean bill of health.

Healthcare.gov appears to be working much better, at least in enabling individuals to select plans. And some of the state exchange web sites appear to be improving their functionality too. Some have heralded these advances as providing hope that the Exchanges will be able to meet the enrollment projections on which the economics of insurance without medical underwriting in part depend. But do these claims stand up to the cold light of mathematics? Not very well.

Here’s the headline:

A close look at the numbers shows that the pace of enrollments from here to the close of open enrollment needed to meet projections is high in every state, even those touted as successful, and almost impossibly high in many. Given the incredibly slow start in most jurisdictions, it will not just take a little pickup over the next few months to achieve the projected and needed number of persons in the Exchanges. It will take a miraculous last minute stampede. Since miracles seldom occur, the result may be two different stories of the Affordable Care Act: a few states in which the Exchanges proved from the start to be a somewhat stable mechanism for providing health insurance without medical underwriting but a significant number of other states in which the results for at least the first year represent a large failure.

Today’s news

News appears to be breaking today that the federal exchanges enrolled about 100,000 in November. This is being heralded as somewhat of a success compared to the 26,000 who enrolled in October. And, of course, enrollment figures from healthcare.gov are difficult to assess due to the actual and feared dysfunctionality of the web site. But one way to look at this is to consider what has to happen between December 1, 2013, and March 23, 2014, the close of open enrollment to make projections. The states that are dependent on healthcare.gov need about 4.84 million enrollees by the end of that period if the nation is to meet the goal of having 7 million enrolled in the Exchanges by the close of open enrollment. If, right now, there are about 126,000 enrollees in those states, we are just 2.5% of the way there. The pace of enrollment on healthcare.gov will need to increase by a factor of about 20 in order to meet goal. In absolute terms, healthcare.gov needs to be enrolling about 42,000 people per day. And while perhaps not every single one of those people need to enroll for the system to succeed, the 7 million enrollment goal isn’t just a mere wish. There are, as I and many others have noted potentially serious consequences to the stability of insurance markets if the figures fall well short, even in several states.

Whether healthcare.gov can score the needed come back, however, will basically depend on two related factors: (1) whether healthcare.gov is truly fixed and can stand up to the increased pace that will be needed and (2) whether the requisite increase in pace is likely. This latter factor depends in turn on where on the following spectrum the possibilities fall. On one end of the spectrum, there is the possibility that there is this pent up demand from procrastinators that will surge forward to access the web site in the coming weeks. Perhaps March Madness for 2014 will constitute this huge surge — kind of like April 15 rushes to the post office to send in tax returns — as the March 23 “deadline” approaches. On the other end of the spectrum, there is the possibility that most people who wanted to and had the means to enroll — the wealthy sick — did so already and others have looked at the prices, the coverages and the penalties and decided that, for now, Exchange coverage is not for them. The fact that a surprising 70% of current enrollees in the Exchange plans are unsubsidized gives some support to this gloomier hypothesis.

To get further insights, we can also take a closer look at some representative states.

Connecticut

First, let’s look at what has to happen in the most successful state, Connecticut. There, as of November 14, 2013 (the date of the last report), 7,591 people had selected a plan. That’s not all it will take finally to get coverage — among other things, people will have to start actually paying premiums — but it’s a solid start. This 7,591 figure represents 12.9% of the projected total of 58,637 for Connecticut. A little math shows that in order to make projections, people in Connecticut will need to enroll at a pace 2.3 times faster than they had as of November 14 in order to make the projection by the March 23, 2014 date.

It hardly seems impossible that Connecticut could make the projections. Whether they do so, however, will basically depend on the location of Connecticut on the spectrum discussed above. We should have a better sense of where on the spectrum we are falling when Connecticut releases new numbers.

Texas

Connecticut is a small state. The enrollment there was projected to constitute only about 1.4% of the total enrollment in the Exchanges. Let’s take a look at a big state: my home state of Texas. With the largest uninsured population in the country and with no Medicaid expansion into which some Exchange eligible persons might otherwise “fudge into,” Texas was supposed to enroll 780,959. As of November 2, 2014, Texas had enrolled just 2,991. This means that Texas will have to enroll at a pace 59 times faster than it had as of that date in order to meet enrollment projections. And, even if due to failure to the healthcare.gov website, Texas has enrolled, say, just 10,000 as of November 30, 2013, it will still need to up its pace by a factor of 41 in order to meet projections. Viewed in absolute terms, Texas will need to enroll at a pace of over 6,800 per day. Again, we will have a better sense of the plausibility of this increase when the federal government releases newer data.

