Those optimistic about the success of the Affordable Care Act have been noting over the past several months that the premiums offered by insurers have been lower than those earlier forecast. But if one looks carefully at the original rhetoric, the comparison tends to be between some of the lowest premiums offered within a jurisdiction and those originally forecast. And this metric, according to ACA proponents, is appropriate because they expect consumers to focus purchases on the lowest cost policies.

But what if the lowest premiums are lower than expected not because the mix of purchasers is thought to be fine or because of cost cutting measures enabled by the ACA, but simply because all this metric exposes is the work of the insurers who priced their policies below actual risk? The “winner’s curse” is the term economists and game theorists give to situations in which, in an atmosphere of uncertainty, people bid on an item in an auction environment. What will often happen is that the “winning” bidder will tend to be one that loses money.

It is quite possible that all we are seeing with “low” ACA pricing, as measured by ACA proponents, is “the winner’s curse” in action. We may well be looking at insurers who (a) got it wrong or (b) thought the government would most greatly subsidize their losses or (c) for strategic reasons, decided to sell a “loss leader” in the first year or so of the ACA in order to lock consumers into their networks and their doctors with the idea that they could substantially raise premiums in the future. If this hypothesis is correct, individual policies under the Exchange are a lot less stable than many ACA proponents are asserting.

To summarize the results of the computations shown below, if the mean premium charged by insurers selling a type of policy (Silver HMO Plans, for example ) in a given geographic region (Harris County, Texas, for example) reflects the true risk posed by ACA policy purchasers, about 20% of the low bidders — the ones that I suspect will get a disproportionate share of the business — stand to lose at least 20% on their policies before the Risk Corridor program bails them out.

The big story as the ACA unfolds may be that some insurers — the ones who ended up with the business — simply made an error of exuberance in a new market and priced their policies too low. While these insurers will, thanks to a federal subsidization program for losing insurers called Risk Corridors, not entirely lose their shirts in the first year of the program as a result, they do stand to lose a lot of money that they will likely want to make up in any subsequent years of the Affordable Care Act.

New data analysis finds significant dispersion in plan premiums

This post will contribute some new data analysis that suggests the likelihood of the winner’s curse materializing as well as the magnitude of such a curse. Basically, I have sucked into my computer official government data on the 78,000 plans sold on the federal marketplace and done a lot of number crunching. The data shows a significant dispersion of prices offered by insurers for plans in the same geographic area, of the same metal tier and offering the same form of coverage (PPO, POS, HMO, or EPO) . While this dispersion does not prove that the low prices are outliers reflecting either miscalculation by some insurers or only-temporary use of low prices, it does suggest a significant possibility that such is the case.

Let’s take an example. Here are the prices offered where I live, Harris County, Texas — mostly Houston — for an HMO Silver Policy to a couple with two kids. The couple has an average age of 50 years old. We’ll call this hypothetical family “The Chandlers,” as a matter of convenience. The graphic shows the dispersion of premiums normalized so that the lowest price for a given policy is given a value of 1.

As one can see, for the Harris County, Texas policies shown here, although there are three policies that have premiums fairly close to the minimum, there are, however, two policies that have premiums more than 30% more than the minimum. If the mean premium estimated by insurers is “correct,” the insurer selling a Silver HMO policy at the lowest price will lose about 17%. The implication, if the Harris County plan is representative and if the mean premium is closer to the true risk than the low premium, is that the insurers most likely to win business due to low prices are likely to lose a considerable amount of money.

There are several potential rejoinders to the suggested implication of the graphic. Let me address each of them in turn.

Might Harris County, Texas be unusual?

