As discussed yesterday on this blog and elsewhere in the media, Cover California, the state entity organizing enrollment there, has released data showing the age distribution of the group thus far enrolling in plans on its Exchanges. Although I took a rather cautionary tone about the age distribution — fearing it could stimulate adverse selection — the head of Cover California and some influential media outlets generally favorable to the Affordable Care Act have been considerably more cheerful. So, who’s right? For reasons I will now show — and probably to no one’s surprise — me. (More or less).

To do this, we need to do some math. It’s a more sophisticated variant of the back of the envelope computation I undertook earlier on this blog. The idea is to compute the mean profit of insurers in the Exchange as a function of the predicted versus the actual age distribution of the pool they insure. Conceptually, that’s not too difficult. Here are the steps.

1. Compute the premium that equilibrates the “expectation” of premiums and costs for the predicted age distribution of the pool they insure. Call that the “predicted equilibrating premium.”

2. Compute the expected profit of the insurer given the predicted equilibrating premium and the actual age distribution of the pool they insure.

3. Do Step 1 and Step 2 for a whole bunch (that’s the technical term) of combinations of predicted age distributions and actual age distributions.

Moving from concept to real numbers is not so easy. The challenge comes in getting reasonable data and, since there are an infinite number of age distributions and in developing a sensible parameterization of some subset of plausible distributions.

The Data

The data is interesting in and of itself. To get the relationship between premiums and age, I used the robust Kaiser Calculator. Since healthcare.gov itself recommends the web site (their own site seems to have a few problems) and I have personally validated its projected premiums for various groups against what I actually see from various vendors, I believe it is about as reliable a source of data as one is likely to find anywhere right now. So, by hitting the Kaiser Calculator with a few test cases and doing a linear model fit using Mathematica (or any other decent statistics package), we are able to find a mathematical function that well captures a (quadratic) relationship between age and premium. (The relationship isn’t “really” quadratic, but quadratics are easy to work with and fit the data very well.) The graphic below shows the result.

Nationwide average health insurance premium for a silver plan as a function of age

We can normalize the graphic and the relationship such that the premium at age 18 (the lowest age I consider) is 1 and everything else is expressed as a ratio of the premium at age 18. Here’s the new graphic. The vertical axis is now just expressed in ratios.

Nationwide average health insurance premium ratio for a silver plan as a function of age

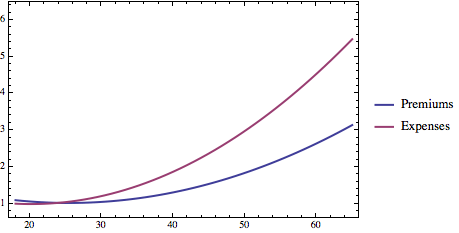

To get the relationship between cost and age, I used a peer reviewed report from Health Services Research titled “The Lifetime Distribution of Health Care Costs.” It’s from 2004 but that should not matter much: although the absolute numbers have clearly escalated since that time, there is no reason to think that the age distribution has moved much. I can likewise do a linear model fit and find a quadratic function that fits well (R^2 = 0.982). Again, I can normalize the function so that its value at age 18 is 1 and everything else is expressed as a ratio of the average costs incurred by someone at age 18. Here’s a graphic showing the both the relationship between age and normalized premiums in the Exchanges under the Affordable Care Act and normalized costs.

The key thing to see is that health care claims escalate at a faster rate than health care premiums. Others have noted this point as well. They do so because the Affordable Care Act (42 U.S.C. § 300gg(a)(1)(A)(iii)) prohibits insurers from charging the oldest people in the Exchanges more than 3 times what they charge the youngest people. Reality, however, is under no such constraint.

Parameterizing the Age Distribution

There are an infinite number of potential age distributions for people purchasing health insurance. I can’t test all of them and I certainly can make a graph that shows profit as a function of every possible combination of two infinite possibilities. But, what I can do — and rather cleverly, if I say so myself — is to “triangulate” a distribution by saying how close it is to the age distribution of California as a whole and how close it is to the age distribution of those currently in the California Exchange pool. I’ll say a distribution has a “Pool Parameter Value” of 0 if it comes purely from California as a whole and has value of 1 if it comes purely from the California Exchange pool. A value of 0.4 means the distribution comes 40% from California as a whole and 60% from the current California Exchange pool. The animation below shows how the cumulative age distribution varies as the Pool Parameter Value changes.

How the age distribution varies as the pool goes from looking more like California as a whole to looking more like the current pool as a whole.

Equilibration and Results

The last step is to compute a function showing the equilibrium premium as a function of the predicted pool parameter value. We can then use this equilibrating premium to compute and graph profit as a function of both predicted pool parameter value and actual pool parameter value.

The figure below shows some of the Mathematica code used to accomplish this task.

