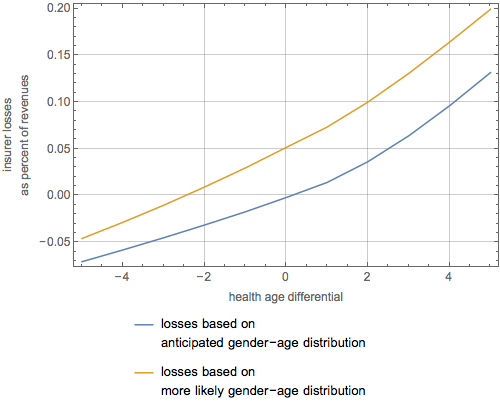

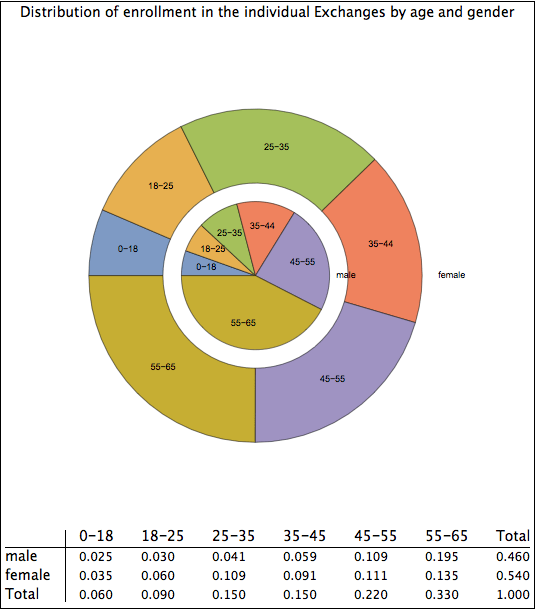

I’ve been doing some research into the effects of market concentration on health insurance premium pricing on the health insurance Exchanges run by the federal government. During the course of that research, I discovered what I first thought had to be a programming error on my part or a database error on the part of healthcare.gov: Silver and Gold plans that were costing individuals age 50 upwards of $2,000 per month. Yes, per month!

It turns out, however, that these exorbitant prices are not errors. They represent a clever attempt by several insurers in Virginia — Optima Health, Coventry Health Care of Virginia, Inc., Innovation Health Insurance Company, and Aetna — to get the federal government to pick up a substantial part of the tab for bariatric surgery. Here’s how it works. The insurer offers the consumer a premium that is often $2,000 per month ($24,000 per year) more than it charges for other essentially identical plans. The bonus is that the insurer offers the consumer, in addition to the usual benefits, bariatric surgery, which is otherwise subject to coverage restrictions in Virginia. Now, the only person who would rationally purchase such a policy is one who is pretty certain to undergo such surgery. And, as it happens, bariatric surgery (such as a gastric bypass) appears to cost between $20,000-$25,000. In effect, then, the insured prepays for the surgery via augmented premiums and perhaps piggybacks on the insurer’s bargaining power with surgeons to get a cheaper price.

So far, however, this does not seem like a compelling business model for insurance; at best it converts insurance into an elaborate financing scheme. But wait: if the insured has a relatively low income (and obesity correlates with poverty in modern America), under the cost sharing reductions provisions of the ACA (42 U.S.C. § 18071) the federal government now picks up much of the deductible and coinsurance that would otherwise be owed. Instead of there being, say, an $3,500 deductible and a $6,350 coinsurance limit, as there is under the Aetna Classic 3500 PD:MO policy offered in Virginia, if the person is poor enough (100-150% of federal poverty level), the deductible under the Aetna Classic 3500 PD: CSR 94% MO is now $300 and the out-of-pocket limit is now $1,250. The federal government is thus likely to pay for $3,200 to $5,100 of the bariatric surgery that would otherwise come out of the patient’s pocket.

Is this legal under the ACA? I believe it may well be. I don’t see a violation of the “metal tiering” provisions of the ACA. Under section 1302 of the ACA (42 U.S.C. § 18022), whether something qualifies as a Silver or Gold plan depends on the cost to the insurer of providing essential health benefits to a standard population, not on the cost to the insurer of providing its actual health benefits to the population it anticipates attracting. That may not be a very good system, but is the one in the law; it is probably simpler than some alternatives. Moreover, section 1302(b)(5) of the ACA makes clear that a health plan may provide “benefits in excess of the essential health benefits described in [the ACA].” And, since some states apparent include bariatric surgery in their list of essential health benefits, it’s hard to say that Congress implicitly rejected paying for this procedure.

Footnote: I suppose there could be an issue as to whether this plan conforms to Virginia insurance regulations. I’m not an expert on that, but my working assumption is that the Virginia regulatory apparatus has approved these plans.

Is what these insurers are doing appropriate? That’s a tricky question. Basically what they are doing is the result of a decision by the Department of Health and Human Services relating to implementation of sections 1201 and 1302 of the ACA. HHS, instead of creating some uniform concept of Essential Health Benefits for those states that elected not to make their own decision, instead decided to try and mimic features of the “largest plan by enrollment in the largest product by enrollment in the State’s small group market.” 45 C.F.R. 156.100) That essentially made it a bit a matter of luck as to the circumstances under which bariatric surgery or other weight loss programs would be covered by plans permitted to be sold after 2013 on the individual market. It meant that in some states the risk of needing (or badly wanting) bariatric surgery would be spread among all those purchasing non-grandfathered plans after 2014 whereas in other states either the risk would not be transferred at all or would be transferred, as in Virginia, only at a high price. The map below created by the “Obesity Care Continuum” shows how the states differ.

Obesity treatment under state benchmark plans

And should bariatric surgery itself be covered? It’s not an easy decision. On the one hand, bariatric surgery frequently results in part from poor health choices made by the individual. Yes, there may be contributing factors such as access to healthy foods, genetics, access to safe methods of exercise, but, still, most people have a choice not to become obese. And, if the condition is viewed as substantially the result of individual choice, the case for socializing and spreading the risk is weaker. On the other hand, there are plenty of risks that health insurance policies do pay for — both before and after the ACA — that likewise result substantially from personal choice. They cover orthopedic surgery for (mostly wealthy) people who choose to ski. They cover smoking related conditions — albeit for an additional premiums which, if actually collected, would still probably be less than the actuarial risk of tobacco use. They cover treatment in at least some forms for the variety of conditions created by substance abuse (drugs, alcohol). They sometimes cover non-surgical costs to which obesity contributes even when those problems are partly the result of individual choices. And they covers the costs of treating sexually transmitted diseases even when those diseases might, in some instances, have been prevented by safer sexual practices. Untangling fault out of medical need is often a tricky proposition indeed.

So, perhaps these Virginia insurers are doing the public a service by evading/working around restrictions in the Obamacare package of essential benefits provided in some states that were unduly narrow. Indeed, on this view, the problem is not that the federal government is subsidizing bariatric surgery, it is that individuals have to pay these enormous extra premiums for a risk that should be shared and that are shared in some states. It will be interesting to see what happens with these Virginia plans and whether what has started there extends to other states in which bariatric surgery is not presently considered an essential health benefit.

This past Thursday, the Obama administration issued its latest “fix” to the troubled roll out of the Affordable Care Act. The Center for Medicare & Medicaid Services issued a guidance that permits federal funds to go to insurers and insureds involved in sale of an individual health insurance outside of either a federally established or state-established Exchange. The premise of the guidance is that, in certain states such as Maryland, Massachusetts, Hawaii and Oregon, the complete dysfunctionality of the websites that were intended to determine eligibility for Obamacare subsidies may have led people to enroll in policies off the Exchanges; these purchasers, the guidance directs, should be treated the same as if the state Exchanges had made a timely determination and the individuals had enrolled in an Exchange policy. The guidance implements this concept by retroactively making such individuals eligible for premium tax credits the same as if they had purchased a policy on the Exchange and requires their insurers to readjudicate their claims both retroactively and for the remainder of the policy year as if they were eligible for the same cost sharing reductions that would have applied had they purchased a policy on the Exchange.

The Obama administration’s guidance calling for expenditures of taxpayer money plainly violates the Affordable Care Act. Unlike prior violations incurred in an effort to rescue the ACA from implementation and architectural infirmities, however, this one may actually hurt legal entities in a traceable and individualized fashion. Some off-Exchange insurers may have standing to challenge the violation in court should they have the courage to pursue that option.