Another way of thinking about the issue is to consider what would happen if Texas’ future enrollment relative to its prior enrollment is the same as Connecticut needs to be in order to meet the Connecticut projection. If Texas enrolls at a pace 2.3 times faster than it has thus far, Texas enrollment will be something like 29,000. That would be just 4% of what was originally projected, a shortfall of 752,000. Connecticut could double its projected enrollment and it would barely make a dent in compensating for a shortfall of this magnitude. Even if Texas celebrates the rebirth of healthcare.gov by stepping up its enrollment by a factor of 10, that still gives it less than 150,000 enrollees, a shortfall of 630,000 over the projected value.

It would also help if the government could get the Spanish language version of its website, cuidadodesalud.gov, to accept applications the same way that healthcare.gov does.

California

A problem with projecting Texas numbers is that it has been hamstrung by its chosen dependency on healthcare.gov, which has been completely dysfunctional until recently. So, what about a large state that shares some demographic characteristics of Texas but that has a mostly functional web site? Let’s look at California.

In California, as of November 19, 2013, there were 78,891 counted as enrolled relative to a projected enrollment as of March 23, 2014 of 691,016. Viewed one way, California is going to need to step up the pace of its enrollment by a factor of 3.07 in order to meet its target. In absolute terms, California needs a pace of about 4,936 per day (including weekends and including the busy holiday season) in order to meet target.

Whether viewed in relative or absolute terms, the pace needed in California is ambitious. Covered California, which brags of a recent tripling in the pace of enrollment, still enrolled just 2,700 per day for Exchange plans in the most recent period for which data currently exists. (It is only by counting Medicaid/Medical enrollments that the numbers get higher). If California were to persist at that pace for the remainder of the enrollment period, it would have something like 414,000 enrolled by the March 23, 2014 date. Depending on the precise composition of the pool of insureds, such a figure would likely be enough to stave off severe adverse selection but probably not enough to do so entirely. And, again, for those focusing on the 7 million nationwide figure, shortfalls of 277,000 in California or 700,000 in Texas are just difficult to compensate for even if other states are considerably more successful.

New York

Let’s pick one more big state. And, again, let’s pick one where the Exchange is generally said to be doing well: New York. In New York, as of November 24, 2013, 41,021 are claimed to have enrolled in plans out of the 411,304 originally projected. This means New York will have to quadruple the pace of enrollments (4.09) in order to meet projections. In absolute terms, the state needs to be enrolling 3,111 per day every day until March 23, 2014. It is thus in roughly the same position as California. Whether it meets its goals depends on why there has thus far been a shortfall. If it’s massive procrastination, perhaps New York can get pretty close. If, on the other hand, many New Yorkers are rejecting the product, and the pace of enrollment just doubles from what it has been, expect New York to fall short by about 190,000 people (46%). Again, smaller states that are more successful will have difficulty compensating for such a large absolute shortfall.

Conclusion

There is no state in which a significant uptick in the pace of enrollments will not be needed in order to meet enrollment projections. This is true in states that have their own Exchanges and states that do not. It is true in states touted as a success as well, of course, of those seen as failing. It is most definitely true for states that depend on the federal website, healthcare.gov.

In a few states, the burden may be met. Many people do indeed procrastinate, even perhaps when it comes to subsidized health insurance that they now lack. To meet enrollment projections in many other states,however, we need for Exchange applications to be far more the province of procrastinators than even income tax returns. After all, only 25% or so wait until the last two weeks to file those. In these other states, the appropriate analogy may not be tax procrastination but the miracle of The Heidi Game in which two touchdowns were scored in the closing 9 seconds after the mainstream media (NBC Sports) assumed the game was lost. But it’s been 45 years since that turnaround occurred. It just might happen again with applications for health insurance on the Exchanges, but it seems unlikely.

Could I add one more point?

People are focusing on March 23, 2014 (earlier March 15, 2014) as the measuring date. The ACA will presumably be deemed a success if enrollment figures meet projections by that date. But this strikes me as an awfully generous measure. The problem for insurers is that there will be a smaller pool during the first three months of the policy year. And smaller pools generally have higher claims per person. So, if I ran the world, I’d be looking at two dates to examine enrollments: January 1, 2014 when the plans kick in and March 23, 2014 when open enrollment ends. Yes, great enrollment by March 23 will ultimately go a long way to reassuring insurers if enrollment is problematic on New Years Day. But if enrollment is really bad come Rose Bowl time, expect insurers to lose a lot of money on claims filed between then and the close of open enrollment. If they can’t make that money back on the late filers, expect insurers to figure out some way of getting even for 2015.

As discussed yesterday on this blog and elsewhere in the media, Cover California, the state entity organizing enrollment there, has released data showing the age distribution of the group thus far enrolling in plans on its Exchanges. Although I took a rather cautionary tone about the age distribution — fearing it could stimulate adverse selection — the head of Cover California and some influential media outlets generally favorable to the Affordable Care Act have been considerably more cheerful. So, who’s right? For reasons I will now show — and probably to no one’s surprise — me. (More or less).