Mathematica code used to produce graphic showing relationship between insurer profit in the California exchanges and the nature of the predicted pool and the actual pool

Stare at the graphic at the bottom. What it shows is that if, for example, California insurers based their premiums on the pool having a “parameter value” of 0 (looks like California) and the actual pool ends up having a “parameter value of 1 (looks like the current pool), they will, everything else being equal, lose something like 10% on their policies and probably need to raise rates by about 10% the following year. If, on the other hand, they thought the pool would have a parameter value of 0.5 and it ended up having a parameter value of 0.75 the insurers might lose only about 3.5%.

Bottom Line

If I were an insurer in California I’d be concerned about the age numbers coming in, but not panicked. First, I hope I did not assume that my pool of insureds would look like California as a whole. I had to assume some degree of adverse selection. But it does not look as though, even if I made a fairly substantial error, the losses will be that huge. That’s true without the Risk Corridors subsidies and it is all the more true with Risk Corridor subsidies.

What I would be losing sleep about, however, is that the pool I am getting is composed disproportionately of the sick of all ages. If I underestimated that adverse selection problem, I could be in deep problem. My profound discomfort would arise because, while I get to charge the aged somewhat more, I don’t get to charge the sick anymore. And there’s one fact that would be troubling me. Section 1101 of the Affordable Care Act established this thing calledthe Pre-Existing Condition Insurance Pool. It’s been in existence (losing boatloads of money) for the past three years. It held people who couldn’t get insurance because they had pre-existing conditions. They proved very expensive to insure. There are 16,000 Californians enrolled in that pool. But that pool ends on January 1, 2014. And the people in it have to be pretty motivated to get healthy insurance. Where are they going to go? If the answer is that a good chunk of the 79,000 people now enrolled in the California pool are former members of the PCIP, the insurers are in trouble unless they get a lot more healthy insureds to offset these individuals.

The Affordable Care Act does not establish a uniform national pool for persons purchasing Bronze, Silver, Gold and Platinum policies on the Exchanges. Rather, it creates at least one such pool for each of the states involved in the program . And that is true even if multiple states use the same “Exchange” — the one in Washington D.C. — to establish coverage.

This fracturing of the pool and of the administrative apparatus creates an architectural problem: what happens if, as may well be the case, insurers in the Exchanges muddle through in a few states but suffer massive losses in many others? Most likely, insurers in the problem states will exit from the Exchanges or require significant premium hikes on top of rates that already give many potential customers sticker shock. But this reaction by profit-motivated insurance companies could lead more Americans to complain that imposition of a uniform individual mandate tax under 26 U.S.C. § 5000A throughout the nation is unfair. And, if the increases are large enough and a large enough number of people stick with the Exchanges — because they don’t see another choice — this could increase the cost of premium subsidies to the federal government and its taxpayers beyond the substantial numbers already projected.

The key point I want to make here is that even the best and brightest people often fall into the trap of thinking that the Affordable Care Act Exchange-based system for reducing the number of uninsureds will either succeed or fail. Either the system will fall into an adverse selection death spiral or it will not. Perhaps that is the case. But this binary thinking probably is not right. It’s kind of like quantum physics: the Exchanges could both succeed and fail at the same time. It just depends what state you’re in. (Physics pun intended).

Here’s how. Although it is too early to tell for sure — and the persistent failure of healthcare.gov and many of the state exchange sites such as Maryland and Oregon hinders augury — it looks as though the Affordable Care Act is having somewhat more success in some states than others. Proponents of the ACA like to point to California experience where it is claimed that 70,000 people have made it through at least some more advanced state of the enrollment process. The gloomy point to Oregon where apparently no one has successfully enrolled or Texas, which, despite having the largest number of uninsureds, had only 2,991 enrolled in a plan last time anyone counted. (Here’s the handy chart in the Washington Post.) Both the optimistic and pessimistic point to Kentucky where the number of enrollees is proportionately higher than in many states but in which the population of insureds seems disproportionately old.

So, in a few months it could be that Exchange insurance in some states such as California where the technology has worked better and the political environment is more sympathetic to the ACA is able to persist into 2015 without major rate hikes or insurer withdrawals. In those states, there remains some considerable logic to imposing a tax of what will be 2% of household income or roughly $325 per household member (kids count as half) for failure to buy health insurance. But what might we do in states such as Texas or Mississippi or West Virginia or perhaps many others where the insurers experience severe adverse selection that even Risk Corridors (42 U.S.C. § 18062) is unable to cure adequately? If the result is, as one would expect, a reduction in the number of insurers continuing to participate in the Exchange and an increase in rates, the Affordable Care Act is likely to become even less popular in those jurisdictions. This would be all the more true for those people — a small group, but still people nonetheless — whose income is such that the rates remain less than the 8% of household income level that would otherwise excuse them under 26 U.S.C. § 5000A(e)(1) from having to buy the expensive policies.

