Experts who have taken a look at the Affordable Care Act have separately considered the effects of three possible sources of unexpected losses by insurers selling policies in the individual Exchanges: purchasers being older than originally projected, more purchasers being women than originally projected, and purchasers having poorer health than originally projected. And, at least with respect to the potential for age-based problems, the prestigious Kaiser Family Foundation has given supporters of the ACA considerable comfort by saying, worst case, older purchasers might result in only a 2.5% increase in insurer costs. But no one to my knowledge — until now — has carefully considered the combined effects of these three sources of potential cost increases and, most likely, pressure for future premium increases.

I have now made an effort to consider the effects of these three sources of insurer losses acting together. Based on that effort, which represents the culmination of work over the past month, I believe it quite possible that insurer losses could amount to 10%, approximately 4% due to purchasers being older than expected, 1% due to greater purchases by women, particularly those in their 20s and 30s, and another 5% due to purchasers having poorer health than expected.

There are four major caveats that should be emphasized up front. (1) These figures are estimates with large error bars; and anyone pretending to great exactitude in this field, particularly as much of the best data is not yet available, is, I suspect, likely pursuing more of a political agenda than a scholarly one. Losses could be close to zero; losses could be in the 15% range. Still, as I am going to show, significant losses are a serious possibility. (2) These losses are computed without consideration of “risk corridors” under section 1342 of the Affordable Care Act. That provision basically calls on taxpayers to pay insurers losing money on the Exchanges a significant subsidy. After consideration of Risk Corridors, average net insurer losses could range anywhere from close to zero to around 6%-7%. (3) These are national figures. There are states such as West Virginia in which the age distribution is considerably worse right now than it is nationally. One should not expect any of the rates of insurer losses (or profits) to be uniform across states or, indeed, across insurers. The figures developed here are an attempt at a rough average. (4) The figures are based on the last full release of data by HHS on enrollment in the Exchanges; if matters change and, for example, the proportion of younger enrollees grows or the proportion of men grows, the loss rates I project here are likely to decline.

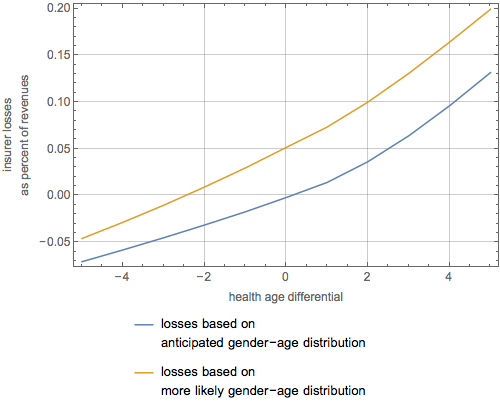

The graphic below summarizes my conclusions. It shows insurer losses (or gains) as a function of a “health age differential” under two scenarios. By health age differential I mean the difference in ages between someone who has the expected health expenses of the actual enrollee and the chronological age of the enrollee. Thus, if an enrollee was actually 53 but had the health expenses of an average 57 year old, their health age differential would be 4. If they had the health expenses of a 50 year old, their health age differential would be negative 3. The yellow line shows insurer losses as a function of the health age differential assuming that the joint distribution of gender and age stays the way it was when HHS last released data. The blue line shows insurer losses as a function of the health age differential assuming that the joint distribution of gender and age ends up the way it was originally projected to be. As enrollment under the ACA increases and the proportion of younger enrollees increases, one might expect the ultimate relationship to head from the yellow line down to the blue line. My assertion that losses could well be 10% is based on the assumption that the joint distribution of gender and age stays the way it is now but that the health of enrollees is equivalent, on average, to those 2 years older than their chronological age. An assumption that enrollees could have health equivalent, on average, to those 4 years older than their chronological age, yields insurer losses of greater than 15% assuming the current joint distribution stays in place and about 10% assuming the original distribution ends up being correct.

The graphic above is useful because it gives what hitherto had been missing in discussions of problems in the individual Exchanges: some sense of the relative magnitude of problems created by age-based adverse selection (older people enrolling disproportionately) and health-based adverse selection (sicker people enrolling disproportionately). Roughly speaking, the degree of price increases induced by the current age and gender imbalances is roughly equivalent to what would occur if the health of the enrollees was, on average, equivalent to those of persons 2.5 years old than they actually are.

So what does it all mean?

At some point, a journalist is likely to ask me what this all means? Is there going to be a death spiral? I would say we are right on the cusp. Losses of 10% by insurers relative to expectations, coupled with whatever increase results from medical inflation, isn’t so enormous that I could say, yes, for sure we are heading into a death spiral. But neither is it such a small number that the risk can be ignored. Moreover, as noted above, the 10% figure is a national average and we need to reduce it because of risk corridors. In some states, however, where the age and gender figures may be worse or the health of enrollees is particularly problematic or where insurers just bid too low and the winner’s curse overtakes them, I still believe there is a substantial risk of a serious problem. In other states, where age and gender figures are better or insurers more accurately forecast the health of their enrollees, the risk of a death spiral is minimal. And, of course, the more people that actually end up purchasing policies in the Exchanges over the next few months, regardless of whether they come from the ranks of the previously uninsured or those who find that they can not keep their current policies, the more stable the system of insurance created by the ACA is likely to be.

So, after a lot of research, I feel more confident than ever in giving a lawyer’s answer — it all depends — and a cliche — we’re not out of the woods yet.

