I’ve written before that net premium increases for many individuals purchasing policies under the ACA will be higher than gross premium increases. I’ve gotten some emails expressing puzzlement over this conclusion. So, in this post I want to explain in some detail why this is the case.

An example

Consider five Silver policies on an Exchange. In 2015, here is a table showing their gross premiums

1. $4,161.55

2. $3,881.27

3. $4,338.10

4. $4019.11

5. $3550.64

So, the second lowest silver policy is Policy 2, which has a premium of $3,881.27. Suppose our individual can contribute $1,000 per year based on their income. If they had purchased policy 2 their tax credit would have been $2,881.27 and their net premium would have been $1,000. If our individual purchases policy 4, however, which has a gross premium of $4,019.11, their tax credit is still $2,881.27, so they will end up having a net premium of $1,137.84

Now, suppose the gross premium increases average about 6.33% but are distributed as follows among our 5 insurers.

1. 11.38%

2. -2.57%

3. 7.26%

4. 10.28%

5. 5.29%

The new gross premiums for 2016 are thus as follows:

1. $4,634.99

2. $3,781.70

3. $4,652.87

4. $4,432.30

5. $3,738.41

The new second lowest premium is Policy 2, which has a gross premium of $3,781.70. Suppose now our individual has essentially the same income such that the amount they are deemed to be able to contribute is still $1,000. This means the 2016 tax credit is $2,781.70. What if our individual wants to keep his health plan and stick with Policy 4. Maybe our individual likes the practitioners in the Policy 4 network. The new difference between the new gross premium for Policy 4 ($4,432.30) and the tax credit of $2,781.70 is $1,650.60.

Thus, although the gross premium for the policy has gone up 10.28% (bad enough) the net premium has gone up 45.06%.

So, did I concoct some bizarre set of numbers so that the ACA would look bad? I did not. The result you are seeing is baked into the ACA.

An experiment

Let’s run the following experiment. Suppose premiums are normally distributed around $4,000 with a standard deviation of $500. And suppose the gross premium increase is uncorrelated with premiums and is normally distributed around 5% with a standard deviation of 5%. Assume there are five policies at issue. We can then calculate for each of the five policies, the gross premium increase and the net premium increase in the same way we did in the example above. We run this experiment 100 times.

The graphic below shows the results. The horizontal x-axis shows the size of the gross premium increase (in fractions, not percent). And the vertical y-axis shows the size of the net premium increase. The dotted line shows scenarios in which the gross premium increase is the same as the net premium increase. What we can see is that for the larger gross premium increases, the net premium increases tends to be larger than the gross premium increases and for the smaller gross premium increases (or for gross premium decreases), the net premium increase tends to be smaller than the gross premium increase. Thus, about half the population will experience net premium increases larger — and sometimes way larger — than they might think from reading the news.

Is this result an artifact of, say, having our policyholder being deemed by the government to be able to contribute $1,000 based on their income? Not really. The graphic below runs the same experiment but this time assumes our individual is poorer and is thus deemed able to contribute only $500.

What we can see from the graphic is that the result is even more dramatic. The poor will see drastic divergences between gross premium increases and net premium increases. Many, for example who have gross premium increases of say just 5% experience net premium increases of over 30%.

And what of the less subsidized purchasers, those who, for example, are deemed able to contribute $3,000 towards a policy? The graphic below shows the result.

Now we can see that the gross premium increases and net premium increases are clustered pretty tightly together. Indeed, for the wealthier purchasers, net premium increases more often than not are smaller than gross premium increases. However, since most purchasers of Exchange policies tend to be those receiving large subsidies, the graphic above is not representative of the situation for most purchasers.

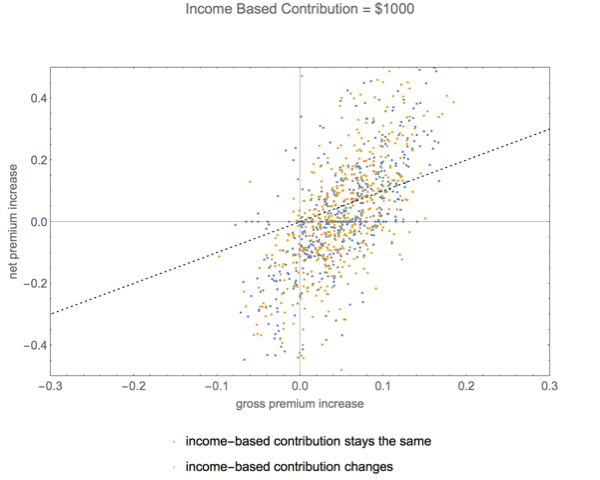

Did I rig the result by assuming that the income-based contribution stayed the same. No. Here’s a graphic showing gross versus net premiums first, under the assumption that income-based contributions remain the same and second, under the assumption that income-based contributions wander, sometimes going up, sometimes going down.

What you can see is there is not much difference between the yellow points — income based contribution remains the same — and the blue points — income based contribution wanders.

And, although I won’t lengthen this post with yet more graphics, the basic result generalizes to situations in which there are more than 5 Silver policies. The pattern is the same.

Conclusion

It really is true. Net premium increases will often be larger than gross premium increases, particularly for the poor. The sticker shock some received on seeing the gross premium increase figures recently released at healthcare.gov will, in many instances, be little compared to the knockout blow that will occur when people start computing their new net premiums.