Fixing such a problem will be extraordinarily difficult. If Congress remains in gridlock with some finding the ACA so abhorrent that reform of even its worst excesses is unacceptable and others divided on the merits of any particular reform, Congress will have little ability to address the genuine problems of those in the failure states. And would Congress be willing to write a statute that excused people in some states from paying an individual mandate tax while insisting that it continue in others? What criterion would be used to distinguish the tax paying from the tax exempt states? If Congress tries, expect some heavy duty litigation on the constitutionality of such a non-uniform tax: “all Duties, Imposts and Excises shall be uniform throughout the United States.” (U.S. Constitution, Article I, Section 8, clause 1). Would Congress be willing to adjust “Risk Corridors” or “Risk Adjustment” (section 1343 of the ACA) to give special preference to insurers in states whose Exchanges have effectively failed? If Congress can not relieve the difficulties of the death spiral states, expect pressure to grow yet further for repeal of the entire law.

Again, we are left with a design problem in the Affordable Care Act. Blinded by the dream of reducing the number of uninsureds and providing healthcare to a broader segment of American society, it creates a system in which, conceivably, under just the right circumstances it might work, but in which even small departures from desired assumptions risk plunging that system into a “basin of attraction” aptly known as “the death spiral.” We end up torn asunder in a black hole of insurance market failure from which there is no escape. Worse, it is constructed in a way such that state-by-state adjustments, even with a less dysfunctional Congress, will prove difficult indeed.

According to a news report from Reuters, which is being picked up widely, early figures from four states are suggesting that the pool of insureds enrolling in the Exchanges is older than anticipated. If this situation persists and is not an artifact of either the particular states involved or simply the urgency with which older people applied, it further threatens the ability of the Affordable Care Act to sustain its plan of equalizing opportunity to acquire health insurance. This is so because, although older people do pay more in the Exchanges established by the Affordable Care Act, they pay less than would be actuarially appropriate. Young people, by contrast, pay more.

Here’s the key passage from the Reuter’s report.

The Obama administration is aiming to enroll about 2.7 million 18- to 35-year-olds in the exchanges by the end of March, out of 7 million total, or about 38 percent.

Early data from Connecticut, Kentucky, Washington and Maryland show that so far more than 20 percent of the 23,500 combined enrollees in private insurance plans are 18 to 34 years old, ranging from about 19 percent in Kentucky and Connecticut to about 27 percent in Maryland. About 36 percent of enrollees across the four states are 55 to 64. Additional demographic data is expected from California on Thursday.

A back of the envelope computation shows that this situation could result in additional losses of about 10% by insurers before risk adjustment payments are taken into account. And this is true even if each age group in the pool is as healthy as anticipated. The insurer losses resulting from disproportionate enrollment of older insureds has several important consequences: (1) insurers may decide to exit the pool in the future; (2) insurers may decide to raise premiums to adjust to the real pool as opposed to the projected pool; and (3) the government is going to pay more in Risk Corridor payments than anticipated.

Relationship between “true ratio”, percent young in the pool, and Exchange insurer profitability

The graphic above attempts to explain the issue. The x-axis shows the “true ratio” of expected medical claims to be paid between the oldest people in the pool and the expected medical claims to be paid of the youngest people in the pool. No one knows this figure for sure, but it could well be about 5 to 1. (This is why the Affordable Care Act is forced to hold premiums to a 3 to 1 ratio; otherwise premiums for the older group would be extremely high.) The y-axis shows the percentage of people entering the Exchange pools who are between 18 and 35. As the Reuters story indicates, it was hoped this group would comprise 38% of the pool. The green dot shows the result that might be hoped for if the young (18-35) indeed constitute 38% of the pool and the true ratio of claims paid between oldest and youngest is 5 to 1. At this level, insurers neither make unusual profits nor suffer unusual losses. The blue dot shows the result that might be seen if the young end up constituting — as the Reuters says the early evidence shows — about 20% of the pool. As one can see the red dot produces losses that are close to 10% of the risk assumed by insurers.

I’m placing a Mathematica notebook on Dropbox showing the computation. The idea, is that one finds a linear relationship between age and premium relationship that just covers claims payments for any value of the true ratio but subject to the constraint that the premium the oldest person pays can not be more than three times bigger than the premium the youngest person pays and under the assumption that those under age 35 constitute 38% of the pool. One then determines profits for any combination of true ratio and percentage of the pool under age 35. The process takes a little algebra (mostly rescaling operations), some calculus (finding “expectations” of distributions) and some visualization.

Notes

1. Although I modeled it that way, I am fully aware that the relationship between age and claims is non-linear. It’s probably more cubic. I’m also fully aware the relationship between age and premiums tends not to be linear under the Affordable Care Act. You can use the wonderful Kaiser Calculator or go to the fabulous Health Sherpa website to see that. And I’m also aware that using a uniform distribution to model the distribution of ages within the 18-35 group and the 35-64 group is imperfect. Still, for purposes of getting just some rapid order of magnitude estimates to guard against those who would dismiss the problem or wildly exaggerate it, I believe the linear assumption is supportable. It keeps things simple in a situation in which one has to be very careful about false assertions of precision and in which predictions are often hideously wrong.