The illegality problem

Here’s why the Obama administration’s action is unlawful.

Premium Tax Credits

Under section 1401 of the ACA, which creates new section 36B of the Internal Revenue Code, the government may provide premium tax credits to the individual only for a “coverage month.” The idea was that households with incomes less than 400% of the federal poverty level would ultimately see their federal income taxes reduced to help compensate for the cost of purchasing health insurance. But not any kind of health insurance purchase constitutes a “coverage month.” Under section 36B(c)(2)(A), a coverage month is only one in which the taxpayer “is covered by a qualified health plan … that was enrolled in through an Exchange established by the State under section 1311 of the Patient Protection and Affordable Care Act.” (emphasis mine) But the policies the Obama administration are now going to subsidize were not enrolled in through an Exchange established by a State (or the federal government); indeed, such is the entire “innovation” of this CMS guidance. And, thus, there is no statutory authorization for the federal government to be giving these taxpayers a credit.

Cost Sharing Reductions

Under section 1402 of the ACA (codified at 42 U.S.C. § 18071), the Secretary requires insurers to offer contracts with reduced cost sharing (deductibles, copays, out-of-pocket limits etc.) to individuals who purchase “Silver” plans. Purchasers are broken down into categories such that purchasers who fall into progressively lower income categories receive progressively more generous reductions. The program effectively converts “Silver” policies into “Silver-Plus”, “Gold Plus” and “Platinum Plus” policies. The government subsidizes insurers issuing these policies so that the cost sharing reductions should not cost them anything (providing the math is done properly). What the Obama administration is proposing is to extend these cost sharing reductions to insurance purchased off the Exchanges, at least where an application had been made to an Exchange.

Again, the problem is that the statute does not authorize cost sharing reductions for all “qualified health plans” sold on or off an Exchange. Under section 1402(a), such payments are authorized only for an “eligible insured.” And the definition of “eligible insured” is quite clear. Section 1402(b)(1) requires that an eligible insured “enroll in a qualified health plan in the silver level of coverage in the individual market offered through an Exchange …” (emphasis mine). Again, that pesky “through an Exchange” language gets in the way of the administration’s goal. The policies now being offered subsidization are precisely those not offered through an Exchange.” The payments to these insurers announced by the Obama administration are illegal. From a financial accountability standpoint, it is not much different than if the Obama administration just decided to give government money to those ineligible for Medicaid simply because it felt badly for some of them.

Why insurers may have standing to challenge the new regulations

The Obama administration has made a habit in its implementation of the Affordable Care Act to exploit the law of “standing.” This is the doctrine that usually denies individuals with generalized grievances about a law or its implementation from bringing suit. Standing usually requires, among other things, that the plaintiff in a legal action have suffered individualized injury from the statute. Thus, when the Obama administration simply declines to collect taxes (as with the refusal to enforce the employer mandate), it becomes challenging to find someone who can use the judicial system to overturn the action. A similar problem plagues efforts to challenge the Obama administration’s decision to permit insurers to continue to sell policies that do not conform to the requirements of the Affordable Care Act. It’s challenging to find an individual or business that is hurt in a particularized and traceable fashion.

With the latest lawless action, however, the Obama administration may have gone too far. Insurers who sold off Exchange will be hurt by the cost sharing reductions. The reason is “moral hazard.” The idea of moral hazard is that the more generous an insurance policy is the greater the frequency with which insureds encounter covered events. In the health insurance arena, people with lower co-pays and deductibles go to the doctor more. Indeed, the major reason for co-pays and deductibles is precisely to induce insureds to be judicious in their use of expensive medical services. Moral hazard is one of the major reasons that platinum policies cost more than bronze ones.

When cost sharing reductions imposed on off-Exchange insurers effectively convert their silver policies into silver-plus, gold-plus and platinum-plus policies, those insurers end up paying more in claims. And, while insurers selling policies on the Exchanges could have taken the induced demand created by cost sharing reductions into account in pricing their policies, there may well be insurers who sold only off the Exchange who, of course, did not take this additional moral hazard into account. Those insurers never dreamed that the government would reduce the amount its insureds would owe in cost sharing. Such insurers should have a strong case for standing in bringing a declaratory judgments to challenge the new guidance or, perhaps, in refusing to honor the demand for cost sharing reductions. Such insurers will, of course, need to be willing to take the political heat that may come from taking on an Executive Branch that more than ever is regulating their products.

A practical problem with imposition of cost sharing reductions on off Exchange policies

There’s also a practical problem with retroactive imposition of cost sharing reductions on off-Exchange insurers. The guidance issued last week does not seem to address it. There are a lot of ways of achieving cost sharing reductions. Some insurers might choose to reduce a deductible for some benefits. Other insurers might choose to reduce a different deductible. Still others might choose to keep the deductible but reduce copays. For this reason, insurers selling policies on the Exchanges needed to specify in advance how they were going to achieve cost sharing reductions for their policies. Hence the government’s “Actuarial Value Calculator.” But insurers selling policies off the Exchange may never have gone through such an exercise. Since CMS is now going to tell these insurers to readjudicate claims once they find out the income level of their insureds, the insurers are somehow going to have to come up, retroactively, with a system of cost sharing reduction. How the insurer chooses to do so will affect how much each insured gets rebated.

The demand for readjudication gives insurers a second basis for standing. Claims adjudication is not free. The insurer is now going to have to go back through claims and resolve them for a second time. Programming computers to adjust claims on a new basis is not costless. Figuring out whether a given service qualifies for cost sharing reductions is not costless. Cutting checks is not costless. And, having an actuary figure out what forms of cost-sharing reductions actually qualify as appropriate under the ACA is hardly costless either. In short, the CMS guidance places new and completely unanticipated burdens on insurers who may have chosen to sell off Exchange precisely to avoid some of the regulatory burden that comes with on-Exchange sales.

The possible abortion problem

The “fix” concocted by the Obama administration may also end up violating restrictions in the ACA on federal funds being used to fund elective abortions. I will admit this is a bit speculative, but here’s the issue. The general problem is that the ACA is an extremely integrated federal statute in which various provisions were enacted on the assumption that the conditions set forth in other provisions would hold. Once the administration starts lawlessly changing certain parts of the ACA, other sections of the act begin to unravel. With abortion, the problem is that section 1303 of the ACA (42 U.S.C. § 18023) prohibits federal tax dollars from being used to pay insurers via advances on premium tax credits to fund elective abortions. Nor may federal funds be used to reduce the amount of “cost sharing” (deductibles, copays) that certain poorer ACA policy purchasers would otherwise pay for services other than elective abortions. There’s an elaborate mechanism specified by the statute involving segregated accounts and allocations that keeps government out of the elective abortion business, almost as if the insured purchased two policies — one for elective abortion and one for everything else — only the latter of which was subsidized by the government. As a result, to the extent that various plans sold on the Exchanges provided for elective abortions — and apparently plans in at least nine states do so — they were structured to avoid receipt of such payments through segregated accounts.

Policies sold off Exchange never anticipated being the recipient of federal taxpayer money via premium tax credits and cost sharing reductions. To the extent they provided for elective abortion coverage — and probably some of them did — there would have been no reason to structure them with segregated accounts to avoid receipt of federal funds for abortion. Thus, when the Obama administration now proposes paying these off-Exchange policies federal tax dollars, the mechanisms for addressing abortion will not exist. I suspect that insurers who chose to sell off Exchange will not be excited by the administrative costs of now establishing segregated accounts. And, of course, if these off-Exchange insurers are not required by the Obama administration to prevent use of federal funds to pay for elective abortions, expect a firestorm of protest from those who believe that the federal government should not be subsidizing elective abortion.

Conclusion

One can be sympathetic to the plight of individuals in states such as Oregon, Maryland and others that wanted subsidized and community rated health insurance and, through no fault of their own, could not get it due to dreadful implementation of database systems that many states managed to accomplish with far fewer problems. In a world of cooperation, it might have been possible for the Executive branch and Congress to work together to hold these individuals harmless for these failings while preserving political and legal accountability for government officials and contractors who collaborated in the various debacles. Instead, however, we have an illegitimate attempt to use the Executive pen to write around the problem and bail out those responsible for embarrassing state implementations of the ACA.

