According to a news report today from the Associated Press, the enrollment numbers in Colorado are about half of what the state had projected as its “worst case scenario” for enrollment in its Exchange. The 6,001 Colorodoans who have enrolled thus far (and that is enrolled, not yet paid) is also way less than the 20,186 that had served as the midpoint projection for this time in the open enrollment season. Colorado officials apparently believed that 136,000 people would enroll by the end of 2014. Enrollment thus far has apparently been complicated, however, by a requirement that consumers seeking a subsidy on the exchange first find out if they qualify for Medicaid, which may require a 12-page application.

Three facts make the low Colorado numbers yet more troubling for those concerned either about a reduction in the number of uninsured individuals or about the prospects that those getting enrollment in the Exchanges for 2014 will shortly find themselves sucked into an adverse selection death spiral.

First, these low figures are coming in a state where the web site has, for the most part, been operating respectably (further details here) and not in a state dependent on healthcare.gov.

Second, it comes in a state where between 106,000 and 250,000 individual health insurance policies have been cancelled. I have an inquiry in but have not yet been able to find from published sources whether Colorado will permit insurers to reinstate those policies and under what conditions. [LATE BREAKING NEWS at 13:52 Houston time: Colorado insurance official says Colorado expects to announce a decision on this point later today or tomorrow (per email from Vincent Plymell, Communications Director at the Colorado Department of Regulatory Agencies, who courteously responded to my inquiry)]

Third, Colorado already had 1,227 people enrolled in the Federal Pre-Existing Condition Insurance Plan (PCIP). One would think those people, who tend to have high medical expenses and are willing to pay full freight for insurance, would have been among the earliest to sign up under the Colorado exchange with the potential for subsidized rates. Thus, some of the 6,001 already enrolled may not represent a reduction in people without insurance to people with health insurance but merely a substitution from one federally created plan to another.

As discussed yesterday on this blog and elsewhere in the media, Cover California, the state entity organizing enrollment there, has released data showing the age distribution of the group thus far enrolling in plans on its Exchanges. Although I took a rather cautionary tone about the age distribution — fearing it could stimulate adverse selection — the head of Cover California and some influential media outlets generally favorable to the Affordable Care Act have been considerably more cheerful. So, who’s right? For reasons I will now show — and probably to no one’s surprise — me. (More or less).

To do this, we need to do some math. It’s a more sophisticated variant of the back of the envelope computation I undertook earlier on this blog. The idea is to compute the mean profit of insurers in the Exchange as a function of the predicted versus the actual age distribution of the pool they insure. Conceptually, that’s not too difficult. Here are the steps.

1. Compute the premium that equilibrates the “expectation” of premiums and costs for the predicted age distribution of the pool they insure. Call that the “predicted equilibrating premium.”

2. Compute the expected profit of the insurer given the predicted equilibrating premium and the actual age distribution of the pool they insure.

3. Do Step 1 and Step 2 for a whole bunch (that’s the technical term) of combinations of predicted age distributions and actual age distributions.

Moving from concept to real numbers is not so easy. The challenge comes in getting reasonable data and, since there are an infinite number of age distributions and in developing a sensible parameterization of some subset of plausible distributions.

The Data

The data is interesting in and of itself. To get the relationship between premiums and age, I used the robust Kaiser Calculator. Since healthcare.gov itself recommends the web site (their own site seems to have a few problems) and I have personally validated its projected premiums for various groups against what I actually see from various vendors, I believe it is about as reliable a source of data as one is likely to find anywhere right now. So, by hitting the Kaiser Calculator with a few test cases and doing a linear model fit using Mathematica (or any other decent statistics package), we are able to find a mathematical function that well captures a (quadratic) relationship between age and premium. (The relationship isn’t “really” quadratic, but quadratics are easy to work with and fit the data very well.) The graphic below shows the result.