To do this, we need to do some math. It’s a more sophisticated variant of the back of the envelope computation I undertook earlier on this blog. The idea is to compute the mean profit of insurers in the Exchange as a function of the predicted versus the actual age distribution of the pool they insure. Conceptually, that’s not too difficult. Here are the steps.

1. Compute the premium that equilibrates the “expectation” of premiums and costs for the predicted age distribution of the pool they insure. Call that the “predicted equilibrating premium.”

2. Compute the expected profit of the insurer given the predicted equilibrating premium and the actual age distribution of the pool they insure.

3. Do Step 1 and Step 2 for a whole bunch (that’s the technical term) of combinations of predicted age distributions and actual age distributions.

Moving from concept to real numbers is not so easy. The challenge comes in getting reasonable data and, since there are an infinite number of age distributions and in developing a sensible parameterization of some subset of plausible distributions.

The Data

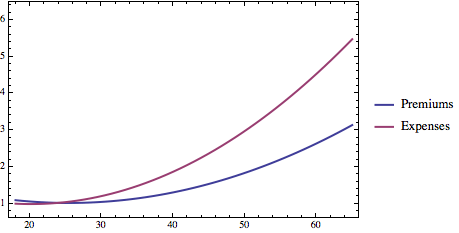

The data is interesting in and of itself. To get the relationship between premiums and age, I used the robust Kaiser Calculator. Since healthcare.gov itself recommends the web site (their own site seems to have a few problems) and I have personally validated its projected premiums for various groups against what I actually see from various vendors, I believe it is about as reliable a source of data as one is likely to find anywhere right now. So, by hitting the Kaiser Calculator with a few test cases and doing a linear model fit using Mathematica (or any other decent statistics package), we are able to find a mathematical function that well captures a (quadratic) relationship between age and premium. (The relationship isn’t “really” quadratic, but quadratics are easy to work with and fit the data very well.) The graphic below shows the result.

Nationwide average health insurance premium for a silver plan as a function of age

We can normalize the graphic and the relationship such that the premium at age 18 (the lowest age I consider) is 1 and everything else is expressed as a ratio of the premium at age 18. Here’s the new graphic. The vertical axis is now just expressed in ratios.

Nationwide average health insurance premium ratio for a silver plan as a function of age

To get the relationship between cost and age, I used a peer reviewed report from Health Services Research titled “The Lifetime Distribution of Health Care Costs.” It’s from 2004 but that should not matter much: although the absolute numbers have clearly escalated since that time, there is no reason to think that the age distribution has moved much. I can likewise do a linear model fit and find a quadratic function that fits well (R^2 = 0.982). Again, I can normalize the function so that its value at age 18 is 1 and everything else is expressed as a ratio of the average costs incurred by someone at age 18. Here’s a graphic showing the both the relationship between age and normalized premiums in the Exchanges under the Affordable Care Act and normalized costs.

The key thing to see is that health care claims escalate at a faster rate than health care premiums. Others have noted this point as well. They do so because the Affordable Care Act (42 U.S.C. § 300gg(a)(1)(A)(iii)) prohibits insurers from charging the oldest people in the Exchanges more than 3 times what they charge the youngest people. Reality, however, is under no such constraint.

Parameterizing the Age Distribution

There are an infinite number of potential age distributions for people purchasing health insurance. I can’t test all of them and I certainly can make a graph that shows profit as a function of every possible combination of two infinite possibilities. But, what I can do — and rather cleverly, if I say so myself — is to “triangulate” a distribution by saying how close it is to the age distribution of California as a whole and how close it is to the age distribution of those currently in the California Exchange pool. I’ll say a distribution has a “Pool Parameter Value” of 0 if it comes purely from California as a whole and has value of 1 if it comes purely from the California Exchange pool. A value of 0.4 means the distribution comes 40% from California as a whole and 60% from the current California Exchange pool. The animation below shows how the cumulative age distribution varies as the Pool Parameter Value changes.

How the age distribution varies as the pool goes from looking more like California as a whole to looking more like the current pool as a whole.

Equilibration and Results

The last step is to compute a function showing the equilibrium premium as a function of the predicted pool parameter value. We can then use this equilibrating premium to compute and graph profit as a function of both predicted pool parameter value and actual pool parameter value.

The figure below shows some of the Mathematica code used to accomplish this task.

Mathematica code used to produce graphic showing relationship between insurer profit in the California exchanges and the nature of the predicted pool and the actual pool

Stare at the graphic at the bottom. What it shows is that if, for example, California insurers based their premiums on the pool having a “parameter value” of 0 (looks like California) and the actual pool ends up having a “parameter value of 1 (looks like the current pool), they will, everything else being equal, lose something like 10% on their policies and probably need to raise rates by about 10% the following year. If, on the other hand, they thought the pool would have a parameter value of 0.5 and it ended up having a parameter value of 0.75 the insurers might lose only about 3.5%.