This fix is not only lawless, it is very sloppy. It fails to prescribe a method by which the retroactive cost sharing reductions are to be done. It imposes costs on insurers who may have traded the opportunities of selling on the Exchanges in favor of the comparative regulatory freedom that came with selling off the Exchanges. If the guidance is not clarified, it may enable strategic behavior by those who purchased off the Exchange without suffering through a dysfunctional Exchange first; it may permit those people to apply for Exchange coverage now, reject it, but still obtain retroactive premium tax credits and cost sharing reductions for their off Exchange policies. And the guidance as it stands fails to take into account sensitivities concerning elective abortion funding. And, of course, this spending of taxpayer money appears to be proposed via a “guidance” and not even a full fledged regulation promulgated with at least minimal process.

For proponents of the “flexibility” the Obama administration has shown in implementing the ACA in the face of a hostile Congress, however, the main sloppiness with the latest guidance is that it enables the judicial branch to rule on the pattern of unilateral Executive action that has characterized recent implementation of the ACA. Insurers off the Exchange will be hurt by the cost sharing reductions imposed by the guidance and by the administrative costs it creates. The question is, will any of them have the guts to sue.

After going through notice and comment rulemaking, the Internal Revenue Service and the Department of the Treasury announced a “final rule” Monday that the employer mandate tax contained in the Affordable Care Act (26 U.S.C. § 4980H) will not apply at all to large “bubble” employers with between 50 and 99 workers until after December 31, 2015, and that employers with 100 or more workers can avoid the § 4980H tax from December 31, 2014 to December 31, 2015, by offering compliant health insurance coverage to 70% of its employees. These provisions amend previous IRS rulings that the employer mandate tax would start for plan years beginning after December 31, 2014, and that a large employer would need to offer health insurance coverage to 95% of its employees before it would be exempt from the potentially steep taxes imposed by section 4980H. Both the new final regulations and the earlier ones contradict the language of the Affordable Care Act, which states that the tax kicks in for plans beginning after December 31, 2013, and that an employer must offer health insurance coverage to “all” of its employees, not 95% and certainly not 70%, before it could escape this form of taxation.

In this blog entry, I want to accomplish three goals. I want to educate on the legal issues created by the recent regulation. I want to suggest both a conventional path to challenge the regulation and an unconventional path. And, I want to advocate. I want to implore the readers of this blog who are predisposed to think highly of President Obama to really question the precedent they let be set by permitting an Executive to refuse to collect a tax for years in circumstances where it is crystal clear that Congress has directed that it be done. There is a serious risk that future leaders may not share the same priorities as President Obama or themselves. Immunizing non-collection decisions from judicial correction will lead to collapse of government programs those sympathetic to our current President believe are worthy. It could also lead subsequent Congresses to refuse to enact government programs that make sense only if payment for them can not be subverted by a recalcitrant executive branch. In short, the people who should be most disturbed about what the President has done are his many friends who support not just the now-gutted employer mandate but who believe that the federal government has a major role in, as with the ACA, redistributing wealth acquired through the market. I would be very impressed if they mustered the courage to stand up to their friends.

A conventional path to challenge the employer mandate delay

Here are some plausible book moves in the legal chess game that likely lies ahead for the decision yesterday to modify the times and conditions under which the employer mandate will be enforced.

Standing

Opponents will hunt for a plaintiff. As others have noted, due to a doctrine called “standing,” this will not be so easy. Under Supreme Court precedent, the plaintiff is going to have to show (a) that the failure to enforce the employer mandate caused the plaintiff’s employer not to provide health insurance, (b) that the employer would provide the requisite form of health insurance if the tax were being enforced, and (c) that the plaintiff has actually been damaged by the failure of their employer to provide health insurance. If, for example, the employer says it is not sure what it would do if the tax were imposed, a case challenging the delay is likely to fail for lack of standing. Or if it could be shown that the failure of the employer to provide health insurance actually permitted the employee to purchase equally good and similarly priced health insurance on an individual Exchange, a case challenging the most recent IRS rules would likewise likely fail for lack of standing.

On the other hand, there may well be plaintiffs out there with standing to sue. There are about 18,000 firms with more than 50 employees in the United States. While some might make decisions on whether to provide health insurance that would be unaffected by the tax, if even 5% would admit to being affected by the tax — whose whole point, after all, is precisely to cause the result plaintiff will need to show — that would represent a universe of 900 potential businesses that almost surely employ more than 50,000 employees. It takes only one employee with standing to bring suit in order to challenge the legality of the President’s latest actions.

The best plaintiff would be an employee of a large corporation that has not provided “minimum essential coverage” (a/k/a/ health insurance) but which says, without equivocation, that it would do so if the employer mandate were in place. It would be best if the insurance the employer would have provided would cost the employee less than alternatives made available on the individual Exchanges. Perhaps, for example, the employee worked for an employer that had extraordinarily healthy employees — a large gymnasium chain filled with youthful, mostly male, low-health-cost physical trainers , for example — and could thus provide even minimally acceptable coverage via self insurance for less than the amount the employee could obtain on an individual Exchange.

Violation of the Administrative Procedures Act

Plaintiff’s argument

Once the standing hurdle is overcome, expect a challenge based on violation of section 702 of the Administrative Procedures Act (5 U.S.C. § 702). This law states: “A person suffering legal wrong because of agency action, or adversely affected or aggrieved by agency action within the meaning of a relevant statute, is entitled to judicial review thereof.” The plaintiff will argue that Congress has spoken with crystal clarity on the issue of when section 4980H was supposed to take effect: it was supposed to take effect for plan years beginning after December 31, 2013. There is nothing ambiguous about that date. There is nothing for the Supreme Court — let alone the Internal Revenue Service — to interpret.

Saying the year 2013 means the year 2015 is completely and totally absurd. The 2013 date chosen by Congress did not encompass the idea of “sometime in the kind of nearish future.” Congress balanced many factors, including the difficulty of complying with the statute and the desirability of having the employer mandate coordinate with many other provisions of the ACA that take effect starting in 2014. Moreover, given the enormous costs of the ACA, even in the reduced form taken by original projections, the $10 billion per year in tax revenues the employer mandate was expected to generate, was another reason to call for adoption in 2013. Under these circumstances, Congress did not choose to give large employers 5 years and 9 months to figure out how to finance and acquire health insurance for their employees; Congress thought 3 years and 9 months of “transitional relief” was perfectly adequate. Congress did not want the goal of reducing the number of uninsureds subverted by letting employers off the hook or, perhaps, the burdens on the subsidized Exchanges exacerbated by large employers not pulling their weight.

The situation is no better, plaintiffs will argue, for the Obama administration’s decision in the regulations to distinguish amongst different sorts of large employers, letting employers with between 50 and 99 employers off the hook in the year 2015 while compelling at least some employers with more than 100 employees to provide health insurance in the same year. The statute carefully defined large employers in this context to mean more than 50 employees and deliberately chose 50 as the point at which to balance the importance of employer-provided insurance against the administrative and financial burdens of forced provision. Congress did not choose, for example, to stage imposition of the employer mandate first on the biggest of the large employers and a year or so later on the smaller within that group.

Finally, even if there was some basis for staging imposition of the mandate, plaintiffs will argue, the Obama regulations have butchered the provision of 4980H that calls for imposition of a large tax unless the employer offers insurance to all eligible employees. Conceivably the agency could stretch the “all” concept to 95% as it did before. Perhaps 95% could be justified as a bright line proxy for the sort of honest mistakes that Congress would not have wanted to serve as a predicate for a hefty tax. But when the Executive branch goes from “all” to 70% it can not be said with a straight face that anyone is speaking about providing a safety zone against honest mistakes. Now we are talking an entirely different regulatory regime. The Administrative Procedures Act does not give the Executive branch the power to legislate; and if it did so, the APA would itself be unconstitutional.