Nationwide average health insurance premium for a silver plan as a function of age

We can normalize the graphic and the relationship such that the premium at age 18 (the lowest age I consider) is 1 and everything else is expressed as a ratio of the premium at age 18. Here’s the new graphic. The vertical axis is now just expressed in ratios.

Nationwide average health insurance premium ratio for a silver plan as a function of age

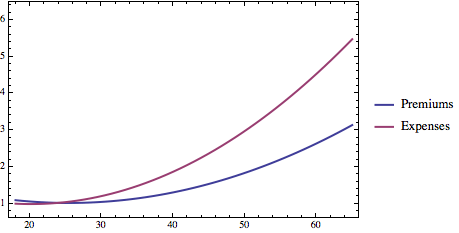

To get the relationship between cost and age, I used a peer reviewed report from Health Services Research titled “The Lifetime Distribution of Health Care Costs.” It’s from 2004 but that should not matter much: although the absolute numbers have clearly escalated since that time, there is no reason to think that the age distribution has moved much. I can likewise do a linear model fit and find a quadratic function that fits well (R^2 = 0.982). Again, I can normalize the function so that its value at age 18 is 1 and everything else is expressed as a ratio of the average costs incurred by someone at age 18. Here’s a graphic showing the both the relationship between age and normalized premiums in the Exchanges under the Affordable Care Act and normalized costs.

The key thing to see is that health care claims escalate at a faster rate than health care premiums. Others have noted this point as well. They do so because the Affordable Care Act (42 U.S.C. § 300gg(a)(1)(A)(iii)) prohibits insurers from charging the oldest people in the Exchanges more than 3 times what they charge the youngest people. Reality, however, is under no such constraint.

Parameterizing the Age Distribution

There are an infinite number of potential age distributions for people purchasing health insurance. I can’t test all of them and I certainly can make a graph that shows profit as a function of every possible combination of two infinite possibilities. But, what I can do — and rather cleverly, if I say so myself — is to “triangulate” a distribution by saying how close it is to the age distribution of California as a whole and how close it is to the age distribution of those currently in the California Exchange pool. I’ll say a distribution has a “Pool Parameter Value” of 0 if it comes purely from California as a whole and has value of 1 if it comes purely from the California Exchange pool. A value of 0.4 means the distribution comes 40% from California as a whole and 60% from the current California Exchange pool. The animation below shows how the cumulative age distribution varies as the Pool Parameter Value changes.

How the age distribution varies as the pool goes from looking more like California as a whole to looking more like the current pool as a whole.

Equilibration and Results

The last step is to compute a function showing the equilibrium premium as a function of the predicted pool parameter value. We can then use this equilibrating premium to compute and graph profit as a function of both predicted pool parameter value and actual pool parameter value.

The figure below shows some of the Mathematica code used to accomplish this task.

Mathematica code used to produce graphic showing relationship between insurer profit in the California exchanges and the nature of the predicted pool and the actual pool

Stare at the graphic at the bottom. What it shows is that if, for example, California insurers based their premiums on the pool having a “parameter value” of 0 (looks like California) and the actual pool ends up having a “parameter value of 1 (looks like the current pool), they will, everything else being equal, lose something like 10% on their policies and probably need to raise rates by about 10% the following year. If, on the other hand, they thought the pool would have a parameter value of 0.5 and it ended up having a parameter value of 0.75 the insurers might lose only about 3.5%.

Bottom Line

If I were an insurer in California I’d be concerned about the age numbers coming in, but not panicked. First, I hope I did not assume that my pool of insureds would look like California as a whole. I had to assume some degree of adverse selection. But it does not look as though, even if I made a fairly substantial error, the losses will be that huge. That’s true without the Risk Corridors subsidies and it is all the more true with Risk Corridor subsidies.