2. As mentioned earlier, if the disproportionate enrollment of the elderly does not persist, as supporters of the ACA hope, the problem identified in this entry is reduced. Other problems, such as disproportionate enrollment of the unhealthy — which is a far more significant issue — may persist. But we don’t have data at present on the health of those enrolling. It is troublesome, however, that most of the time proponents of the ACA trot out someone who has actually enrolled in the Exchanges (or is a Jessica Sanford who thought they would), it is someone who has higher-than-average medical expenses. I wish they would more frequently show off someone who is healthy now but just wants protection against the possibility of an adverse health event.

In a Wall Street Journal op-ed today that tracks much of what has been said on this blog in recent years, Florida Senator Marco Rubio announced that he will introduce later today a bill (provisionally numbered S.1726 ) that would apparently eliminate “Risk Corridors,” the provision of the Affordable Care Act under which the government would reimburse insurers selling insurance on an Exchange for the next three years from a good portion of any losses that they suffer there. Rubio contends that “ObamaCare’s risk corridors are designed in such an open-ended manner that the president’s action now exposes taxpayers to a bailout of the health-insurance industry if and when the law fails.”

Marco Rubio

Senator Rubio is largely correct, I believe, in his understanding of Risk Corridors (section 1342 of the ACA, codified at 42 U.S.C. 18062) both as drafted in the statute and as implemented by the Department of Health and Human Services. Unlike its cousins, the reinsurance provisions (42 U.S.C. § 18061) and the risk adjustment provisions (42 U.S.C. § 18063), both of which likewise help reduce the risks of writing policies for sale on an Exchange, Risk Corridors is not drafted to be budget neutral. That was the way the Congressional Budget Office scored it — it assumed that receipts under the provision would equal outlays — but this was clearly a blunder that should have been apparent at the time and that minimized the advertised budgetary risk entailed by passage of the Affordable Care Act. As discussed in an earlier blog post, if the distribution of profit and loss by insurers selling in the Exchanges is skewed in the loss direction, the government will be obligated to pay out more than it takes in. Where the funding for this new “entitlement” for the insurance industry would come from is unclear. Senator Rubio is thus correct again when he says that the bill will be paid for by the taxpayer.

Senator Rubio is not correct to imply, however, that, standing by itself, the underestimate of Risk Corridor exposure represents this enormous understatement of the cost to the taxpayer of the Affordable Care Act. That law, for better or worse, always called for large taxpayer outlays to help prop up an insurance system that, as one of its critical architectural features, would attack medical underwriting by insurers. Indeed, although it was not apparent to many until recently, precisely because of the Three Rs of Risk Corridors, “free” reinsurance and future “risk adjustments,” the Affordable Care Act always created this scheme that looked like it preserved private insurance but in fact converted insurers largely into claims processors in a system in which profitability and core insurance functions were largely controlled by the federal government.

To see the relative magnitude of the Risk Corridors program, consider the bigger picture. The CBO projected most recently, for example, that subsidies to help individuals purchase insurance via tax credits and cost sharing reductions would total $26 billion in 2014 and ramp up to $108 billion by 2017. To be sure, that figure was based on the assumption, which is beginning to look very suspect, that there would be 7 million people in the Exchanges in 2014, and thus might decrease if enrollment is considerably lower. Still, since by my calculations it seems unlikely that the Risk Corridor payments will amount to more than $1 billion per year (but see footnote below), it is not as if the cost of “Obamacare” suddenly went through the roof. Maybe Risk Corridors could be considered the “straw that broke the camel’s back,” but the Affordable Care Act has always been a stretch of the federal budget and it has been a stretch that many have long found deeply troubling.

CBO projections on the cost of the Exchanges

The more serious issue surrounding Senator Rubio’s suggestion that Risk Corridors be repealed is that such an action might well be the straw that broke the insurers’ backs. Insurers do not have to participate in the Exchanges and they certainly do not have to continue to do so in 2015. I suspect that if, anything stands right now or in the future between the deeply troubling enrollment numbers and an adverse selection death spiral caused by a combination of premium escalation and insurer withdrawals from the exchange marketplace, it is insurers’ belief that Uncle Sam will take care of the insurance industry. Indeed, that’s the not-too-subtle consolatory hint that accompanied the letter sent last week by the Obama administration to state insurance commissioners. It tells regulators and insurers that, to enable the President to keep his oft-repeated campaign promise — I don’t even have to tell you which one — the healthy insureds on which Exchange insurers were banking would now be given a sometimes cheaper (and sometimes competitive) alternative. How many of these victims of the previously broken promise would have purchased insurance on the Exchanges if forced to do so is open to question. But, at the present time, every insured helps those Exchanges survive, even if only barely.