The Chevron Deference rebuttal

Expect the defendants to fight back with something known in the law as “Chevron deference.” This widely cited doctrine emerges from the observation that executive agencies actually have a lot of expertise in interpreting statutes in their area. Therefore, it should be assumed that Congress would have wanted the agency to have considerable leeway in interpreting statutes. So long as the agency follows the right procedures in developing its rules, such as the “notice and comment” rulemaking that preceded the recent pronouncement on the employer mandate, the rules developed by the agency are lawful and binding even if the court would itself not have interpreted the statute the way the agency does. The main caveat — and it is the big “Step 1” in the Chevron process — is that the agency’s interpretation has to be a reasonable interpretation of the statute, a “permissible construction.”

But, the plaintiff will argue — and I believe with great success — “Chevron deference” does not exist where the statute is really not subject to interpretation at all. As the Supreme Court said in Chevron, USA v. Natural Resources Defense Counsel, Inc., “If the intent of Congress is clear, that is the end of the matter; for the court, as well as the agency, must give effect to the unambiguously expressed intent of Congress.” And it is hard to imagine anything clearer than “December 31, 2013.” It is hard to imagine a construction of “all” — particularly in a context in which alternative taxes (4980H(b)) are placed on employers that offer compliant health insurance to at least some of their employees– that could mean 70%. It is just not a reasonable construction.

“But wait,” I hear some judge asking. “Are you saying that the IRS could not give a company a few extra weeks to get health insurance? Are you saying that the IRS could not give companies any leeway in obtaining health insurance and saying that if a single employee goes uninsured the company is subject to a $2,000 per employee (minus 30) tax?” No, not quite. As to the few weeks grace period, I do not believe the IRS can interpret the statute to permit such to occur automatically. I understand giving a select company a few extra weeks if there were extraordinarily circumstances — a natural disaster, an unintentional failure of communications — but Congress (a) already gave the companies more than a three year grace period to get health insurance for their employees and (b) assesses the tax on a monthly basis, $166.67 per employee per month, so that the company would not in fact be hit with a $2,000 whammy. And as to whether the IRS could give companies some leeway, again, if there were a factual showing that it would be easy for a company to mess up on a small percentage of employees and that some accommodation was necessary in a particular case, I do not believe some leniency would subvert the intent of Congress. But I see no evidence from the IRS that a 30% mistake zone is necessary; instead, this appears to be a way of simply mellowing out a tax regime that the Executive branch now believes (perhaps rightly) is too harsh without, however, asking Congress, who might actually agree were the case respectfully put to them, to assist with a modification of the statute.

The Prosecutorial Discretion rebuttal

The better argument the Obama administration will muster goes under the name “prosecutorial discretion.” The idea, buttressed by many case, including the 1985 Supreme Court decision in Heckler v. Chaney, is that the Executive branch needs lots of leeway in determining enforcement priorities and there is therefore a very strong presumption against judicial review of decisions not to prosecute and not to pursue agency enforcement actions. And while, to be sure, most of these cases arise where the government is less transparent about its enforcement priorities, surely the government should not be restricted in its otherwise existing discretion just because it sought notice and comment before deciding what to do and was transparent enough to publish the basis on which it would make decisions.

Here are some quotes from Chaney which the Obama administration’s attorneys are likely to throw in the face of any potential challenger to its regulations.

“[A]n agency decision not to enforce often involves a complicated balancing of a number of factors which are peculiarly within its expertise. Thus, the agency must not only assess whether a violation has occurred, but whether agency resources are best spent on this violation or another, whether the agency is likely to succeed if it acts, whether the particular enforcement action requested best fits the agency’s overall policies, and, indeed, whether the agency has enough resources to undertake the action at all. An agency generally cannot act against each technical violation of the statute it is charged with enforcing. The agency is far better equipped than the courts to deal with the many variables involved.”

“In addition to these administrative concerns, we note that, when an agency refuses to act, it generally does not exercise its coercive power over an individual’s liberty or property rights, and thus does not infringe upon areas that courts often are called upon to protect.

“[A]n agency’s refusal to institute proceedings shares to some extent the characteristics of the decision of a prosecutor in the Executive Branch not to indict — a decision which has long been regarded as the special province of the Executive Branch, inasmuch as it is the Executive who is charged by the Constitution to “take Care that the Laws be faithfully executed.” U.S.Const., Art. II, § 3.”

“The danger that agencies may not carry out their delegated powers with sufficient vigor does not necessarily lead to the conclusion that courts are the most appropriate body to police this aspect of their performance.”

Sounds bad for our plaintiff!

There is, however, the noteworthy footnote 4 in Chaney that should give plaintiffs some hope. After all, Chaney articulates the doctrine of agency discretion as a strong presumption, not an irrebutable one. Here is what Justice Rehnquist said:

We do not have in this case a refusal by the agency to institute proceedings based solely on the belief that it lacks jurisdiction. Nor do we have a situation where it could justifiably be found that the agency has “consciously and expressly adopted a general policy” that is so extreme as to amount to an abdication of its statutory responsibilities.” See, e.g., Adams v. Richardson, 156 U.S.App.D.C. 267, 480 F.2d 1159 (197) (en banc). Although we express no opinion on whether such decisions would be unreviewable under § 701(a)(2), we note that, in those situations, the statute conferring authority on the agency might indicate that such decisions were not “committed to agency discretion.”

In other words, plaintiffs may be able to argue that this is not a case where the agency is in fact making enforcement decisions based on budgetary priorities or the probability of success. Few if any of the reasons behind the discretion doctrine exist here; the doctrine of discretion should not exist for its own sake precisely because it derogates from popular sovereignty exercised via Congress. There should be enough of a paper trail for the plaintiff to show persuasively that, the agency is making an enforcement decision based on a sense that the statute is unfair or unwise or, if someone has left a smoking-gun email around, pure political considerations.

The facts of Adams bear some resemblance to the facts here. Just as here there is a statute calling on the IRS to levy a tax starting in 2014, in Adams, there was a statute that directed certain federal agencies to terminate or refuse to grant assistance to public schools that were still segregated. Just as here the agency in charge (the IRS) is apparently going to refuse to pursue that tax in 2014 (and 2015) as a matter of policy, in Adams the federal agency in charge (Health, Education and Welfare) effectively adopted a policy of refusing to stop funding segregated public schools. The fact that there was general non-enforcement as a matter of policy distinguished the case, in the view of the Adams court, from conventional prosecutorial discretion.

The other hope for plaintiffs would be to use the extreme example of this case as a way of infusing contemporary doctrine on review of agency inaction with some thoughts from Justice Thurgood Marshall in his concurring opinion in Heckler v. Chaney. Marshall’s thoughts might have particular appeal to Justice Elena Kagan, for example, who, in addition to being fair minded, was one of Marshall’s clerks close to the time Chaney was decided. Marshall, who perhaps unfortunately took an expansive view of the majority opinion in order to criticize it, and who appears to have drafted without noting its cautionary footnote 4, wrote several quotations that might prove helpful if introduced gently.

“[T]his ‘presumption of unreviewability’ is fundamentally at odds with rule-of-law principles firmly embedded in our jurisprudence, because it seeks to truncate an emerging line of judicial authority subjecting enforcement discretion to rational and principled constraint, and because, in the end, the presumption may well be indecipherable, one can only hope that it will come to be understood as a relic of a particular factual setting in which the full implications of such a presumption were neither confronted nor understood.”

“But surely it is a far cry from asserting that agencies must be given substantial leeway in allocating enforcement resources among valid alternatives to suggesting that agency enforcement decisions are presumptively unreviewable no matter what factor caused the agency to stay its hand.” (emphasis in original)

Moreover, conceivably traction might be gained in an attack on the employer mandate regulations by limiting the theory of the case to agency failure to enforce a regulation as opposed to decisions of prosecutors not to pursue criminal charges. As Justice Marshall wrote:

“A request that a nuclear plant be operated safely or that protection be provided against unsafe drugs is quite different from a request that an individual be put in jail or his property confiscated as punishment for past violations of the criminal law. Unlike traditional exercises of prosecutorial discretion, “the decision to enforce — or not to enforce — may itself result in significant burdens on a . . . statutory beneficiary.” (citing Marshall v. Jerrico, Inc.,446 U. S. 238, 446 U. S. 249 (1980)).

Nonetheless, plaintiffs will have to contend with the fact that (a) Thurgood Marshall’s ideas on prosecutorial and agency discretion were not shared by the remainder of the court and (b) the extreme conditions found in Adams have not been found in other cases in which such “footnote 4” claims have been brought. The presumption established by Heckler v. Chaney has clearly remained a very strong one.