Bottom Line

If I were an insurer in California I’d be concerned about the age numbers coming in, but not panicked. First, I hope I did not assume that my pool of insureds would look like California as a whole. I had to assume some degree of adverse selection. But it does not look as though, even if I made a fairly substantial error, the losses will be that huge. That’s true without the Risk Corridors subsidies and it is all the more true with Risk Corridor subsidies.

What I would be losing sleep about, however, is that the pool I am getting is composed disproportionately of the sick of all ages. If I underestimated that adverse selection problem, I could be in deep problem. My profound discomfort would arise because, while I get to charge the aged somewhat more, I don’t get to charge the sick anymore. And there’s one fact that would be troubling me. Section 1101 of the Affordable Care Act established this thing calledthe Pre-Existing Condition Insurance Pool. It’s been in existence (losing boatloads of money) for the past three years. It held people who couldn’t get insurance because they had pre-existing conditions. They proved very expensive to insure. There are 16,000 Californians enrolled in that pool. But that pool ends on January 1, 2014. And the people in it have to be pretty motivated to get healthy insurance. Where are they going to go? If the answer is that a good chunk of the 79,000 people now enrolled in the California pool are former members of the PCIP, the insurers are in trouble unless they get a lot more healthy insureds to offset these individuals.

California has frequently been cited as an early Affordable Care Act success story with enrollment coming at least closer to projected numbers than in other states. Today’s release of information from Covered California, the state entity organizing enrollment there, shows a mixed picture about the likelihood that the ACA will become a stable source of non-discriminatory relatively inexpensive health insurance in the nation’s most populous state.

A highlight from the report is that 79,891 have at least gotten as far as selecting a plan since enrollment opened on October 1, 2013. That’s better than any other state and better — at least as of the last report — of all the other states combined using the healthcare.gov portal. And, because, contrary to the wishes of California Insurance Commissioner Dave Jones, Covered California has decided not to permit those with recently enrolled in underwritten individual health insurance to “uncancel” policies that do not provide Essential Health Benefits, there is the potential to add more people to the Exchange pools than would otherwise be possible. Additional good news: the pace of enrollment has picked up over the past two weeks. Still, to date, the 79,891 who have at least selected a plan are only 6% of the 1.3 million that the federal government projected California would enroll through 2014. And the web site in California appears to be working acceptably.

Perhaps the news on the number of enrollees is equivocal. It’s better than other states, and it’s still early, but, relative to the projections on which the ACA was premised, it is not good at all. There is also, however, what appears to me to be distinctly troubling news coming from California. We have another report on the age distribution of enrollees: so far, it is disproportionately old. And this is true in the state in which enrollment has progressed the furthest and in the nation’s most populous state. So, the data is potentially significant not just as an augury of what may be seen in other states but because a disproportionately elderly population in the largest state is, in an of itself, a problem.

Although persons age 55 through 64 constitute about 18% of the California population aged 18 through 64, they constitute double that, 36%, of persons in that same age segment who have enrolled for a plan. Similarly, although persons age 45 through 64 constitute about 41% of the California population, they constitute 59% of those who have enrolled thus far. As discussed earlier on this blog and elsewhere, because premium ratios between old and young are capped at 3 to 1, whereas actual claim ratios are likely to be higher, disproportionate enrollment of the elderly can help drive an adverse selection death cycle. This would be all the more true if the older people — it’s hard to call people age 55 “elderly”” — that are enrolling are disproportionately unhealthy relative to their age-group peers. Claims, therefore, by Covered California Director Peter Lee that “enrollment in key demographics like the so-called young invincibles is very encouraging” rest on theories of economics and statistics that I do not understand.

A Side Note on Market Concentration

By the way, who’s on the hook in the event the ultimate pool is distinctly more expensive than insurers anticipated? It’s the usual suspects. The big “winners” in California thus far are the usual suspects: Anthem Blue Cross has 28.1%, Kaiser Permanente, a California fixture, has 26.8%, Blue Shield of California has 25.6% and Health Net (with headquarters in Southern California) has 15.7%. Together, these four have 96% of the market with a “Herfindahl Index” of a moderately concentrated 2410. Dreams, therefore, of new competitors entering the marketplace, thus far seem illusory. But it is these “winners” that stand to lose the most money — and be the greatest recipient of federal redistributions under Transitional Reinsurance, Risk Corridors and Risk Adjustments — in the coming year if the trends hold up.

Exploring the likely implosion of the Affordable Care Act