By telling insurers that, contrary to the strong hints at the end of the Obama administration letter, there will be no relief for the additional average costs now imposed on insurers, passage of Senator Rubio’s bill might lead to the implosion of the insurance Exchanges and the death of a crucial portion of the Affordable Care Act. While such a result would hardly deter many from voting in favor of the bill, those who dislike the Affordable Care Act ought to think hard not just about how much they want it to end but in what way they want it to end. Dismantling the ACA is itself going to be difficult and painful — wait until we hear the cries from the people who deeply craved the subsidized insurance they thought they were receiving or who otherwise benefited from the Act — and ultimately entails very serious and difficult policy choices about how we want to finance healthcare in the United States. Consumer driven? Single payor? If the law is to be unwound, it would be better if it were done in as deliberate and orderly way as practicable rather than as an unforeseen result of legislation that purported to deal with a narrow aspect of the ACA.

There is, it should be noted, a compromise position that will preserve something of Risk Corridors while not adding to the federal budget deficit. One could amend the Risk Corridors provision to force it to be budget neutral. This has already been done in the companion provisions of stop-loss reinsurance and risk adjustment and there is no reason that, if legislators could act in good faith, the law could not be modified to state that payments by the Secretary of HHS to insurers would be reduced pro rata to the extent necessary to make payments in under Risk Corridors equal payments out. This potential reduction in payments might, it must be acknowledged, scare insurers and contribute to the implosion of Obamacare, but it would be less likely to do so that a bill that repealed Risk Corridors altogether.

A Footnote on the cost of Risk Corridors

Footnote: I’ve been thinking some more about a back of the envelope computations in a blog entry that attempted to develop a relationship between the number of people enrolling in insurance on the Exchanges and the size of the Risk Corridor payments. As those paying the closest attention to my prior blog post will recall, I made an assumption about the spread of the distribution of insurer profits and losses. The assumption was not unreasonable, but it was also hardly infallible. What if, I have been wondering, the spread was much narrower than I suggested it might be?

I decided to run the experiment again using a standard deviation of profits and losses only 1/10 of what it had been. I thus create regimes in which the financial fates of most insurers selling policies are closely tied together. What I find is that assuming that most insurers will either make money or that most insurers will lose money has a tendency to increase the payments the government will likely have to make if enrollment is small. In this new experiment, payments peak at about $1.5 billion rather than $1 billion in the prior experiment. Bottom line: the prior blog post was basically correct — we are dealing here with very rough estimates — but if all insurers are subject to similar economic forces the Risk Corridor moneys paid by the government might grow somewhat. Still, it is not as if the cost of Risk Corridors is suddenly going to dwarf the cost of premium subsidies and cost sharing reductions already required by the ACA.

Let us suppose, for the moment, that enrollment in the Exchanges increases as healthcare.gov becomes less dysfunctional and as we get closer to the January 1, 2014 and March 1, 2014 deadlines. It is, after all, unrealistic to think that enrollment will remain at the pathetic/paltry/miserable levels recounted by today’s testimony from Kathleen Sebelius, notwithstanding her counting of people who merely put a plan in their shopping cart. But it does seem likely to many , including me, that

sticker shock,

the small and difficult-to-enforce penalties for 2014,

President Obama’s decision to let insurers “uncancel” ungrandfatherable policies and let some of those insureds stay out the Exchanges,

will likewise lead the enrollment in the Exchanges to be considerably smaller than projected. This is particularly likely to remain true, I believe, in states such as Texas in which institutional forces and political culture often do not encourage participation and in which fewer than 3,000 out the estimated 3,000,000 eligible to do so have enrolled thus far.

The key question is how resilient are the Exchanges to low enrollments in which, one would expect, the enrollees are — even more than they were projected to be — disproportionately older and disproportionately less healthy. And have the Exchanges been rendered yet more fragile by what many cheered as the surprisingly low premiums charged by many insurers? Could those insurers, who are likely to swoop up most of the business in a price sensitive market, in fact be about to face the winners curse? The answer to these questions may lie deep in the details of one of the least studied and yet one of the most important set of provisions in the Affordable Care Act: the reinsurance and risk adjustment provisions contained in sections 1341-1343 of that Act and now codified at 42 U.S.C. §§ 18061-18063.

Here’s the (long) paragraph-length explanation of how these reinsurance and risk adjustment provisions work. 42 U.S.C. § 18061 basically creates a transitional (2014-16) government operated stop-loss reinsurance program funded out of a special tax on other health plans ($63 per covered life). The reinsurance attaches when a person covered by a plan in an Exchange incurs $60,000 or more in claims per year. After that point, the reinsurer pays for 80% of the claims up to a cap of $250,000. Thus, if an individual had claims of $180,000 in a year, the government would reimburse the insurer for $96,000, which is 80% of the difference between $180,000 and $60,000. What this provision appears to do is make insurer profit and loss less sensitive to attracting high claims insureds. 42 U.S.C. § 18062 basically redistributes money in a complex way from insurers whose Exchange plans profit to insurers whose Exchange plans lose money. Again, the idea is to reduce the insurer anxiety either that their plan and their marketing (if any) happens to attract an unhealthy pool or that they selected a premium too low for the actual risk that materializes. Finally, 42 U.S.C. § 18063, the only program that is supposed to persist past 2016, imagines an incredibly complex system in which the risk posed by an insurer’s pool is assessed and the states or, in their default, the federal government (see 42 U.S.C. 18041(c)(1)(B)(ii)(II)), transfers at least some money from those with the riskiest pools to those with the least.