A Tax Whistleblower action: An unconventional path for challenging the employer mandate delay

The greatest difficulty for those disturbed by the Obama administration’s regulatory subversion of its own law is the prosecutorial discretion argument discussed above. Almost everyone thinks there should be some degree of prosecutorial discretion and the case law strongly and pretty persuasively supports the idea that the judicial branch should at least seldom be able to force prosecutors or agencies to more forcefully enforce laws, particularly where Congress has the ability to coerce the Executive branch to do so through aggressive techniques such as appropriations or, I suppose, in the most egregious cases, impeachment. The tension will be whether and under what circumstances the Executive branch under the rubric of “prosecutorial discretion” can completely subvert the language and intent of a statute through a refusal to collect a tax.

So, might there be another path for attacking the regulation, one either already in existence or one created by Congress?

IRS Form 211 (filled in)

Perhaps. There is a remedy on the books already that might at least make the Obama administration squirm. It would do so because it might make clear that what was going on was not an exercise in prosecutorial discretion at all, but rather an effort to rewrite the statute. The idea is to for anyone at all to be a whistleblower under 26 U.S.C. § 7623 and to advise the IRS via a Form 211 that a particular large employer, preferably one that had over 1030 employees and therefore could owe more than $2,000,000 in 4980H taxes, had failed to provide health insurance to its employees and had failed to pay any of the taxes created in section 4980H. The whistleblower does not need to show fraud to file a Form 211. The whistleblower merely needs to show that there has been an underpayment of tax. Of course, to protect against claims of bad faith, the Form 211 should disclose that the claimant knows that the employer is relying on IRS regulations as a defense but that the claimant asserts that those regulations are unlawful.

Now, I would not expect the IRS to then take a customary next step of pursuing the non-paying large employer for the 4980H taxes. I would not expect the IRS to provide any award to the whistleblower that would be available if the IRS had actually collected any money as a result of the Form 211 filing. But it is this failure of the IRS to do anything or to pay anything that might trigger the right of the Form 211 claimant to bring a legal action in which the legality of the Obama administration’s delay of the employer mandate could be challenged. Section 7623(b)(4) of the Internal Revenue Code permits “any determination regarding an award” to be appealed to the Tax Court, which has jurisdiction over such appeals.

Again I would not expect the IRS to take such an appeal lying down. The IRS will claim that it has complete discretion over whether to pursue a taxpayer brought to its attention under Form 211. A decision to the contrary could create the potential for massive, expensive litigation. Moreover, the IRS will say, the appeal permitted by section 7623(b)(4) is one over the size of any award not over whether the IRS decides to proceed with any administrative or judicial action based on information contained in a Form 211.

These will be strong arguments. They may well persuade the Tax Court. They may well persuade a Circuit Court of the United States to which an adverse decision of the Tax Court can be appealed. But what they will expose is that the IRS does not regard the regulatory changes it has made as merely ones of prosecutorial discretion — deciding where and how to expend its resources detecting underpayments. Here, that work has already been done for them. Instead, they constitute a substantive rule on the circumstances — none for 2014 and few for 2015 — under which a large employer that fails to provide health insurance should be liable for taxes that Congress demanded be paid under section 4980H. Perhaps, therefore, the Tax Court, or, on appeal, an Article III appellate court or the Supreme Court might summon up the courage to say, kind of like the suggestion in footnote 4 in Chaney, that, although the IRS may have broad discretion, it does not have “discretion” to abdicate its statutory responsibilities. It can not fail to pursue obvious tax deficiencies brought to its attention by a third party when the only reason for so declining is an unlawful regulation promulgated by the IRS in a usurpation of legislative powers. Whatever one thinks of the merits of the employer mandate, such a decision, in my view, would be a healthy restoration in the balance of power among the federal branches of government.

One other note

It was suggested by a friend that Congress could overcome such exercises of prosecutorial discretion by an expanded use of “qui tam” lawsuits. This remedy, which dates back to the 13th Century and has seen a resurgence over the past 20 years in the United States, allow a private citizen to bring a civil action in the name of the government and collect some of the money otherwise owed to the government. Qui tam litigation is a broad and complex subject on which I do not pretend great expertise. But, as I understand it, qui tam lawsuits generally permit a private party to go forward only if the Executive branch either supports the private party’s efforts at supplemental enforcement of a regulatory norm or at least acquiesces to it. Under 31 U.S.C. 3730(c)(2)(A) and case law interpreting one of the major branches of qui tam actions, the government can basically kill a qui tam lawsuit to which it objects even if the underlying claim is meritorious. It would therefore take a special qui tam statute that expressly squelched this veto power in order for such action by Congress to permit an attack on the delay of the employer mandate. More fundamentally, however, the probability of a gridlocked Congress enlarging qui tam rights to facilitate judicial overturning of the Obama administration’s delay of the employer mandate and doing so over a presidential veto is about zero.

Caution

I’m forging some new ground here and laying out arguments without weeks of legal research in order to get them on the table. I am likely missing things or even, perchance, getting things wrong. My hope, however, is that what I’ve written is intelligent and helpful enough to get others to discuss further and potentially take action on the serious legal issues involved when a President decides not to collect taxes that Congress has clearly demanded be paid.

Acknowledgement

This blog post benefited greatly from a conversation with Professor Sapna Kumar, an expert on administrative law. I, of course, am responsible solely for any mistakes made herein and I have no idea what Professor Kumar — whose main focus is the intersection of administrative law and intellectual property — thinks about the Affordable Care Act or its implementation. So, if you don’t like the post or there is something wrong, don’t blame her.

The Congressional Budget Office just issued a report that assumes the Affordable Care Act system of individual policies sold in Exchanges without medical underwriting can remain relatively stable. Tightly bound up with that assumption is its prediction about a controversial ACA program known as “Risk Corridors” that requires profitable insurers to pay the federal government up to 80% of profits they make on policies sold on the Exchanges but that also requires the federal government to pay insurers up to 80% of the losses they suffer from policies sold on the Exchanges. The CBO now believes it has enough information to predict that Risk Corridors will actually make money — $ 8 billion over three years — for the government at the expense of insurers.

This CBO prediction of $8 billion in federal revenue, which has gained much publicity, pulls the rug out from critics of the ACA such as Senator Marco Rubio who have introduced legislation that would repeal Risk Corridors as an insurance industry “bailout.” Such a blunting of Senator Rubio’s proposed repeal legislation is crucial in the ongoing battle over the ACA because repeal of Risk Corridors could result in insurers (who just might not believe the CBO’s numbers) exiting the Exchanges for fear of having no government protection against losses resulting from unfavorable experiences in the new market the government has created. On the other hand, if the CBO is just getting its number wrong, Rubio’s case for repeal of Risk Corridors remains as strong (or problematic) as it ever was. The CBO projection is also important because Risk Corridors nets the government money if and only if the ACA works, insurers are able to make some profits, and a death spiral never takes hold. And this, as readers of this blog are aware, is a prediction about which many have serious doubts.

Here’s the short version of the rest of this post.

I’ve done the math and I don’t see how the CBO is getting this $8 billion number unless it is assuming either very high enrollment in policies covered by Risk Corridors or very high rates of return made by insurers. Or it made a mistake. I don’t think the CBO’s own numbers support very high enrollment in policies covered by Risk Corridors and I don’t believe either an emerging reality or the CBO’s own rhetoric justify assuming very high rates of return. So I think the CBO ought to take a second look at its prediction. People should not yet make policy decisions based on the CBO estimate.

Reader, you now have a choice. I’m afraid that the next several paragraphs of this post become very technical. It’s kind of forensic mathematics in which one attempts to use statistics and numerical methods to deduce the circumstances under which something said could be true. If that sounds dreadful, scary or tedious, I would not protest too loudly were you to skip ahead to the section titled “How could I be wrong?” Before you leave, however, realize that what I am attempting to accomplish in the part you skip is a form of proof by contradiction. I prove that if what the CBO was saying were true, then insurers would have to be making 8% profit. But nobody, including the CBO thinks they will make 8% profit, so the $8 billion number can’t be right.