What I would be losing sleep about, however, is that the pool I am getting is composed disproportionately of the sick of all ages. If I underestimated that adverse selection problem, I could be in deep problem. My profound discomfort would arise because, while I get to charge the aged somewhat more, I don’t get to charge the sick anymore. And there’s one fact that would be troubling me. Section 1101 of the Affordable Care Act established this thing calledthe Pre-Existing Condition Insurance Pool. It’s been in existence (losing boatloads of money) for the past three years. It held people who couldn’t get insurance because they had pre-existing conditions. They proved very expensive to insure. There are 16,000 Californians enrolled in that pool. But that pool ends on January 1, 2014. And the people in it have to be pretty motivated to get healthy insurance. Where are they going to go? If the answer is that a good chunk of the 79,000 people now enrolled in the California pool are former members of the PCIP, the insurers are in trouble unless they get a lot more healthy insureds to offset these individuals.

California has frequently been cited as an early Affordable Care Act success story with enrollment coming at least closer to projected numbers than in other states. Today’s release of information from Covered California, the state entity organizing enrollment there, shows a mixed picture about the likelihood that the ACA will become a stable source of non-discriminatory relatively inexpensive health insurance in the nation’s most populous state.

A highlight from the report is that 79,891 have at least gotten as far as selecting a plan since enrollment opened on October 1, 2013. That’s better than any other state and better — at least as of the last report — of all the other states combined using the healthcare.gov portal. And, because, contrary to the wishes of California Insurance Commissioner Dave Jones, Covered California has decided not to permit those with recently enrolled in underwritten individual health insurance to “uncancel” policies that do not provide Essential Health Benefits, there is the potential to add more people to the Exchange pools than would otherwise be possible. Additional good news: the pace of enrollment has picked up over the past two weeks. Still, to date, the 79,891 who have at least selected a plan are only 6% of the 1.3 million that the federal government projected California would enroll through 2014. And the web site in California appears to be working acceptably.

Perhaps the news on the number of enrollees is equivocal. It’s better than other states, and it’s still early, but, relative to the projections on which the ACA was premised, it is not good at all. There is also, however, what appears to me to be distinctly troubling news coming from California. We have another report on the age distribution of enrollees: so far, it is disproportionately old. And this is true in the state in which enrollment has progressed the furthest and in the nation’s most populous state. So, the data is potentially significant not just as an augury of what may be seen in other states but because a disproportionately elderly population in the largest state is, in an of itself, a problem.

Although persons age 55 through 64 constitute about 18% of the California population aged 18 through 64, they constitute double that, 36%, of persons in that same age segment who have enrolled for a plan. Similarly, although persons age 45 through 64 constitute about 41% of the California population, they constitute 59% of those who have enrolled thus far. As discussed earlier on this blog and elsewhere, because premium ratios between old and young are capped at 3 to 1, whereas actual claim ratios are likely to be higher, disproportionate enrollment of the elderly can help drive an adverse selection death cycle. This would be all the more true if the older people — it’s hard to call people age 55 “elderly”” — that are enrolling are disproportionately unhealthy relative to their age-group peers. Claims, therefore, by Covered California Director Peter Lee that “enrollment in key demographics like the so-called young invincibles is very encouraging” rest on theories of economics and statistics that I do not understand.

A Side Note on Market Concentration

By the way, who’s on the hook in the event the ultimate pool is distinctly more expensive than insurers anticipated? It’s the usual suspects. The big “winners” in California thus far are the usual suspects: Anthem Blue Cross has 28.1%, Kaiser Permanente, a California fixture, has 26.8%, Blue Shield of California has 25.6% and Health Net (with headquarters in Southern California) has 15.7%. Together, these four have 96% of the market with a “Herfindahl Index” of a moderately concentrated 2410. Dreams, therefore, of new competitors entering the marketplace, thus far seem illusory. But it is these “winners” that stand to lose the most money — and be the greatest recipient of federal redistributions under Transitional Reinsurance, Risk Corridors and Risk Adjustments — in the coming year if the trends hold up.

Exploring the likely implosion of the Affordable Care Act