Computation details

The results obtained here are based on essentially the same data as user by the Kaiser Family Foundation, which includes data on the relation between age and premium under typical plans, data from the Society of Actuaries (SOA), also used by Kaiser, on the relation between gender, age and expected medical expenses, and my own prior work attempting, based on data from the Department of Health and Human Services released earlier this month, to derive a joint distribution of enrollment in the individual Exchanges based on age and gender. And, although the math can get a little complicated, the basic idea behind the computations is not all that difficult. It is essentially the computation of some complicated weighted averages. Each combination of gender and age has some expected level of insurance cost (computed by the Society of Actuaries based on commercial insurance data) and some expected premium (computed by Kaiser based on a study of the ACA). Thus, if we know the joint distribution of gender and age, we can weight each of those costs and each of those premiums properly.

There are three areas of the computation that prove most challenging. First, because HHS has not released all of the needed data, one must develop a plausible method of moving from the marginal distributions that were provided by HHS on enrollment by age and enrollment by gender into a joint distribution by gender and age. Second, one must calibrate the SOA cost data and the Kaiser premium data, which are expressed in somewhat different units, such that, if the joint distribution of gender and age was as was originally expected an insurer would just break even. And, third, one must develop a reasonable method of modeling insured populations that are drawn disproportionately from persons who have higher medical expenses. I believe I have now come up with reasonable solutions to all three issues.

Solution #1

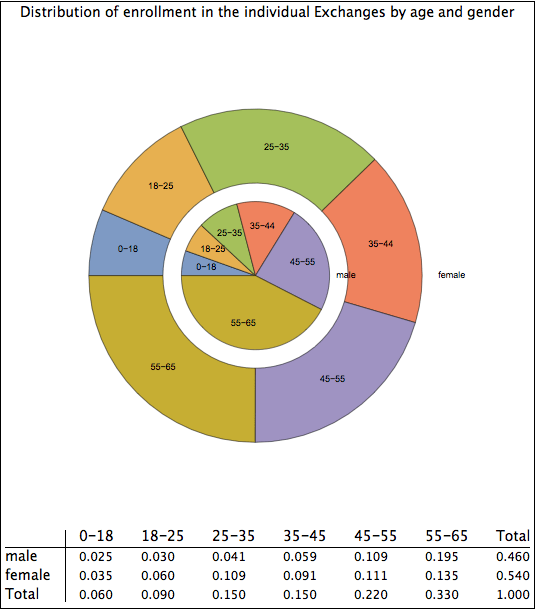

The solution to the first issue, moving from a marginal distribution to a joint distribution, was detailed in my prior blog entry. In short, one finds a large sample of possible joint distributions that match the marginal distributions and scores them according to how well they match the property that people who are subsidized more likely to enroll. One takes an average of a set of solutions that score best. There is an element of judgment in this process on the degree to which individuals respond to subsidization incentives and, all I can say, is that I believe my methodology is reasonable, avoiding the pitfall of thinking that subsidization is irrelevant or of thinking that it is the only factor that matters in determining enrollment rates. I present again what I believe to be the most likely joint distribution of enrollment by gender and age.

Solution #2

The solution to the second problem is obtained using calculus and numeric integration. One computes the expected costs and expected premiums given the original joint distribution of enrollees, which is taken to be a product distribution of which one distribution is a “Bernoulli Distribution” in which the probability of being a male or female is equal and the other is a “Mixture Distribution” in which the weights are those shown below (and taken from the Kaiser Family Foundation web site) and the components are discrete uniform distributions over the associated age ranges.

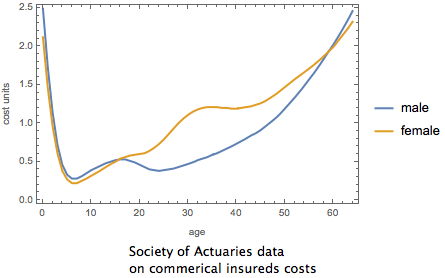

The Society of Actuary data on the relationship between age, gender and medical costs is shown here.

The premiums under the ACA are shown here.

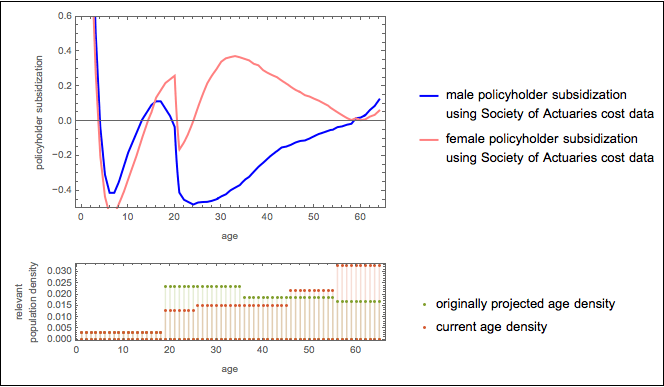

These two plots combined can give us a subsidization rate plot by gender and age. It is shown below along with an associated plot showing the distribution of enrollees by age as was originally assumed and as appears to be the case.

Solution #3

To model adverse selection based on expensive medical conditions, I simply added a health age differential to the insureds. That is, in computing expected medical costs, I assumed that people were their actual age plus or minus some factor. (Ages after this addition were constrained to lie between 0 and 64). The graphic above showed insurer losses as a function of this “health age differential” under two scenarios.

Technical Note

A Mathematica notebook containing the computations used in this blog entry is available . here on Dropbox. I’m also adding a PDF version of the notebook here. I want to thank Sjoerd C. de Vries for coming up with an elegant method within Mathematica of describing the joint distribution used in the computations of various integrals. I am responsible for any mistakes in implementation of this method and my use of Mr. de Vries idea implies nothing about whether he agrees, disagrees or does not care about any of the analyses or opinions in this post.