On the other hand, dear reader, if you liked the Numb3rs television show (including my minor contributionsthereto) or math or detective work or just care a lot about the Affordable Care Act, the rest of this post is for you. What I am about to discuss is not only exciting math, but also the soul of the Affordable Care Act — whether the individual Exchanges without medical underwriting can remain relatively stable.

Forensic mathematics in action

Conceptually, here’s the calculation one needs to do. What we want to figure out is the distribution of insurer profits (measured as a ratio of expenses divided by premium revenues) upon which the CBO must be relying. I assume the CBO is using a member from the “Normal” or “Lognormal” family of distributions because those are typical models of financial returns and there is little reason to think that the distributions of insurer profits (expenses minus revenues) will materially depart from those assumptions. To continue reading this post, you don’t have to know exactly what those distributions are except that they look for our purposes like the “bell curves” you have seen for many years. I’ve placed a graphic below showing some normal (blue) and lognormal (red) distributions. Although it should not matter all that much, I’m going to use a lognormal distribution from here on in because the ratio of insurer expenses to premiums should never be negative and the lognormal distribution, unlike its normal cousin, never takes on negative values.

Examples of probability density functions for normal and lognormal distributions

The problem is that there are an infinite number of lognormal distributions from which to choose. How do we know which distribution the CBO is emulating in its computations? How do we know just how positive the CBO assumes the individual Exchange market is going to be on average or how dispersed insurer profits are going to be? As it turns out, the complexity of the lognormal distribution can be characterized with just two “parameters” often labeled μ (mu, the mean of the distribution) and σ (sigma, the standard deviation of the distribution). Once we have those two parameters (just two numbers), we can deduce everything we need about the entire distribution.

Now, to solve for two parameters, we often need two relationships. And, thoughtfully, the CBO has given us just enough information. It has told us how much money in total it intends to raise from Risk Corridors ($8 billion) and the ratio (2:1) between money it collects from profitable insurers and the money it pays out to unprofitable insurers. These two facts help constrain the set of permissible combinations of Risk Corridor populations (the number of people purchasing policies in plans subject to the Risk Corridor program) and insurer profitability distributions. What I want to show is that it takes an extremely high Risk Corridor population in order to get rates of return that are not way larger than most people — including the CBO — think likely to occur.

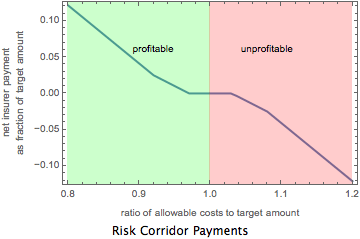

I first want to calculate the amount of money insurers would pay to HHS under the Risk Corridors program if the total amount of premiums collected were $1. Some of the payments — those by highly profitable insurers — will be positive. Those by highly unprofitable insurers will be negative. To do this I take the “expectation” of what I will call the “payment function” over a lognormal distribution characterized by having a mean of μ and a standard deviation of σ. By payment function, I mean the relationship shown below and created by section 1342 of the ACA, 42 U.S.C. § 18062. This provision creates a formula for how much insurers pay the Secretary of HHS or the Secretary of HHS pays insurers depending on a proxy measure of the insurer’s profitability. The idea is to calculate a ratio of “allowable costs” (roughly expenses) to a “target amount” (roughly premiums). If the ratio is significantly less than 1 (and outside a neutral “corridor”), the insurer makes money and pays the government a cut. If the result is significantly greater than 1 (and outside the neutral “corridor”), the insurer loses money and receives a “bailout”/”subsidy” from the government. The program has been referred to with some justification as a kind of “derivative” of insurer profitability, the ultimate “Synthetic CDO.”

The graphic below shows the relationship contained in the Risk Corridors provision of the ACA. The blue line shows the net insurer payment (which could be negative) to the government as a function of this proxy measure of the insurer’s profitability. Ratios in the green zone represent profits for the insurer; ratios in the red zone represent losses. Results are stated as a fraction of “the target amount,” which, as mentioned above, is, roughly speaking, premium revenue.

How much the insurer pays (positive) or receives (negative) under Risk Corridors as a function of a ratio-based measurement of profitability

When we do this computation, we get a ghastly (but closed form!) mathematical expression of which I set out just a part in small print below. (It won’t be on the exam). I’ll call this value the totalPaymentFactor. Just keep that variable in the back of your mind.

Excerpt of the formula for insurer total payout

I next want to calculate the amount of payments profitable insurers will make to HHS. To do this, we truncate the lognormal distribution to include only situations where the ratio between premiums and expenses is greater than 1. Again, we get a pretty ghastly mathematical expression, a small excerpt of which is shown below. I will call it the expectedPositivePaymentFactor.

Formula for expected negative insurer payments under risk corridors over a truncated lognormal distribution

Finally, I want to calculate the amount of payments unprofitable insurers will receive from HHS. To do this, we truncate the lognormal distribution to include only situations where the ratio between premiums and expenses is less than 1. Again, we get a pretty ghastly mathematical expression, which, for those of you who can not get enough, I excerpt below. I will call it the expectedNegativePaymentFactor.

Formula for expected positive insurer payments under risk corridors over a truncated lognormal distribution

The CBO has told us in its recent report that the government will collect twice as much from profitable insurers (expectedPositivePaymentFactor) as it pays out to unprofitable ones (expectednegativePaymentFactor). We can use numeric methods to find the set of μ, σ combinations for which that relationship exists. The thick black line in the graphic below shows those combinations.

Black line shows combination of mu and sigma that result in the correct ratio of positive and negative insurer payouts under Risk Corridors

To determine which point on the black line above, which combination of the parameters μ, σ , is the actual distribution, we need to use our information about the totalPaymentFactor. The idea is to realize that the totalPaymentFactor must be equal to the quotient of the CBO’s estimated $8 billion and the total premium collected by Risk Corridor plans over the next three years. But we know that the total premium collected should be equal to the mean premium charged by the Exchanges multiplied by the number of people in Risk Corridor plans. Some math, discussed in the technical notes, suggests that the mean premium under the ACA is about $3,962. And the CBO accounts for 8 million people being in Risk Corridor plans in 2014, 15 million being in Risk Corridor plans in 2015 and 25 million being in Risk Corridor plans in 2016. This means that the total premiums collected by insurers under Risk Corridor plans over the next 3 years should be about $190.2 billion. And this in turn means that the totalPaymentFactor must be 0.042.

Ready?

It turns out that of all the infinite number of lognormal distributions there is only one that satisfies the requirements that (a) the government will collect twice as much from profitable insurers (expectedPositivePaymentFactor) as it pays out to unprofitable ones (expectednegativePaymentFactor) and (b) for which the totalPaymentFactor takes on a value of 0.042. It is a distribution in which the mean value is 0.923 and the standard deviation is 0.113. I plot the distribution below. A dotted line marks the break even point for insurers. Points to the left of the break even line correspond with profitable insurers; points to the right correspond with unprofitable insurers.

Lognormal distribution of insurer profitability consistent with CBO data

Here are some factoids about the uncovered distribution. The average insurer will have expenses that are 92.3% of premiums and the median insurer will have expenses that are only 91.6% of profits. In other words, they will be making 7.7 cent and 8.4 cents respectively on every dollar of premium they take in. For reasons discussed below, this is a difficult figure to accept. It is particularly difficult in light of the pessimistic news that is emerging about things such as the age distribution of enrollees , reports from Deutsche Bank that one of the largest insurers in the Exchanges, Humana, expects to receive (not pay!) a lot of money under the Risk Corridors program, the hardly exuberant forecasts of other publicly traded insurers about the ACA, and the recent general downgrading of the insurance sector by Moody’s partly because of the ACA.

Implicit in my finding about the most likely distribution of profitability is an assertion by the CBO that 76% of insurers will be profitable under the ACA while 24% will be unprofitable. About 17% will be sufficiently unprofitable that they will receive subsidies (a/k/a bailouts) from the federal government and 9% will be sufficiently unprofitable that their marginal losses will be covered at 80%. Only 15% of insurers will be “inside” the risk corridor and neither pay nor receive under the program.

How could I be wrong?

I feel confident that I’ve done the ” gory math part” of this blog post correctly. Mathematica, which is the software I’ve used to do the integral calculus and the numeric components involved just does not make mistakes. I also feel pretty confident that I understand how the Risk Corridors program works under section 1342 of the ACA. That’s kind of my day job. And so, readers who skipped down to this part, I do believe that if the CBO were right about the $8 billion, that could only happen if insurers were, on average, earning an implausible 8% in the Exchanges.