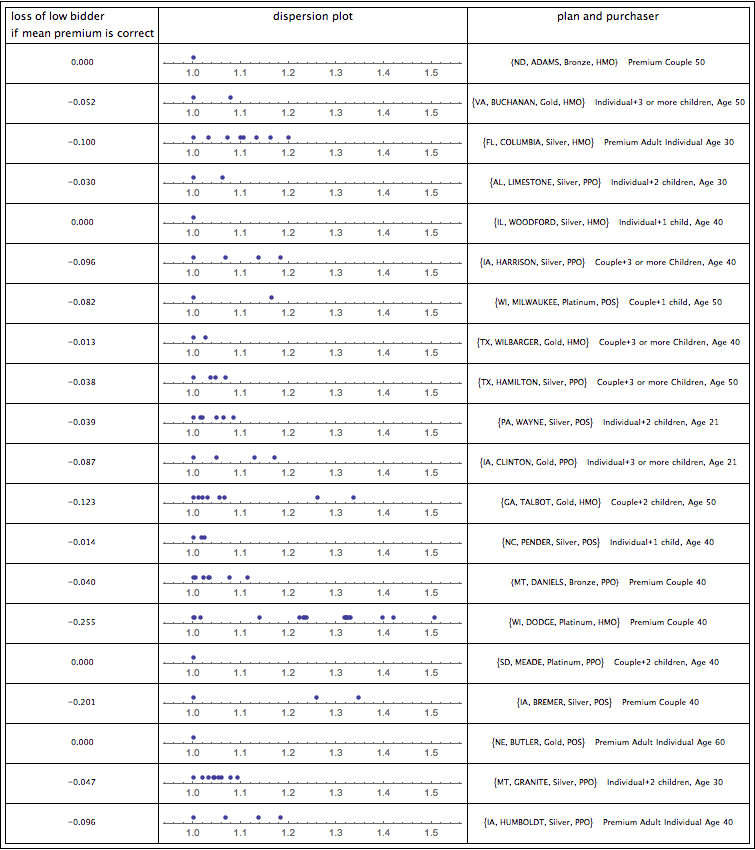

One response is that the example for Harris County, Texas Chandlers is unrepresentative. Houston, for example, has some very fancy hospitals and some not so fancy hospitals; so maybe premium dispersion for Harris County simply reflects whether one has access to the fancier hospitals (and the doctors who have admitting privileges to them). I have considered this possibility and find that, actually, the example I provide is pretty representative. Here, for example, are 20 randomly selected examples. For each plan, I show the amount the low bidder would lose if the average premium is “correct,” the dispersion of premiums, and the plan and purchaser randomly chosen. Of the ones in which there are any significant number of policies available, most of the premiums show a dispersion pattern qualitatively similar to that in Harris County for The Chandlers. Indeed, some of the random examples show dispersion considerably greater than that for the Harris County silver HMO policies. Except where there is little competition for plans and the low bidder is thus selling at the average price, the result presented above does not look like a fluke.

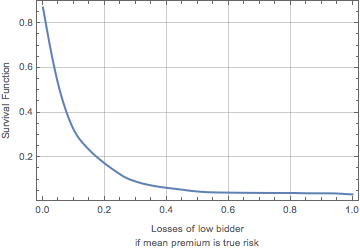

I can double check this result by computing for 5,000 random combinations of plans and purchasers the losses of the low bidder if the true risk was equal to the mean premium charged for policies and purchasers of that type. The graphic below shows the “survival function” (or “exceedance curve”) for the resulting distribution of these losses. The value on the y-axis is the probability that the losses will exceed the value on the x-axis. The results shown below confirm that the situation for Harris County Silver HMO plans sold to The Chandlers is not all that unusual. As one can see, losses of more than 10% take place more than 30% of the time and losses of more than 20% take place about 17% of the time. A rather scary picture.

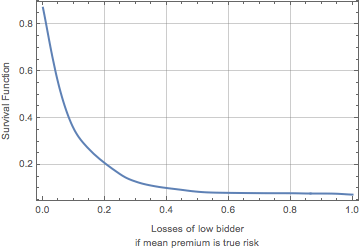

In fact, however, the situation may be even worse than depicted in the graphic above. Sometimes the losses computed by this method are low because the low bidder is also the only bidder. If we consider situations in which there is more than one bidder, here is the resulting survival function (exceedance curve) of the distribution. As one can see in the graphic below, the distribution of risks is shifted slightly to the right. Now 40% of the low bidders stand to lose at least 10% and about 21% stand to lose at least 20%.

Maybe the higher priced policies are better?

Another potential explanation for price dispersion is that, even if the policies are priced differently, that does not mean that the cheapest policies are selling for too low a price. All Silver HMO policies sold in Harris County, Texas to The Chandlers may not be the same. Some may have different deductibles or different networks.

The first response to this rejoinder is that the actuarial value of the policy — the relationship between expected payments by the insurer and premiums — should be about the same for each metal tier of policies. Silver policies should all have actuarial values, for example, of 70%. So it should not be the case that one silver policy has cost sharing different than the cost sharing of another silver policy in a way that would affect the premium charged for the policy. Moreover, the calculations underlying this post keep HMOs, PPOs, POS plans and EPOs apart; so it should not be the case that observed premiums differ because, perhaps, the cheaper plans are HMOs whereas the more expensive ones are PPOs.