Will these provisions really rescue the insurers?

All of this might seem a comfort to insurers that might permit them to survive and continue in the Exchanges even if the pools are, on average, considerably more expensive than originally projected. But to get a better handle on the degree of solace these provisions might provide, we need to look at some of the limitations of these programs and the actual numbers.

Stop-loss reinsurance under 42 U.S.C. § 18061

First, let’s look at how much risk the transitional reinsurance provided by 42 U.S.C. § 18061 really slurps up. What I contend is that while this provision should — and probably did — lower the premiums the insurer would otherwise need to charge to avoid losing money, it does less to rescue insurers if the pool is less healthy than they foresaw. While to really see this, we need to get deep into the weeds and do some math, I’m going to hold off on that fun for now. We have to save some things, such as the Actuarial Value Calculator, for other blog entries. I believe I have developed a plain English explanation that gets us most of the way there.

The key concept is to recognize that sophisticated insurers (are there other kinds?) took the free reinsurance into account when they priced their policies. They computed an expected value of the reinsurance reimbursements and lowered their rates by something approximating that amount. They were able to charge lower rates than they otherwise would because some of the claims bill would be picked up by the government. But this does not mean that the insurers end up having profits that are insensitive to the actual claims incurred by their pool. Unless all of the higher-than-expected claims are stuffed into the zone in which the reinsurance kicks in ($60,000 to $250,000), the insurers will be hurt when the pool has higher claims than expected. But such an assumption is incredibly implausible. If the insurer assumed that only, say, 2% of its insureds would have claims between $20,000 and $25,000 but, as it turns out, 4% of its insureds have such claims, nothing in 42 U.S.C. § 18061 will help such an insurer with that unanticipated loss. Moreover, because the reinsurance even within the relevant zone is incomplete, the insurer will lose money if claims between $60,000 and $250,000 are higher than expected. The effect of the transitional stop-loss reinsurance on reducing the consequences of adverse selection is thus likely to be small.

In the end, what this transitional reinsurance mostly does is mostly to tax non-Exchange policies $63 per covered life in order to make policies within the Exchange more attractive to policyholders. And, yes, that fact should make Exchange-based policies cheaper and reduce the problem of adverse selection. After all, if the insurance were free presumably there would be little adverse selection — everyone would get it. But the reinsurance fails to reduce insurer vulnerability to adverse selection much more than, say, providing more generous tax credits and cost sharing reductions would have done. If the pool ends up being less healthy than the insurer anticipated — an almost certain consequence of lower-than-expected enrollments, 42 U.S.C. § 18061 is hardly going to end up relieving the insurer of most of the unhappy consequences of having written policies in that environment.

Footnote: There is one more wrinkle, but it only means that the transitional reinsurance is a yet weaker rescue vehicle: the government’s obligations under the transitional reinsurance provisions are limited. There’s “only” $12 billion in 2014 and this ramps down to $4 billion in 2015. If those amounts aren’t adequate to pay reinsurance claims, each claim gets reduced pro rata. The reason I relegate this point to a “footnote,” however, is that if the pools are really small then even if claims per person are way higher than expected, the aggregate amount of claims in the reinsured zone of $60,000 to $250,000 aren’t going to be that big. My back-of-the-envelope computation suggests that the $12 billion allocated for transitional reinsurance should not be insufficient unless at least 2 million people enroll on the exchanges; since right now we are almost certainly at less than 100,000, 2 million seems a lot of insureds away.

“Risk Corridors” under 42 U.S.C. § 18062

The biggie in this field is the “Risk Corridors” provisions contained in 42 U.S.C. § 18062. It essentially creates this massive transfer scheme, taking money from insurers who had profitable pools and giving it to those who did not. In some sense, it converts insurers from entities bearing risk to mere fronts for government funded health insurance. If I were prone to accuse the Affordable Care Act of creating “socialized medicine,” my Exhibit A would be the stealth “Risk Corridors” provision of 42 U.S.C. § 18062.