If I’m wrong, then, it is because, except for the little issue I will mention at the end, I have made bad assumptions about the total premiums insurers expect to collect over the next three years in policies covered by Risk Corridors. That error could come from two sources. I could have the mean premium per policy wrong or I could have the relevant enrollment wrong. Let’s look at each of these.

Could I be wrong about the mean premium?

I computed the mean premium in the computation above by using data collected by the Kaiser Family Foundation on the ratio of premiums by age under most insurance plans and the typical Silver plan premium for a 21 year old (non-smoker). I then used the original forecast about the age distribution of insureds to compute an expected premium. I got $3,962. And this number seems very much in line with earlier HHS estimates, which were that mean premiums would be $3,936. So, I think I have the mean premium correct.

Could I be wrong about the number of people in Risk Corridor plans?

I computed the number of people enrolled in policies covered by Risk Corridors by looking at the CBO’s own figures. I’m not vouching that the CBO is right in its projections, but this is not the day to argue that point. The CBO now says (Table B-3, p. 109) that individual enrollment in the Exchanges will be 6 million, 13 million and 22 million respectively over the next three years. And it says that employment-based coverage purchased through Exchanges (which I assume are SHOP Exchanges) will be 2 million, 2 million and 3 million respectively. So , by addition, that’s where the figures I used of 8 million, 15 million and 25 million come from. I’m not aware of anyone else who would purchase a policy subject to Risk Corridors. Again, bottom line, I don’t think I’m doing anything wrong here.

The little issue at the end: Could ACA definitions be responsible for the incongruity?

The only other conceivable explanation of the divergence between the CBO figures and my analysis is that I am failing to take a subtlety of Risk Corridors into account. Remember, careful readers, that sentence earlier up that started out: “The idea is to calculate a ratio of “allowable costs” (roughly expenses) to a “target amount” (roughly premiums).” I stuck in the “roughlies” because the “allowable costs” are not exactly expenses and the “target amount” is not exactly premiums. When you look at the statute and the regulations, you can see that both of these terms are tweaked: basically you subtract administrative costs from both values. And you subtract reinsurance payments from expenses — but that makes sense because the insurer reduced premiums in anticipation of those reinsurance payments.

So, in the end, I don’t see why these subtleties should affect my analysis in any significant way. But I am not infallible. And I do pledge that if someone points out an error to me, I will dutifully assess it and report it.

Sensitivity Analysis

Out of an abundance of caution, however, I have rerun the numbers on the assumption that premium revenue from policies subject to Risk Corridors is 50% greater than my original estimate either because of an underestimate of per policy costs or a failure to understand that there is some additional group within Risk Corridors protection. When I do that, though, I find that the ratio of expenses to premiums is 0.943, meaning that insurers are still earning a pretty substantial 5.6%. Although that is more believable than the earlier figure of 7.7%, it is still pretty high.

Conclusion

To be honest, it makes me very nervous to say that the CBO did its math wrong or, worse, to accuse it of bad faith. These are intelligent, educated professionals and they have access to a lot more data and a lot more personnel than I do. Here at acadeathspiral it’s just me and my little computer along with some very powerful software. On the other hand, it’s not as if the CBO hasn’t been wrong before. It assumed earlier that the government would reduce its deficit $70 billion over 10 years as a result of Title VIII of the ACA (the so-called CLASS Act on long term care insurance) when many independent sources believed — rightly as it turned out — that the now-repealed CLASS Act was obviously structured in a way that could never fly. The CBO assumed in July 2012 that 9 million people would enroll in the Exchanges in 2014, a number that is now down to 6 million. And, while there are explanations for each of these changes, the bottom line is that CBO is fallible too.

So, if I might, I would strongly urge the CBO to double check its numbers and provide more information on the data it relied upon and the methodology it employed in getting to its results. I’d ask Congress, which has ongoing oversight of the ACA, to insist that the Congressional Budget Office, which is exempt from Freedom of Information Act requests from ordinary citizens, provide further detail. American healthcare is indeed too important to have policy decisions made on the basis of what could be some sort of mathematical error.

Really Technical Notes

I’m using a reparameterized version of the lognormal distribution that permits direct inspection of its mean and standard deviation rather than the conventional one, which in my opinion is less informative. The explanation for doing so and the formula for reparameterization is here.

To compute the average premium, I took the premium ratios used by the Kaiser Family Foundation, calibrated it so that a 21 year old was paying the national average payment for a silver plan purchased by a 21 year old. I then computed the expected premium over the distribution of purchase ages originally assumed by those modeling the ACA.

Those optimistic about the success of the Affordable Care Act have been noting over the past several months that the premiums offered by insurers have been lower than those earlier forecast. But if one looks carefully at the original rhetoric, the comparison tends to be between some of the lowest premiums offered within a jurisdiction and those originally forecast. And this metric, according to ACA proponents, is appropriate because they expect consumers to focus purchases on the lowest cost policies.

But what if the lowest premiums are lower than expected not because the mix of purchasers is thought to be fine or because of cost cutting measures enabled by the ACA, but simply because all this metric exposes is the work of the insurers who priced their policies below actual risk? The “winner’s curse” is the term economists and game theorists give to situations in which, in an atmosphere of uncertainty, people bid on an item in an auction environment. What will often happen is that the “winning” bidder will tend to be one that loses money.

It is quite possible that all we are seeing with “low” ACA pricing, as measured by ACA proponents, is “the winner’s curse” in action. We may well be looking at insurers who (a) got it wrong or (b) thought the government would most greatly subsidize their losses or (c) for strategic reasons, decided to sell a “loss leader” in the first year or so of the ACA in order to lock consumers into their networks and their doctors with the idea that they could substantially raise premiums in the future. If this hypothesis is correct, individual policies under the Exchange are a lot less stable than many ACA proponents are asserting.

To summarize the results of the computations shown below, if the mean premium charged by insurers selling a type of policy (Silver HMO Plans, for example ) in a given geographic region (Harris County, Texas, for example) reflects the true risk posed by ACA policy purchasers, about 20% of the low bidders — the ones that I suspect will get a disproportionate share of the business — stand to lose at least 20% on their policies before the Risk Corridor program bails them out.

The big story as the ACA unfolds may be that some insurers — the ones who ended up with the business — simply made an error of exuberance in a new market and priced their policies too low. While these insurers will, thanks to a federal subsidization program for losing insurers called Risk Corridors, not entirely lose their shirts in the first year of the program as a result, they do stand to lose a lot of money that they will likely want to make up in any subsequent years of the Affordable Care Act.

New data analysis finds significant dispersion in plan premiums

This post will contribute some new data analysis that suggests the likelihood of the winner’s curse materializing as well as the magnitude of such a curse. Basically, I have sucked into my computer official government data on the 78,000 plans sold on the federal marketplace and done a lot of number crunching. The data shows a significant dispersion of prices offered by insurers for plans in the same geographic area, of the same metal tier and offering the same form of coverage (PPO, POS, HMO, or EPO) . While this dispersion does not prove that the low prices are outliers reflecting either miscalculation by some insurers or only-temporary use of low prices, it does suggest a significant possibility that such is the case.

Let’s take an example. Here are the prices offered where I live, Harris County, Texas — mostly Houston — for an HMO Silver Policy to a couple with two kids. The couple has an average age of 50 years old. We’ll call this hypothetical family “The Chandlers,” as a matter of convenience. The graphic shows the dispersion of premiums normalized so that the lowest price for a given policy is given a value of 1.

Dispersion plot for Harris County, Texas, Silver HMO policies sold to Couple, aged, 50 with two children

As one can see, for the Harris County, Texas policies shown here, although there are three policies that have premiums fairly close to the minimum, there are, however, two policies that have premiums more than 30% more than the minimum. If the mean premium estimated by insurers is “correct,” the insurer selling a Silver HMO policy at the lowest price will lose about 17%. The implication, if the Harris County plan is representative and if the mean premium is closer to the true risk than the low premium, is that the insurers most likely to win business due to low prices are likely to lose a considerable amount of money.