Of course, cost sharing is not the only way in which policies within a given location, of the same metal tier and sold to the same purchaser could vary. One policy might offer richer benefits than another. It could have a richer network with more doctors available or more prestigious and expensive hospitals inside the network. Could that be responsible for a substantial part of the premium dispersion we see? It’s impossible to tell for sure — the data published by HHS does not attempt to quantify the richness of the network being offered. I do find it difficult to believe, however, that such differences are responsible for the entirety of differences in excess of 20% between the low bidder and the mean bid, or, for that matter, differences in excess of 40% that sometimes occur between the low bidder and the higher bidders.

Maybe the average premium is meaningless; the low bidder got it right

Of all the potential rejoinders I have considered, the one now forthcoming is the one that is most troubling. There is nothing the data standing by itself can tell us whether most of the insurers have it right and the low insurers are about to lose their shirts or whether the low insurers have been more insightful or have managed to keep costs down such that they will break even (or even make money) selling their policies at low premiums. And, yet, I am doubtful. One can view the mean or median of the premiums as an “ensemble model” of the true cost of providing care under the Affordable Care Act. And there is research (examples here, here and here) suggesting that ensemble models predict better in many open-textured situations than individual models. So, while it’s possible, I suppose, that in every jurisdiction the low bidder is predicting more accurately than the group of insurance companies as a whole, such a result would be surprising. A far simpler explanation is that the low bidder — the one who is likely to win business from price sensitive insureds — is succumbing to “the winner’s curse.”

Maybe the disaggregation of plans is misleading

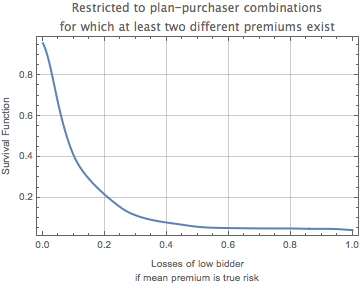

This is a very technical objection, but consider carefully what I have done. I have looked at all policies of a given metal tier and a given plan type in a given geographic location sold to a certain family type such as “all silver policies in Harris County, Texas, sold to The Chandlers.” But, really, plans are sold not to just to The Chandlers but to all family types. So, it could conceivably be that while the plans sold to the family type I am looking at are highly dispersed, the average premiums over all family types (weighted by prevalence of the family type) are far less dispersed. This strikes me as unlikely — why would an insurer be overcharging one family type relative to another — but you can not rule it out a priori. Maybe — just maybe — the dispersion we are observing is not real; it is just an artifact of my disaggregation of the data.

I would, of course, love to aggregate the data and see if the high degree of dispersion persists. The difficulty with this cure comes with the problem of weighting the data. We don’t know the distribution of policies sold among family types. We don’t know, for example, whether The Chandlers constitute 2% of policies sold or 5% of policies sold. So, I can’t perform a perfect aggregation of the data. One way to get a feel for the objection, however, is to simply take an unweighted average of the premiums for all the family types identified in the database and aggregate it that way. This is far from perfect, and we could spend a lot of time refining it, but it should provide a clue as to whether the disaggregation of plans is significantly responsible for the high degree of observed dispersion.

The graphic below shows the exceedance curve for losses of the low bidder assuming the mean premium is the true risk based on an unweighted average of family types purchasing the policies. One can see that 20% of the low bidders will lose at least 20% if it turns out that the mean premium charged for similar policies reflected the true risk. Upwards of 35% will lose more than 10%. A quick comparison of this curve with those above shows that it is essentially the same. There is nothing that I can see suggesting that the fundamental result shown in this blog entry — high dispersion of premiums among what should be similar policies and the potential for significant losses by low bidders — is an artifact of the methodology I have employed.

Conclusion

In the end, even the extensive data that the government is put out is insufficient to determine definitively whether the lower priced insurers in the individual Exchanges are about to lose money. There are more optimistic interpretations of the observed premium dispersions: maybe it is the low bidders who are “getting it right” or maybe the low bidders have just found ways to keep costs down through better negotiating or cheaper care networks. But if these optimistic explanations prove insufficient, what this post shows is that while some insurers will likely do just fine there are a substantial minority of insurers who are about to get bitten by the “winner’s curse” and get a large volume of purchasers for whom the premiums charged will be insufficient to defray the expenses incurred.

Technical Notes

The data used here was taken directly from the United States Department of Health and Human Services. It was analyzed using Mathematica software, which was also used to produce the graphics shown here.