The graphic below shows how the scheme works. The x-axis of the graph shows hypothetical aggregate net premiums (what 18062 calls “the target amount”) an insurer might receive for some plan in some state. The y-axis shows the profits the insurer receives as a function of those aggregate net premiums assuming that claims (a/k/a “allowable costs”) are $11.4 million. The purple line shows what profits would have been as a function of premiums if 42 U.S.C. sec. 18062 did not exist. The blue line shows what profits will be after the payments required by 42 U.S.C. 18062 are taken into account. The khaki-shaded zone shows the payments insurers are supposed to receive (and the Secretary of HHS supposed to pay) under the statute. The green zone shows the payments insurers are supposed to make (and the Secretary of HHS supposed to receive) under the statute.

Profit as a function of premiums before and after 42 USC 18062

We can create a similar graphic in which the role of claims and premiums is reversed. The x-axis of the graph shows hypothetical aggregate claims costs (what 18062 calls “the allowable costs”) an insurer might receive for some plan in some state. The y-axis shows the profits the insurer receives as a function of those aggregate claims costs assuming that net premiums are $8.6 million. The purple line again shows what profits would have been as a function of premiums if 42 U.S.C. sec. 18062 did not exist. The blue line again shows what profits will be after the payments required by 42 U.S.C. 18062 are taken into account. The khaki-shaded zone again shows the payments insurers are supposed to receive (and the Secretary of HHS supposed to pay) under the statute. The green zone again shows the payments insurers are supposed to make (and the Secretary of HHS supposed to receive) under the statute.

Insurers profits as a function of claims before and after 42 USC 18062

If one looks at the slope of the blue lines — the ones that show profits after 18062 risk corridors are taken into account — they are much less steep for most of the domain than the purple lines — the one that show profits before 18062 risk corridors are taken into account. What this means is that, in some sense, it doesn’t matter to insurers all that much whether they price too low or too high, whether claims are lower than they thought or — due to adverse selection or otherwise — higher than they thought. Either they are going to pay money to the government or they are going to get money from the government. The risk of writing policies in the Exchange is greatly diminished.

In some sense, then, if section 18062 (1342) is fully implemented — an issue to which I will shortly return — insurers don’t act very much as profit-making enterprises within the Exchange making or losing money on the spread between premiums and claims. (This is even more true after the corporate income tax is taken into account) Instead, they are almost fronting for the government, providing their license, their claims processing abilities and their credibility to a scheme in which the government really bears the risk associated with the new Exchange-based system of providing insurance. A cynic might term the Exchanges as having gone 80% of the way towards a single payor system in which there is but minor variation in the benefits offered by insurance policies and claims processing contracted out to various insurance companies with the experience to do so.

The incentives issue

There are several implications of this consideration of 42 U.S.C. 18062. The first is to consider what incentives the system sets up for insurers. My tentative belief is that it incentivizes insurers to offer a low premium if they want to go into the Exchanges and this statutory provision may explain in substantial part why insurers priced their policies at rates lower than most expected. Let me see if I can sketch out the argument. If the insurer prices high, they are going to get very little business. Other insurers will take their business away by going low. If they price low, they will get a lot of the business. Sure, they may lose money if they price too low, but, if so, the government will reimburse them for most of their losses. And if they price right or still too high, they can make some money.

The graphic below illustrates this concept. The x-axis shows possible premiums the insurer might charge. The y-axis shows the profit of the insurer associated with that profit. As one can see, before section 18062, the insurer does best to charge about $2,840 in premiums; after 18062, the insurer does best to charge about $2,677 in premiums. Although the assumptions chosen to produce this graphic were somewhat arbitrary, it is interesting and suggestive to me that the magnitude of the reduction in premiums is roughly similar to that observed in the actual market place in which premiums came in several hundred dollars below that originally projected.

Profit as a function of premiums in a competitive market before and after 42 USC 18062

The imbalance issue

There’s a second issue suggested by the two graphics above (the ones with the shading) showing the effect of premiums and claims on profitability. They highlight that there is is no reason to think that the amount the Secretary receives will be equal to the amount the Secretary takes in. That would be true only if insurers happen, in aggregate, to price the policies just right. If insurers have underpriced the policies because they expected a larger — and correlatively healthier — pool, the graphics may quite accurately reflect what occurs and the Secretary will be obligated to pay out far more than the Secretary takes in. I have found no one who has written on this problem, no one who can explain where the money will come from to make the needed payments, or what mechanism will be used to reduce payments in the event, as I suspect, there will be an imbalance between the money collected and the money the Secretary is supposed to pay out.

And one final thing

Extra credit: Can anyone spot the uncorrected typo in 42 U.S.C. 18062? For answer, look here.