There are several potential rejoinders to the suggested implication of the graphic. Let me address each of them in turn.

Might Harris County, Texas be unusual?

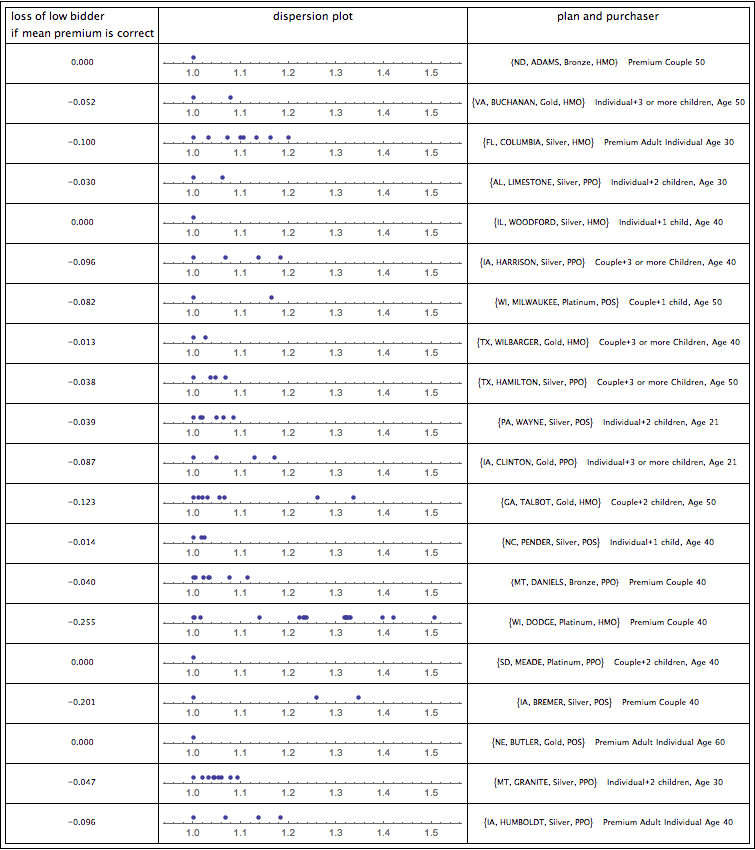

One response is that the example for Harris County, Texas Chandlers is unrepresentative. Houston, for example, has some very fancy hospitals and some not so fancy hospitals; so maybe premium dispersion for Harris County simply reflects whether one has access to the fancier hospitals (and the doctors who have admitting privileges to them). I have considered this possibility and find that, actually, the example I provide is pretty representative. Here, for example, are 20 randomly selected examples. For each plan, I show the amount the low bidder would lose if the average premium is “correct,” the dispersion of premiums, and the plan and purchaser randomly chosen. Of the ones in which there are any significant number of policies available, most of the premiums show a dispersion pattern qualitatively similar to that in Harris County for The Chandlers. Indeed, some of the random examples show dispersion considerably greater than that for the Harris County silver HMO policies. Except where there is little competition for plans and the low bidder is thus selling at the average price, the result presented above does not look like a fluke.

Dispersion Plot and potential losses of low bidder for 20 random plans and purchasers

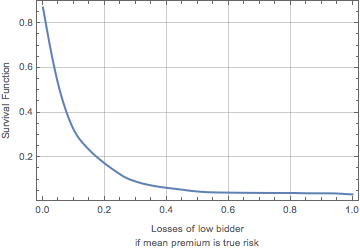

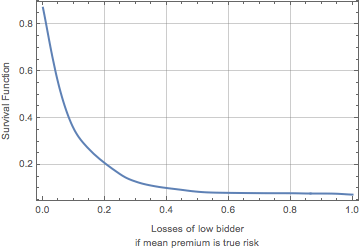

I can double check this result by computing for 5,000 random combinations of plans and purchasers the losses of the low bidder if the true risk was equal to the mean premium charged for policies and purchasers of that type. The graphic below shows the “survival function” (or “exceedance curve”) for the resulting distribution of these losses. The value on the y-axis is the probability that the losses will exceed the value on the x-axis. The results shown below confirm that the situation for Harris County Silver HMO plans sold to The Chandlers is not all that unusual. As one can see, losses of more than 10% take place more than 30% of the time and losses of more than 20% take place about 17% of the time. A rather scary picture.

Exceedance curve of the distribution of losses of low bidders for random plan-purchaser combinations on the assumption that the mean premium represents the true risk

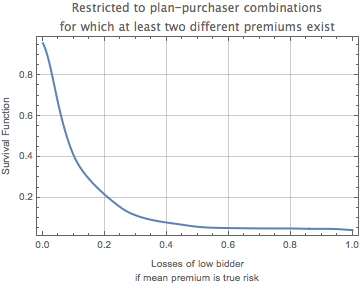

In fact, however, the situation may be even worse than depicted in the graphic above. Sometimes the losses computed by this method are low because the low bidder is also the only bidder. If we consider situations in which there is more than one bidder, here is the resulting survival function (exceedance curve) of the distribution. As one can see in the graphic below, the distribution of risks is shifted slightly to the right. Now 40% of the low bidders stand to lose at least 10% and about 21% stand to lose at least 20%.

Exceedance curve of the distribution of losses of low bidders for random plan-purchaser combinations where at least two premiums exist on the assumption that the mean premium represents the true risk

Maybe the higher priced policies are better?

Another potential explanation for price dispersion is that, even if the policies are priced differently, that does not mean that the cheapest policies are selling for too low a price. All Silver HMO policies sold in Harris County, Texas to The Chandlers may not be the same. Some may have different deductibles or different networks.

The first response to this rejoinder is that the actuarial value of the policy — the relationship between expected payments by the insurer and premiums — should be about the same for each metal tier of policies. Silver policies should all have actuarial values, for example, of 70%. So it should not be the case that one silver policy has cost sharing different than the cost sharing of another silver policy in a way that would affect the premium charged for the policy. Moreover, the calculations underlying this post keep HMOs, PPOs, POS plans and EPOs apart; so it should not be the case that observed premiums differ because, perhaps, the cheaper plans are HMOs whereas the more expensive ones are PPOs.

Of course, cost sharing is not the only way in which policies within a given location, of the same metal tier and sold to the same purchaser could vary. One policy might offer richer benefits than another. It could have a richer network with more doctors available or more prestigious and expensive hospitals inside the network. Could that be responsible for a substantial part of the premium dispersion we see? It’s impossible to tell for sure — the data published by HHS does not attempt to quantify the richness of the network being offered. I do find it difficult to believe, however, that such differences are responsible for the entirety of differences in excess of 20% between the low bidder and the mean bid, or, for that matter, differences in excess of 40% that sometimes occur between the low bidder and the higher bidders.

Maybe the average premium is meaningless; the low bidder got it right

Of all the potential rejoinders I have considered, the one now forthcoming is the one that is most troubling. There is nothing the data standing by itself can tell us whether most of the insurers have it right and the low insurers are about to lose their shirts or whether the low insurers have been more insightful or have managed to keep costs down such that they will break even (or even make money) selling their policies at low premiums. And, yet, I am doubtful. One can view the mean or median of the premiums as an “ensemble model” of the true cost of providing care under the Affordable Care Act. And there is research (examples here, here and here) suggesting that ensemble models predict better in many open-textured situations than individual models. So, while it’s possible, I suppose, that in every jurisdiction the low bidder is predicting more accurately than the group of insurance companies as a whole, such a result would be surprising. A far simpler explanation is that the low bidder — the one who is likely to win business from price sensitive insureds — is succumbing to “the winner’s curse.”

Maybe the disaggregation of plans is misleading

This is a very technical objection, but consider carefully what I have done. I have looked at all policies of a given metal tier and a given plan type in a given geographic location sold to a certain family type such as “all silver policies in Harris County, Texas, sold to The Chandlers.” But, really, plans are sold not to just to The Chandlers but to all family types. So, it could conceivably be that while the plans sold to the family type I am looking at are highly dispersed, the average premiums over all family types (weighted by prevalence of the family type) are far less dispersed. This strikes me as unlikely — why would an insurer be overcharging one family type relative to another — but you can not rule it out a priori. Maybe — just maybe — the dispersion we are observing is not real; it is just an artifact of my disaggregation of the data.