Risk Adjustment Under 42 U.S.C. §18063

The transitional reinsurance and risk corridors provisions only last until 2016. After that, assuming the Affordable Care Act survives in something like its present form for that long, insurers are protected from adverse selection only by the sleeping giant among the trio of protection measures: the “risk adjustment” provisions in ACA section 1343, codified at 42 U.S.C. §18063. The idea here is to equalize the playing field for insurers not based on the amount they actually pay out in claims (stop-loss reinsurance) or their actual profits (risk corridors) but on the risk they took in accepting insureds. It thus envisions this massive bureaucratic scheme whereby each individual purchasing a policy on an Exchange is scored (based on a complex federal methodology involving “Hierarchical Condition Codes“) and then, the insurers with high scores get paid by the insurers with low scores with the Secretary of HHS figuring out exactly how it works. To do this, the Secretary will need masses of sensitive information, including fairly granular accounts of the medical conditions of each person enrolled on an Exchange. The idea in the end, though, is to calm insurer fears that because of peculiarities of their plans, bad luck, or other factors, they tend up with a worse than average pool.

This provision will not save the Affordable Care Act from an adverse selection death spiral if enrollment stays low. This is because Risk Adjustment simply protects insurers from worse-than-average draws from the pool of insureds purchasing Exchange policies. It does nothing to protect insurers from having an overall pool of insureds purchasing Exchange policies that is higher risk than anticipated. If that larger pool is high risk on average, however, insurers will need to price their policies high, which will lead the lesser risk insureds to drop out, which will result in prices being raised again — the death spiral story.

The Bottom Line

The bottom line here is that two of the provisions (18061 and 18063) that purport to protect insurers from adverse selection really do little to protect insurers from the sort of adverse selection that is now appearing quite likely to develop: lower risk persons staying out of the Exchanges, period. The remaining provision, 18062, “Risk Corridors” in theory could give insurers some confidence that they will not lose their shirts if the pool stays small and high risk. But this is only true to the extent that insurers believe the Secretary of HHS will find some currently unknown pot of money with which to make payments when the number of insurer losers in the Exchanges far outstrips the number of insurer winners. If insurers doubt that the Secretary will be able to find the money and may simply resort to some pro-rata reduction in payouts under 18062(b)(1), they will have be less pacified in what must be their growing fears that the pool of insureds inside the Exchanges will, on balance, be far higher risk than they anticipated. And, if the Secretary finds money with which to honor the promises in section 18062, look for protests from those who were told that the Affordable Care Act would not have all that large a price tag.

Late Breaking News

As it turns out, the reinsurance and risk adjustment provisions are in the news today in an elliptical remark made at the end of a letter sent by the Center for Consumer Information & Insurance Oversight (CCIIO) that implements President Obama’s transitional “fix” with respect to canceled nongroup policies. He states:

Though this transitional policy was not anticipated by health insurance issuers when setting rates for 2014, the risk corridor program should help ameliorate unanticipated changes in premium revenue. We intend to explore ways to modify the risk corridor program final rules to provide additional assistance.

I believe this passage amounts to recognition by the President that providing a non-Exchange insurance substitute for generally healthy people who otherwise likely would have gone into the Exchanges will end up making adverse selection worse and further increase likely losses by insurers writing in the Exchanges. This, by the way, is why insurers are apparently furious about the President’s “fix.” The question, though, is where is the money going to come from to make the insurer’s whole. The statute appears to envision a zero sum game in which the winners compensate the losers. It does not appear to contemplate what seems ever more likely to occur: a game in which the only winning move is not to play.

Acknowledgements

If you are interesting in this topic, you should read the articles by Professor Mark Hall. I don’t alway agree with Professor Hall, but I have tremendous respect for his analysis. He is, in my view, one of the leading scholars with a generally positive view about the Affordable Care Act. You can find the articles here and here.

This blog is going to chronicle what I believe will be the implosion of the Affordable Care Act. I do not believe the Exchange based system of providing health insurance without medical underwriting is likely to work or that, if it does, it will not need far more massive propping up from federal taxes than is conventionally recognized. We’ll be looking at current events, the history of the Act, important court cases, and regulatory developments. Our tools will be a careful review of primary documents, some graphical and mathematical analyses, and references to important and insightful articles written by others.

Also, there is more to the Affordable Care Act than the Exchanges. There is more than the individual mandate. There is the employer mandate, the complex systems of federal reinsurance needed to backstop the Act, the reintroduction of medical underwriting under the “wellness label” and so much more. We’ll try as time permits to take a look at developments in these important areas too.

I recognize that many are writing on this topic and that it will be hard to stay a pace of such a fast moving target. But I do feel that there is a need for some hard and at least somewhat scientific look at what is going on. It will be my goal and burden to try to provide that in the months ahead.

Oh, and who am I? I’m Seth Chandler, a law professor at the University of Houston Law Center. I’ve taught insurance law, including life and health insurance law, for many years, been a co-director of the Health Law & Policy Institute, and done considerable work on the economics of insurance and its regulation. I’ve been very active using Mathematica, a system for doing mathematics by computer, and have shown how this tool can be used to analyze legal systems and many issues in insurance law such as adverse selection, moral hazard, correlated risk and a variety of issues in life, health, property and casualty insurance.

I should also add that the views expressed here are my own and do not necessarily reflect those of the University of Houston.

Exploring the likely implosion of the Affordable Care Act